The phrase “what time will my direct deposit hit?” typically refers to the precise moment funds arrive in a bank account. However, in the rapidly evolving landscape of technology and innovation, this question can be re-imagined. It speaks to the imminence and efficiency of processes, the automation that drives them, and the predictability we expect from sophisticated systems. This article delves into the technological advancements that are revolutionizing financial transfers, making them faster, more secure, and increasingly invisible, akin to a perfectly timed “deposit” of information or capability. We will explore the underlying technologies, the current state of play, and the future possibilities that will redefine our understanding of financial accessibility and technological integration.

The Evolution of Automated Financial Transactions: From Batch Processing to Real-Time Systems

The journey of automated financial transactions is a testament to human ingenuity in streamlining complex processes. What was once a manual, time-consuming endeavor has transformed into a sophisticated digital ballet, orchestrated by cutting-edge technology. Understanding this evolution is key to appreciating the speed and reliability of modern financial flows.

The Dawn of Electronic Funds Transfer (EFT)

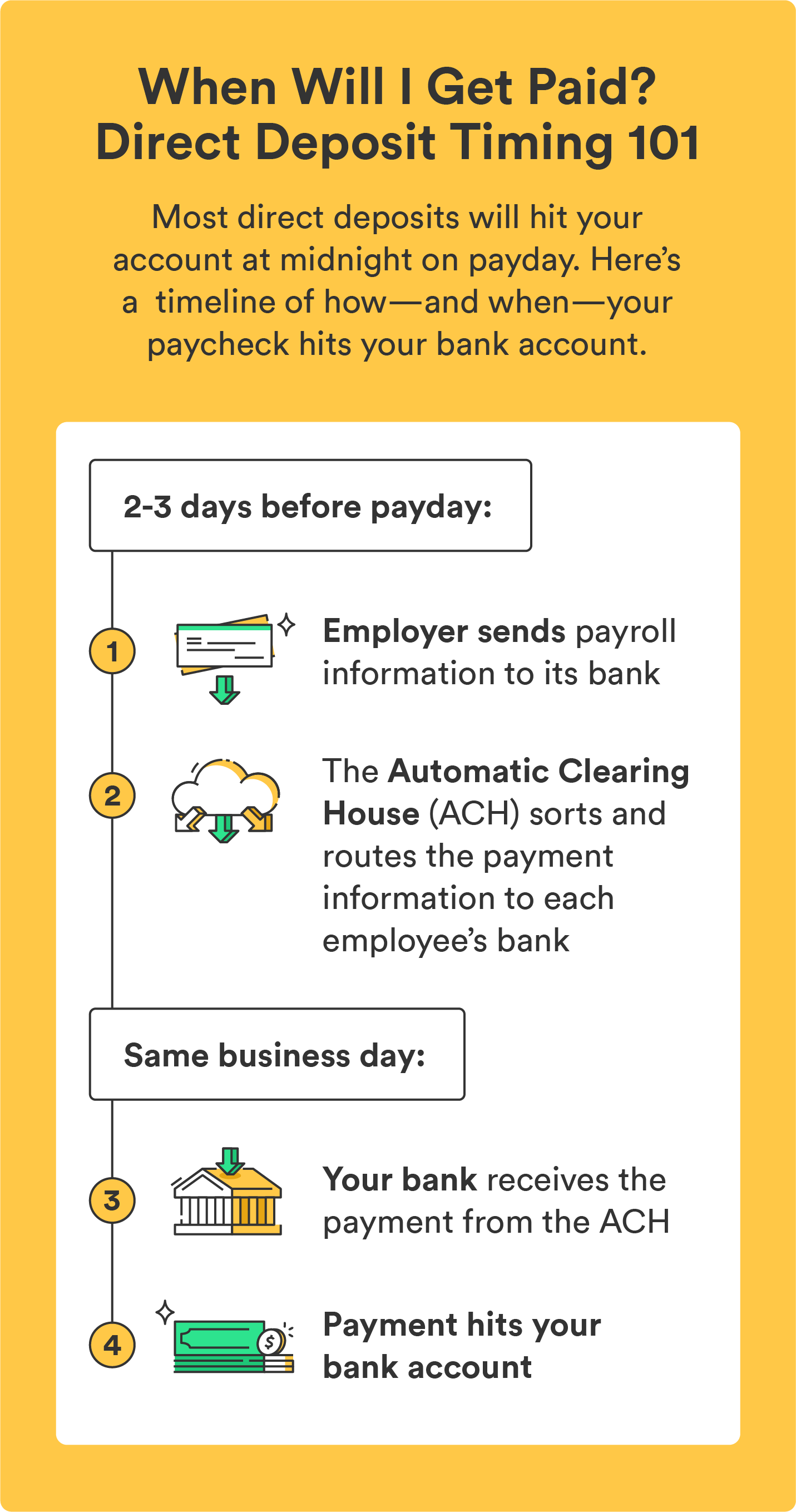

The genesis of direct deposit, and by extension, the concept of a timely financial “hit,” lies in the development of Electronic Funds Transfer (EFT) systems. In the early days, these systems were primarily batch-oriented. This meant that transactions were grouped together and processed at scheduled intervals, often overnight. While a significant leap from paper checks, this still introduced a delay. The “hit” time was dictated by the bank’s processing schedule, not necessarily by the moment the funds were initiated.

Batch Processing and its Limitations

Batch processing, while efficient for handling large volumes, inherently involved a lag. Imagine a scenario where a payroll is processed on a Friday evening. The funds would be initiated then, but due to the batch nature, they might not actually reflect in an employee’s account until Saturday morning or even Monday, depending on the banking institution and the specific EFT network used. This introduced a predictable, yet often inconvenient, waiting period. The technology, while groundbreaking for its time, lacked the real-time responsiveness we now associate with digital immediacy.

The Rise of Real-Time Payments (RTP) and Faster Payment Networks

The demand for instant gratification, fueled by the digital revolution, spurred the development of real-time payment systems. These networks aim to move funds from one account to another in seconds, not hours or days. The technology underpinning RTP is designed for immediate clearing and settlement, allowing for funds to be available almost instantaneously upon initiation.

