If you’ve ever opened your pay stub and wondered why the amount deposited into your bank account is significantly lower than the salary mentioned in your job offer, you aren’t alone. Understanding the difference between gross pay and net pay is essential for budgeting and financial planning.

So, the short answer is: Yes, net pay is exactly what you “take home.”

But to understand how your employer gets to that final number, let’s break down the components of your paycheck.

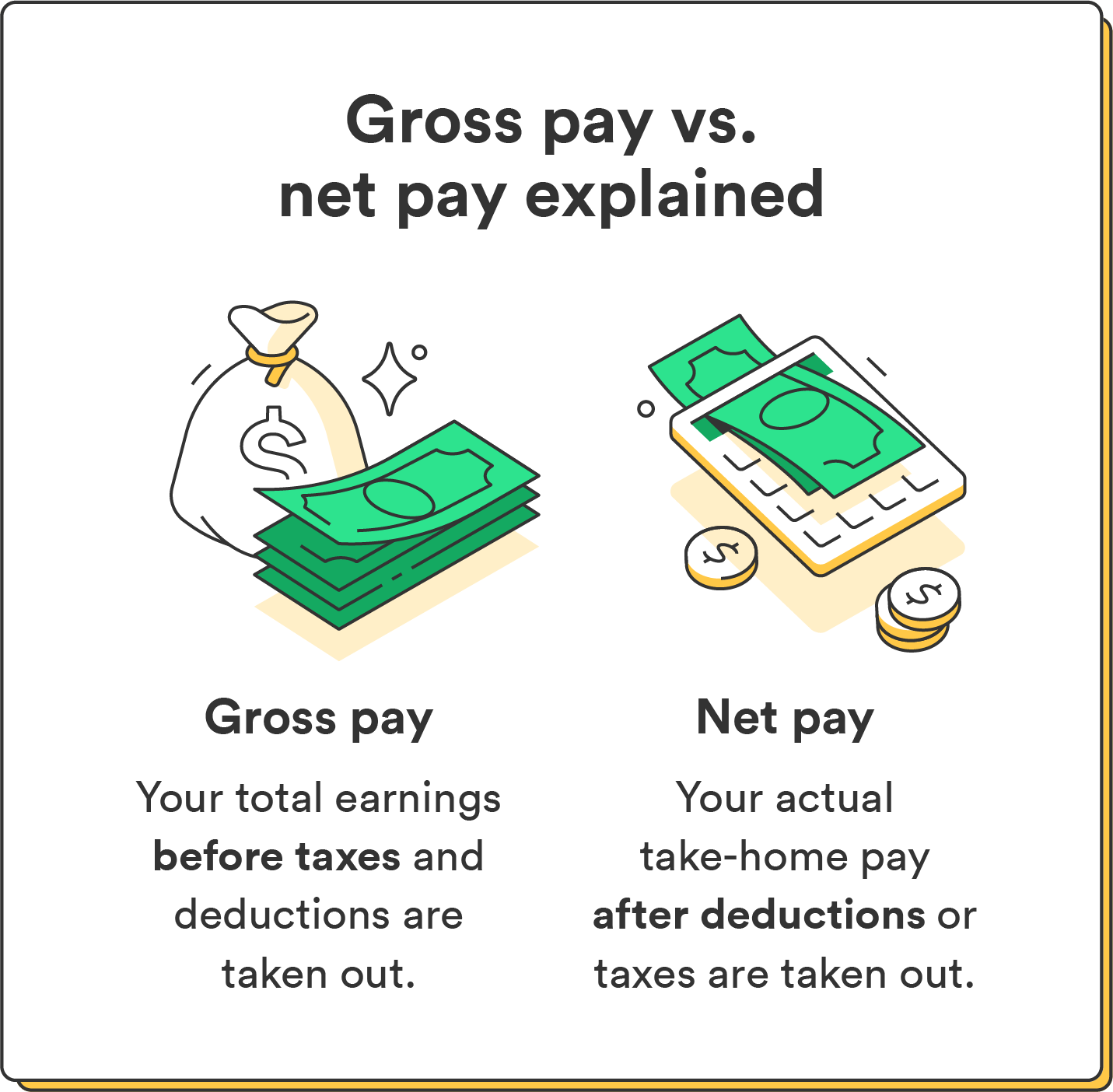

1. Gross Pay vs. Net Pay: What’s the Difference?

To understand your income, you need to know these two fundamental terms:

