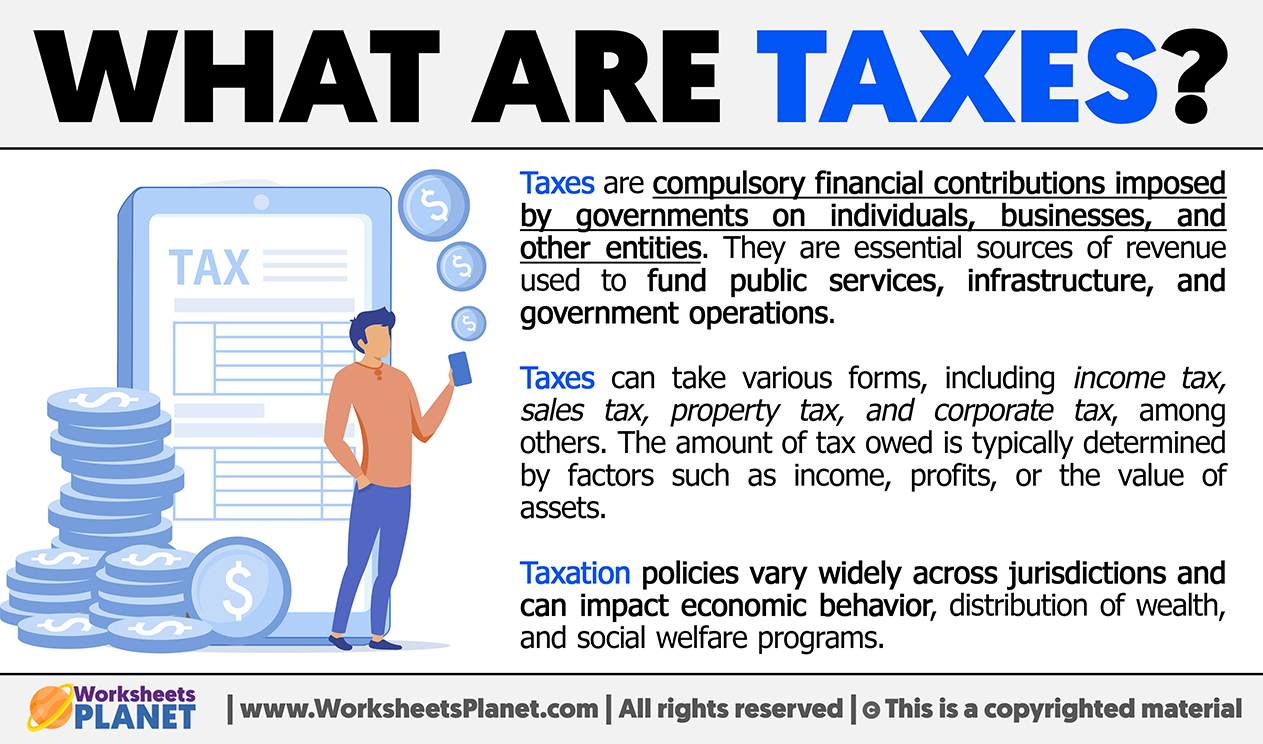

The concept of a tax, at its core, represents a compulsory financial charge or other levy imposed upon a taxpayer (an individual or legal entity) by a governmental organization in order to fund public expenditures. Far from being a static concept, the definition and application of taxation have evolved dramatically throughout history, reflecting societal shifts, economic imperatives, and, increasingly, technological advancements. In the modern era, particularly within the realm of “Tech & Innovation,” understanding what constitutes a tax goes beyond a simple dictionary entry; it involves appreciating how innovative governance and cutting-edge technologies both shape and are shaped by taxation.

Historically, taxes were a rudimentary means of funding monarchies or wartime efforts. Today, they are sophisticated instruments of public policy, designed not only to raise revenue but also to redistribute wealth, stimulate economic activity, discourage harmful behaviors, and foster innovation. This complex interplay positions the definition of a tax firmly within the broader discourse of societal innovation—how we organize, fund, and propel collective progress.