Technological Enablers of Real-Time Transfers

Several technological advancements have been crucial in enabling RTP. These include:

- API Integration (Application Programming Interfaces): APIs act as the digital conduits that allow different financial systems and applications to communicate seamlessly. For direct deposit, APIs enable payroll processors to directly interface with banking systems, initiating transfers and receiving confirmations in real-time. This eliminates manual data entry and reduces processing times dramatically.

- Cloud Computing: The scalability and agility offered by cloud infrastructure are vital for handling the massive volume and speed of real-time transactions. Cloud-based platforms can adapt to fluctuating demand, ensuring that payment systems remain robust and responsive at all times.

- Advanced Encryption and Security Protocols: As financial data becomes more fluid, robust security is paramount. Modern RTP systems employ sophisticated encryption techniques and multi-factor authentication to protect sensitive financial information and prevent fraud, building trust in the speed and integrity of the system.

- Blockchain Technology (Emerging Applications): While not yet universally adopted for everyday direct deposits, blockchain technology holds significant promise for future financial infrastructure. Its decentralized and immutable ledger system can offer enhanced security, transparency, and potentially even faster settlement times for cross-border transactions and other financial flows.

Understanding the Factors Influencing Direct Deposit Arrival Times

While the ideal scenario is an instant “hit,” the reality of direct deposit arrival times can be influenced by a confluence of factors. These range from the internal processes of financial institutions to external regulatory frameworks and the specific technological choices made by employers.

Employer Payroll Processing Schedules

The primary determinant of when your direct deposit initiates is your employer’s payroll processing schedule. Companies have specific cut-off times for submitting payroll data. If you update your direct deposit information or if your employer initiates payroll on a particular day, it will depend on when they submit that data to their bank.

Cut-off Times and Processing Windows

Most payroll systems operate on a schedule, often processing payroll a few days before the actual payday. For example, if payday is Friday, the payroll might be processed and sent to the bank on Wednesday. The “hit” time then depends on the bank’s processing window for these incoming funds. Understanding your employer’s payroll cycle can provide a good indication of when to expect your funds.

