If you have ever applied for a credit card, a car loan, or a mortgage, you have undoubtedly seen the term APR. While most people know it has something to do with the cost of borrowing, many confuse it with a simple interest rate.

Understanding APR is one of the most important steps in managing your personal finances. It allows you to compare different financial products accurately and ensures you aren’t overpaying for debt.

What is APR?

APR stands for Annual Percentage Rate. It represents the total yearly cost of borrowing money, expressed as a percentage.

Unlike a standard interest rate, which only accounts for the cost of the principal balance, the APR provides a more “all-in” picture. It includes the interest rate plus any additional fees or costs associated with the loan (such as origination fees, closing costs, or mortgage insurance).

APR vs. Interest Rate: What’s the Difference?

This is the most common point of confusion for consumers.

- Interest Rate: This is the specific percentage the lender charges you to borrow the principal amount.

- APR: This is the interest rate PLUS any other fees.

Example: Imagine you take out a $10,000 loan with a 5% interest rate. However, the bank charges a $500 processing fee. Because you are paying that extra $500 to get the loan, your actual cost of borrowing is higher than 5%. The APR might end up being 5.8%, reflecting that total cost.

How Does APR Work?

APR works by spreading the total cost of the loan over the entire term. This gives you a standardized number that you can use to compare “Apple A” to “Apple B.”

When you carry a balance on a credit card or pay a monthly mortgage installment, the bank uses the APR to determine how much interest is added to your account.

