The concept of “interest rate” is fundamental to economics and finance, representing the cost of borrowing money or the return on saving it. When we speak of a “new” interest rate, it typically refers to a change in the prevailing benchmark rates set by central banks or significant shifts in market-driven rates. These changes have a ripple effect across the entire economy, influencing everything from individual loan payments to large-scale business investments. Understanding what constitutes a “new” interest rate and the factors driving these changes is crucial for informed decision-making in both personal and professional spheres.

Understanding the Pillars of Interest Rates

Interest rates are not monolithic; they exist in various forms and are influenced by a complex interplay of economic forces. At the core of these rates are the policies of central banks, which act as the primary architects of monetary policy. However, market forces also play a significant role, shaping the rates individuals and businesses encounter daily.

Central Bank Benchmark Rates

The most significant “new interest rates” often originate from the decisions of a nation’s central bank. In the United States, this is the Federal Reserve, and its primary tool is the Federal Funds Rate. This is the target rate that commercial banks charge each other for overnight lending of reserves held at the Federal Reserve. While not directly charged to consumers, this benchmark rate influences all other interest rates in the economy.

The Federal Funds Rate and Its Mechanism

The Federal Reserve influences the Federal Funds Rate through various tools. Open market operations, where the Fed buys or sells government securities, are a primary method. When the Fed buys securities, it injects money into the banking system, increasing the supply of reserves and putting downward pressure on the Federal Funds Rate. Conversely, selling securities withdraws money, tightening credit and pushing the rate higher. The Federal Open Market Committee (FOMC) meets regularly to assess economic conditions and decide whether to adjust the target range for the Federal Funds Rate. A “new interest rate” in this context means the FOMC has announced a change to this target range.

The Discount Rate and Reserve Requirements

Beyond the Federal Funds Rate, central banks also set the Discount Rate, which is the interest rate at which commercial banks can borrow money directly from the central bank. This serves as a backup source of liquidity. Changes in the discount rate also signal the central bank’s monetary policy stance. Additionally, Reserve Requirements, the fraction of deposits that banks must hold in reserve and cannot lend out, can also be adjusted. While less frequently used as an active monetary policy tool, changes to reserve requirements can significantly impact the amount of money available for lending, thereby influencing interest rates.

Market-Driven Interest Rates

While central bank rates provide a foundation, the interest rates encountered by individuals and businesses are often determined by market forces. These include factors like supply and demand for credit, inflation expectations, and the perceived risk associated with lending to a particular borrower.

The Prime Rate: A Consumer Bellwether

The Prime Rate is another crucial benchmark, though it is set by commercial banks themselves. It is the interest rate that commercial banks charge their most creditworthy customers. While it’s not a single, universally fixed rate, it tends to move in lockstep with the Federal Funds Rate. Banks typically announce their prime rate as a specific percentage above the upper limit of the Federal Funds target range. When the Fed changes its target, banks almost invariably adjust their prime rates accordingly, leading to a “new interest rate” for many consumer loans.

Treasury Yields: Indicative of Risk and Inflation

Interest rates on government debt, such as Treasury Bills, Notes, and Bonds, are also highly watched indicators. The yields on these securities reflect the market’s perception of risk-free returns and its expectations for future inflation and economic growth. Longer-term Treasury yields are particularly sensitive to inflation expectations. If the market anticipates higher inflation, investors will demand higher yields to compensate for the erosion of their purchasing power. A significant shift in Treasury yields can signal a “new interest rate” environment that influences corporate borrowing costs and mortgage rates.

The Mechanics of “New” Interest Rates: Drivers of Change

The designation of an “interest rate” as “new” implies a departure from a previous state. These changes are not arbitrary; they are the result of deliberate policy decisions or the dynamic forces of the market responding to evolving economic conditions. Understanding these drivers is key to predicting and adapting to shifts in borrowing and lending costs.

Monetary Policy Adjustments by Central Banks

The most direct cause of a “new interest rate” is a change in monetary policy orchestrated by the central bank. These adjustments are typically made to achieve specific macroeconomic objectives, such as controlling inflation, fostering economic growth, or maintaining financial stability.