The Evolving Definition: Taxation as Social Innovation

To truly grasp the definition of a tax in the context of innovation, one must look at its origins and its journey through various stages of human civilization. Taxation itself can be viewed as one of humanity’s earliest and most enduring social innovations—a systemic method for resource aggregation and allocation without which complex societies could not function.

Ancient Roots and Foundational Principles

The earliest forms of taxation emerged with the advent of settled agriculture and the need for communal projects like irrigation systems or defensive structures. These “taxes” were often in the form of labor, goods, or a portion of agricultural yield. From ancient Egypt’s grain levies to the tithes of medieval Europe, the fundamental principle remained consistent: a mandatory contribution for the common good or the maintenance of ruling power. This early “social technology” enabled specialization, infrastructure development, and the establishment of governance—foundations upon which all subsequent innovations would be built.

The definition here was simple: a non-voluntary transfer of resources from the individual to the collective authority. Its innovation lay in systematizing collective effort beyond ad-hoc contributions, establishing a predictable mechanism for public finance. This represented a critical leap in societal organization, allowing for planned, large-scale projects and the maintenance of a non-producing governing or administrative class, which itself could then focus on further innovations.

Modern Interpretations and Economic Engineering

As societies grew more complex, so too did the definition and types of taxes. The Industrial Revolution brought income taxes, property taxes, and excise duties, designed to fund burgeoning public services like education, healthcare, and extensive infrastructure. Here, the definition expanded to encompass progressive taxation (where higher earners pay a larger percentage), signaling an innovative shift towards using taxation as a tool for social equity rather than just revenue generation.

In the 20th and 21st centuries, the definition further broadened to include concepts like Value Added Tax (VAT) or Goods and Services Tax (GST), carbon taxes, and increasingly, digital service taxes. These aren’t just new types of taxes; they represent innovative approaches to tax design—economic engineering aimed at influencing consumer behavior, encouraging environmental sustainability, or capturing value from new economic activities. The very act of crafting these new tax structures is an exercise in policy innovation, constantly refining what a compulsory levy entails and what societal goals it can achieve. The modern definition, therefore, incorporates not just the compulsory nature but also the deliberate policy objectives embedded within the tax structure.

Defining Taxes in the Digital Age: Tech’s Influence

The exponential growth of technology has presented both unprecedented challenges and opportunities in defining and implementing taxation. The digital age has introduced new forms of economic activity that challenge traditional tax frameworks, prompting significant innovation in how taxes are conceived, collected, and understood.

New Taxable Entities and Digital Commerce

The rise of e-commerce, the gig economy, cryptocurrencies, and digital services has stretched conventional tax definitions to their limits. How do you tax a service provided across borders with no physical presence? What defines an asset in the virtual world? These questions force legislative bodies to innovate the definition of what constitutes taxable income, property, or transactions. For instance, the discussion around “digital service taxes” is an attempt to define and capture value generated by large tech companies in jurisdictions where they have users but little physical presence. Similarly, the debate over whether cryptocurrencies are commodities, currencies, or securities directly impacts how they are defined for tax purposes.

This era demands agility in defining tax liabilities, ensuring fairness and revenue generation without stifling innovation. The challenge lies in creating definitions that are future-proof, adaptable to rapidly evolving technological landscapes, and internationally harmonized to prevent arbitrage and ensure equitable collection. This iterative process of defining and re-defining is a testament to the dynamic relationship between taxation and technological progress.

Big Data and AI in Tax Definition and Compliance

Technology is not just creating new things to tax; it’s also revolutionizing how taxes are administered and how their definitions are applied. Big data analytics and Artificial Intelligence (AI) are transforming tax agencies worldwide. AI algorithms can process vast amounts of financial data, identify complex patterns, and flag discrepancies that human auditors might miss. This technology helps refine the operational definition of tax evasion or non-compliance, making it easier to detect and deter.

Moreover, AI-powered systems can help policymakers model the impact of new tax definitions before implementation, predict revenue outcomes, and understand behavioral responses. This represents a significant innovation in tax administration, shifting from reactive auditing to proactive, data-driven policy design and enforcement. The precision and reach of these technologies mean that the defined obligations of taxpayers are enforced with greater accuracy and efficiency, reinforcing the compulsory nature of taxation in an increasingly transparent digital environment.