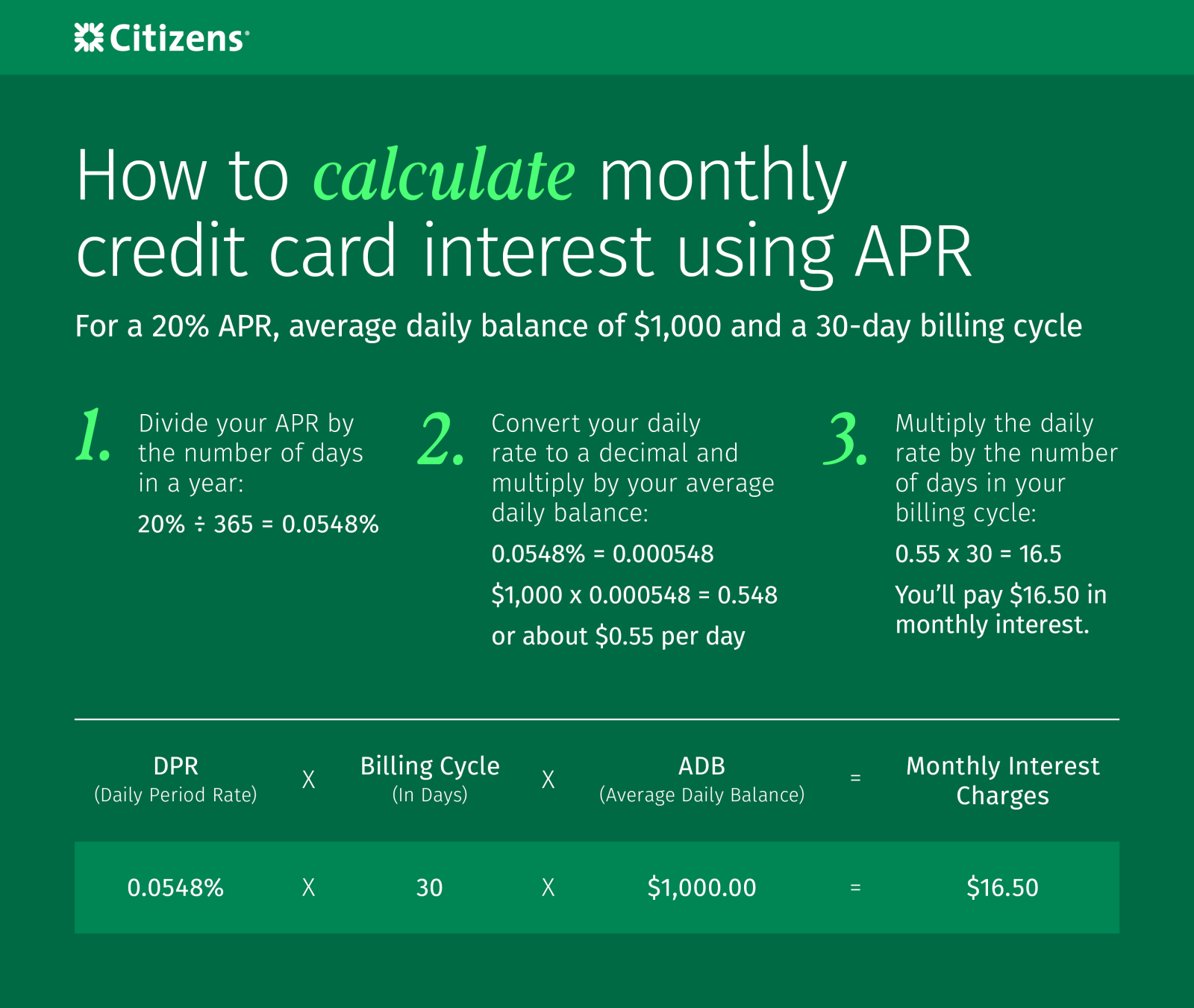

Note on Daily Periodic Rate: Even though APR is an annual rate, most credit card companies calculate interest daily. They do this by dividing your APR by 365 to get the “Daily Periodic Rate,” which is then applied to your average daily balance.

The Different Types of APR

Depending on the financial product, you may encounter different types of APR:

1. Fixed APR

A fixed APR remains the same for the entire life of the loan. This is common in mortgages and auto loans, providing the borrower with predictable monthly payments.

2. Variable APR

A variable APR can change over time based on an underlying index (like the U.S. Prime Rate). Most credit cards have variable APRs, meaning your interest rate could go up or down depending on the economy.

3. Credit Card Specific APRs

Credit cards often have multiple APRs for different types of transactions:

- Purchase APR: The rate applied to standard buys.

- Cash Advance APR: A significantly higher rate for withdrawing cash from an ATM.

- Penalty APR: An increased rate triggered if you make late payments.

- Introductory (0%) APR: A promotional rate offered to new customers for a set period.

Why Does Your APR Matter?

The higher your APR, the more you will pay over the life of the loan.

- Comparison Shopping: If Lender A offers a 4.5% interest rate with $2,000 in fees, and Lender B offers a 4.7% interest rate with $0 fees, the APR will tell you which one is actually cheaper.

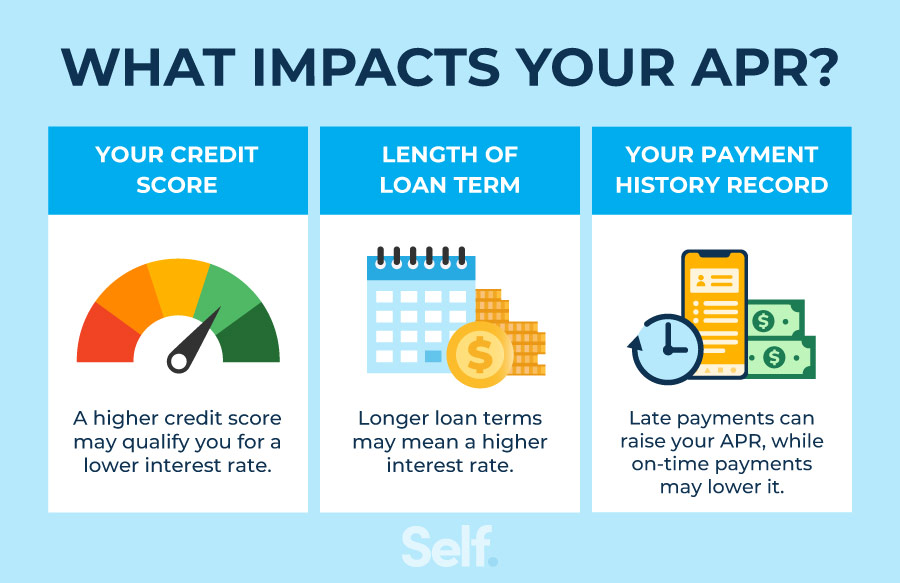

- Credit Score Impact: Generally, the better your credit score, the lower the APR lenders will offer you. A difference of just 1% in APR on a 30-year mortgage can save you tens of thousands of dollars.

How to Lower Your APR

If you find yourself facing high APRs, there are a few ways to lower the cost of your debt:

- Improve your credit score: Pay bills on time and reduce your debt-to-income ratio.

- Negotiate: Sometimes, you can call your credit card issuer and ask for a lower rate if you have been a loyal customer.

- Refinance: If market rates have dropped or your credit has improved, you can take out a new loan with a lower APR to pay off the old one.

Summary

APR is the most accurate tool for measuring the cost of a loan. By looking beyond the sticker-price interest rate and checking the APR, you ensure that you are making the most informed decision possible for your financial future. Always read the fine print to see what fees are being bundled into that percentage.