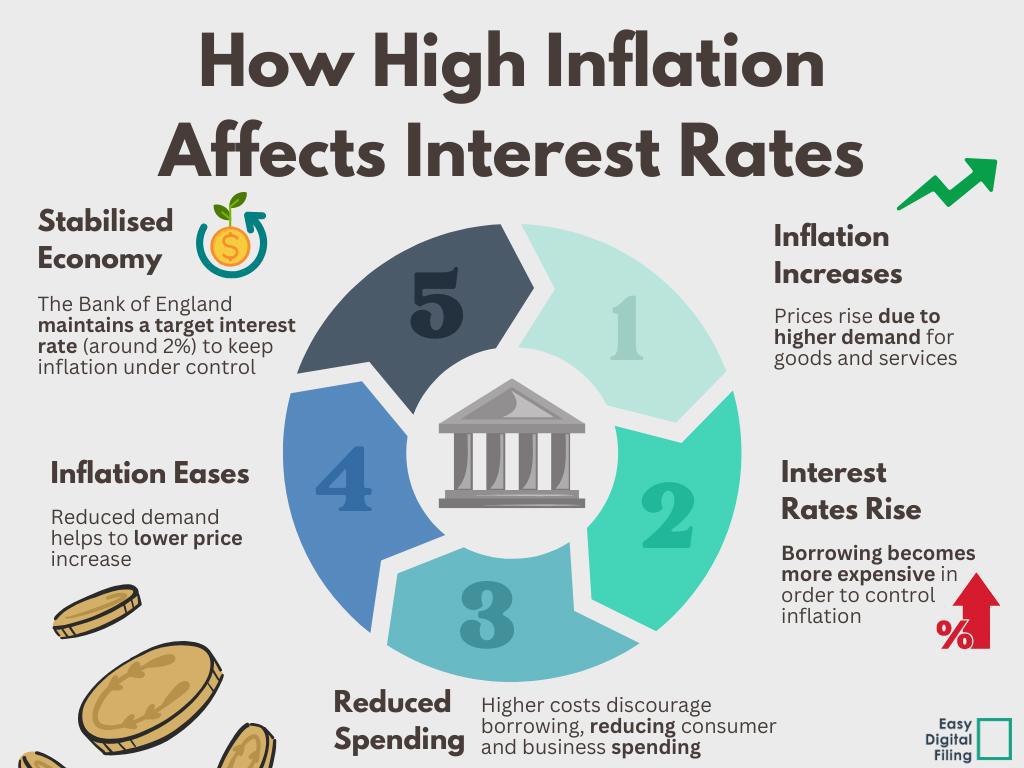

Inflation Control: The Primary Mandate

A core objective for most central banks is price stability, meaning keeping inflation at a low and predictable level. If inflation is too high, central banks will often raise interest rates. This makes borrowing more expensive, which tends to dampen consumer and business spending, thereby reducing demand and easing inflationary pressures. Conversely, if inflation is too low or if the economy is experiencing deflation, central banks may lower interest rates to stimulate economic activity and encourage spending.

Economic Growth and Employment Stimulation

Central banks also aim to promote sustainable economic growth and maximize employment. During economic downturns, where unemployment is high and growth is sluggish, central banks may reduce interest rates. Lower borrowing costs incentivize businesses to invest and expand, and encourage consumers to spend on goods and services. This increased economic activity can lead to job creation and a healthier economy. However, the balancing act is crucial; lowering rates too aggressively can lead to excessive inflation.

Financial Stability Concerns

In times of financial stress, such as a banking crisis or a credit crunch, central banks may intervene by lowering interest rates or providing liquidity to the financial system. This can help to stabilize markets, prevent widespread defaults, and ensure the smooth functioning of credit channels. The introduction of emergency lending facilities or quantitative easing programs, which effectively lower long-term interest rates, are examples of how central banks might introduce “new” rate environments to address financial stability concerns.