The Interplay of Policy, Law, and Innovation in Tax Definition

The definition of a tax is not solely an economic concept; it is deeply embedded in legal frameworks and policy objectives. These frameworks are constantly being innovated to respond to global changes and domestic needs.

Legislative Innovation in Tax Law

Tax law is a continuously evolving field, with legislatures worldwide constantly innovating their statutes to reflect new economic realities, technological advancements, and societal priorities. From defining what constitutes “residence” for digital nomads to establishing clear rules for the taxation of intangible assets, legislative bodies are engaged in an ongoing process of definitional refinement. Each new tax act or amendment is an act of legal innovation, attempting to codify and clarify the scope and application of compulsory levies in a dynamic world.

This innovative legal process often involves intricate debates and compromises, as governments seek to balance revenue generation with economic competitiveness and social equity. The language used in these laws effectively defines a tax in its most concrete, enforceable form, dictating who pays, what they pay on, and how much.

International Harmonization and Cross-Border Definitions

In an interconnected global economy, the definition of a tax becomes even more complex, necessitating international cooperation and innovative frameworks. The rise of multinational corporations and digital trade has highlighted the need for harmonized tax definitions and rules across different jurisdictions. Initiatives led by organizations like the OECD (Organisation for Economic Co-operation and Development) aim to innovate international tax norms, addressing issues like base erosion and profit shifting (BEPS).

These efforts represent significant innovation in international governance, moving towards a shared understanding of what constitutes taxable presence, profit, and activity in a cross-border context. Without such efforts, inconsistent definitions could lead to double taxation, tax havens, or unfair competition, underscoring the importance of innovative collaborative efforts to define and apply taxation globally.

Beyond Revenue: Taxes as Tools for Innovation and Behavior Shaping

Perhaps one of the most innovative aspects of modern taxation is its use as a strategic tool to drive specific behaviors, stimulate particular sectors, and foster societal change, rather than simply raising revenue.

Incentivizing Green Tech and R&D through Tax Definitions

Governments worldwide use the power of taxation to incentivize innovation, especially in critical areas like green technology and research & development (R&D). By defining certain activities as eligible for tax credits, exemptions, or reduced rates, governments effectively subsidize and stimulate growth in desired sectors. For example, tax breaks for investments in renewable energy, electric vehicle purchases, or R&D expenditures directly influence corporate and individual behavior.

Here, the definition of a tax is not just about what is owed, but what can be saved or gained by engaging in innovative activities. These tax incentives are sophisticated policy innovations designed to steer private capital and effort towards public good goals, such as combating climate change or enhancing a nation’s competitive edge in tech. The clear definition of what qualifies for these incentives is paramount to their effectiveness, showcasing taxation’s role as a proactive tool for shaping future innovation.

Defining Taxes for Social Engineering and Economic Stimulus

Beyond direct technological innovation, taxes are also defined to achieve broader social and economic engineering goals. “Sin taxes” on tobacco or alcohol aim to discourage consumption of harmful products, while wealth taxes or inheritance taxes are defined to address wealth inequality. During economic downturns, governments may redefine tax burdens or offer temporary tax holidays as part of stimulus packages.

These applications demonstrate the dynamic and versatile nature of the tax definition. It moves beyond a mere financial obligation to become a highly flexible and powerful instrument of policy, capable of nudging, encouraging, or discouraging a vast array of human activities. In the realm of “Tech & Innovation,” this means taxes can be innovatively defined to support new industries, facilitate digital transformation, or mitigate the societal impacts of rapid technological change.

In conclusion, the definition of a tax, while fundamentally a compulsory levy for public funding, is far more complex and dynamic when viewed through the lens of “Tech & Innovation.” It is a concept that has evolved as a core social innovation, continually redefined by technological advancements, legislative ingenuity, and global collaboration. Taxes are not merely financial burdens; they are powerful, innovative tools whose definitions reflect and shape the very fabric of our technologically advancing societies, guiding behavior, fostering growth, and funding the next generation of breakthroughs.