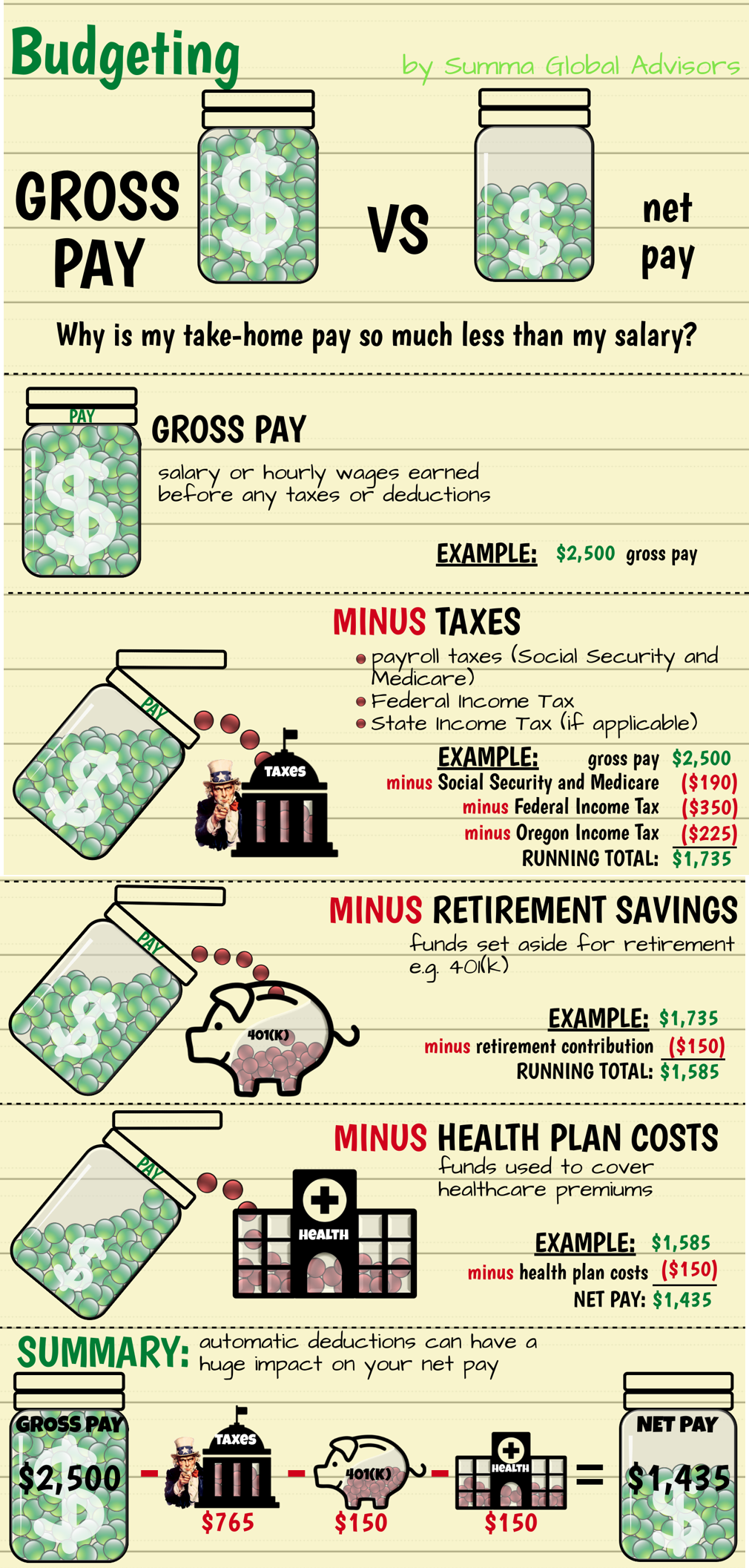

- Gross Pay: This is the total amount of money you earn before any taxes or deductions are taken out. If your salary is $50,000 a year, your monthly gross pay is approximately $4,166.

- Net Pay (Take-Home Pay): This is the amount of money you actually receive in your bank account or via a physical check. It is your gross pay minus all mandatory and voluntary deductions.

The Formula:

Gross Pay – Deductions = Net Pay (Take-Home Pay)

2. Why Is My Net Pay Lower? (Common Deductions)

The “gap” between your gross and net pay is caused by several types of deductions. These generally fall into two categories: Mandatory and Voluntary.

Mandatory Deductions (Required by Law)

- Federal Income Tax: The amount the government takes to fund federal programs. This depends on your income level and the information you provided on your W-4 form.

- State and Local Taxes: Depending on where you live, your state or city may also take a percentage of your income.

- FICA Taxes: This covers Social Security and Medicare. In the U.S., employees typically contribute 6.2% for Social Security and 1.45% for Medicare.

Voluntary Deductions (Chosen by You)

- Health Insurance Premiums: Your share of the cost for medical, dental, or vision insurance.

- Retirement Contributions: Money you choose to put into a 401(k) or 403(b) plan.

- Flexible Spending Accounts (FSA) or HSA: Pre-tax dollars set aside for healthcare or childcare expenses.

- Other Benefits: This could include life insurance, disability insurance, or union dues.

3. Why Knowing Your Net Pay Matters

Understanding your net pay is crucial for several reasons:

- Accurate Budgeting: You cannot build a budget based on your gross salary. You must base your rent, groceries, and savings goals on the money that actually hits your bank account.

- Evaluating Job Offers: When comparing two jobs, look at the benefits packages. A higher gross salary might result in a lower net pay if the second company offers much cheaper health insurance or a better 401(k) match.

- Tax Planning: If your net pay is lower than expected, you may be over-withholding taxes. Conversely, if it’s too high, you might owe money come tax season.

4. How to Calculate Your Take-Home Pay

If you are starting a new job and want to estimate your net pay, follow these steps:

- Determine your Gross Pay for the pay period.

- Subtract Federal and State taxes (you can use online “payroll calculators” for your specific state).

- Subtract FICA taxes (7.65% for most people).

- Subtract your chosen benefits (insurance, retirement).

- The remaining balance is your Net Pay.

Summary

While Gross Pay is the number used to describe your salary during a job interview, Net Pay is the reality of your finances. It is the money available for you to spend, save, and invest. Always check your pay stub regularly to ensure that your deductions are accurate and that you are maximizing your take-home pay.

Do you have questions about your specific pay stub? It’s always a good idea to speak with your company’s HR or Payroll department to clarify any deductions you don’t recognize.