Economic Indicators and Market Sentiment

Beyond direct policy actions, a multitude of economic indicators and the prevailing market sentiment can influence interest rates. These factors create the backdrop against which central banks make their decisions and directly affect market-driven rates.

Inflationary Pressures and Expectations

The current rate of inflation and, perhaps more importantly, inflation expectations are paramount. If businesses and consumers expect prices to rise significantly in the future, they will demand higher interest rates on loans and investments to preserve their purchasing power. Central banks closely monitor surveys of inflation expectations and the actual inflation data (e.g., the Consumer Price Index – CPI) when setting policy. A persistent rise in inflation will invariably lead to a “new interest rate” environment characterized by higher borrowing costs.

Economic Growth and Employment Data

Data on Gross Domestic Product (GDP), unemployment rates, consumer spending, and manufacturing output provide insights into the health of the economy. Strong economic growth and low unemployment often signal that the economy is operating at or near its full potential, which can put upward pressure on interest rates as demand for credit increases and inflationary pressures build. Conversely, weak economic data suggests the need for lower interest rates to stimulate activity.

Global Economic Conditions and Geopolitical Events

Interest rates are not determined in isolation. Global economic trends, such as growth rates in major economies, commodity prices, and international capital flows, can influence domestic interest rates. Furthermore, significant geopolitical events, like wars or major trade disputes, can introduce uncertainty into the markets, leading to shifts in risk premiums and affecting borrowing costs. For instance, a global economic slowdown might prompt a central bank to lower rates to support its domestic economy, even if inflation is moderately high, due to fears of contagion.

The Impact of “New Interest Rates” on the Economy

Changes in interest rates, especially significant shifts that can be characterized as a “new interest rate” environment, have profound and far-reaching consequences for individuals, businesses, and the overall economy. These impacts are felt across various sectors and influence decision-making at every level.

Impact on Consumers

For consumers, “new interest rates” directly affect the cost of borrowing and the returns on savings.

Borrowing Costs for Mortgages, Auto Loans, and Credit Cards

When interest rates rise, borrowing becomes more expensive. This means that individuals seeking mortgages will face higher monthly payments, potentially reducing their purchasing power for homes. Similarly, auto loans and credit card interest rates will likely increase, making it more costly to finance purchases or carry a balance. This can lead consumers to postpone large purchases or reduce discretionary spending. Conversely, falling interest rates can make borrowing more affordable, stimulating demand for major purchases.

Returns on Savings and Investments

Higher interest rates generally mean better returns on savings accounts, certificates of deposit (CDs), and other fixed-income investments. This can be beneficial for savers, allowing their money to grow more quickly. However, when interest rates are very low, as they have been in recent years, savers earn minimal returns, which can impact their retirement planning and overall financial well-being. Low rates also encourage investment in riskier assets like stocks in search of higher yields.

Impact on Businesses

Businesses are also significantly affected by shifts in interest rates, influencing their investment decisions, profitability, and expansion plans.

Investment and Expansion Decisions

For businesses, interest rates represent the cost of capital. When interest rates are low, borrowing money to invest in new equipment, expand facilities, or conduct research and development becomes more attractive. This can fuel business growth and job creation. However, as interest rates rise, the cost of capital increases, making such investments less appealing. Businesses may scale back or postpone expansion plans, which can slow down economic activity.

Debt Servicing and Profitability

Companies with existing debt are directly impacted by interest rate changes. For those with variable-rate debt, an increase in interest rates means higher debt servicing costs, which can eat into profits. This is particularly true for highly leveraged companies. Conversely, falling rates can reduce a company’s interest expenses, boosting its bottom line. The ability of a company to service its debt is a key factor in its financial health and its perceived investment risk.

Impact on Government Finances

Government entities, including national treasuries and local authorities, are also sensitive to interest rate movements.

Government Borrowing Costs

Governments finance their operations and public projects through borrowing. An increase in interest rates means that the government will have to pay more in interest on its outstanding debt and on any new debt it issues. This can strain government budgets, potentially leading to cuts in public services or an increase in taxes. Conversely, lower interest rates reduce the cost of government borrowing, freeing up resources for other priorities.

Fiscal Policy Implications

Changes in interest rates can also influence the effectiveness of fiscal policy. For example, during a recession, a government might implement expansionary fiscal policy (e.g., increased spending or tax cuts). If interest rates are high, this stimulus might be less effective as increased government borrowing could push interest rates even higher, crowding out private investment. Central bank policies on interest rates are therefore intricately linked to the broader economic and fiscal landscape.

Navigating the “New Interest Rate” Landscape

The introduction of a “new interest rate” is not a static event but a dynamic shift that requires careful observation and strategic adaptation. Whether driven by central bank policy or market forces, these changes create both challenges and opportunities for individuals and institutions alike. Understanding the implications and developing proactive strategies can help to mitigate risks and capitalize on emerging possibilities.

Financial Planning and Risk Management

For individuals and businesses, understanding the current interest rate environment and its potential trajectory is fundamental to effective financial planning and risk management.

Adapting Personal Finances

Consumers should review their loan portfolios, particularly variable-rate mortgages, credit cards, and personal loans. If rates are rising, exploring options to refinance into fixed-rate loans or paying down high-interest debt can be prudent. Conversely, if rates are falling, individuals might consider taking advantage of lower borrowing costs for significant purchases or consolidating existing debt. For savers, assessing the best options for their savings, considering both returns and liquidity, becomes crucial in different interest rate environments.

Business Strategy and Capital Management

Businesses need to closely monitor interest rate movements and their impact on their cost of capital. This involves reviewing debt structures, considering fixed versus variable rate options for new financing, and assessing the feasibility of capital expenditure projects based on updated borrowing costs. Effective cash flow management and the maintenance of strong credit ratings become even more critical in an environment of rising rates. Hedging strategies to manage interest rate risk can also be a valuable tool.

Investment Strategies in a Changing Rate Environment

Investment decisions are heavily influenced by prevailing interest rates. A “new interest rate” environment necessitates a reassessment of investment strategies to align with evolving market dynamics.

Fixed Income Considerations

The attractiveness of fixed-income investments, such as bonds, is directly tied to interest rates. When rates rise, existing bonds with lower coupon payments become less valuable as newly issued bonds offer higher yields. Investors may need to adjust their bond portfolios by shortening durations or seeking investments with higher credit quality in a rising rate environment. Conversely, falling rates can make existing fixed-income assets more valuable and increase demand for newly issued bonds.

Equity Market Performance and Sectoral Impacts

Interest rates have a significant impact on equity markets. Higher interest rates can reduce corporate profitability and make borrowing more expensive for businesses, potentially leading to lower stock valuations. Additionally, the attractiveness of dividend-paying stocks relative to fixed-income investments can shift. Certain sectors, such as utilities and real estate, which are often more sensitive to borrowing costs, may perform differently in various interest rate environments. Understanding these correlations is vital for diversified investment portfolios.

The Role of Central Bank Communication and Forward Guidance

Central banks increasingly use forward guidance – communication about their future policy intentions – to influence market expectations and manage the transition to new interest rate environments.

Understanding Policy Signals

Paying close attention to the statements, meeting minutes, and press conferences of central bankers provides valuable insights into their economic outlook and potential future policy moves. This information can help individuals and businesses anticipate changes in interest rates and adjust their strategies accordingly. A clear communication strategy from the central bank can help to reduce market volatility and ensure a smoother adjustment to new interest rate levels.

The Influence of Market Expectations

The market often anticipates central bank actions. If a rate hike is widely expected, its impact might be partially priced into financial markets before the official announcement. Conversely, unexpected policy shifts can lead to more significant market reactions. Therefore, understanding not just what the central bank is doing, but what the market expects it to do, is crucial for navigating the evolving interest rate landscape. The constant dialogue between central bank policy and market perception shapes the ongoing narrative of “new interest rates.”