Bank Processing Times and Cut-off Hours

Even with real-time payment networks, individual banks still have internal processing times and cut-off hours. While a transaction might be initiated instantly, its final posting to your account can be subject to these internal workflows.

The Role of Clearing Houses and Settlement Systems

Funds often move through clearing houses and settlement systems before reaching your bank. These intermediaries play a crucial role in reconciling transactions between different financial institutions. The efficiency of these systems, and their operating hours, can introduce minor delays. For example, if a deposit is initiated late in the day, it might be processed in the next business day’s cycle.

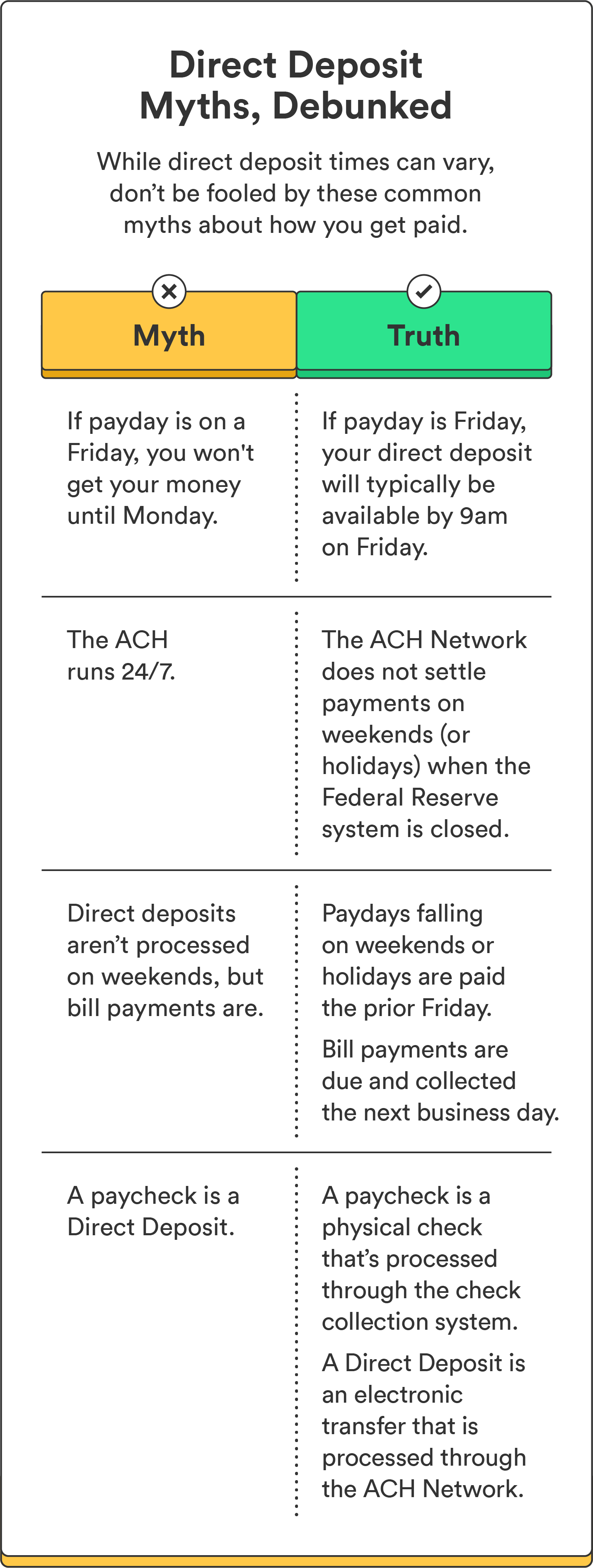

The Impact of Weekends and Holidays

Weekends and public holidays are significant factors that can delay the arrival of direct deposits. Most banking systems do not operate on weekends or holidays, meaning that any transactions initiated on these days will be processed on the next business day.

Business Days vs. Calendar Days

It’s crucial to distinguish between business days and calendar days. While your employer might process payroll on a Friday, if Saturday is a holiday, the funds might not appear in your account until Monday or even Tuesday. This is a common reason for perceived delays, and understanding this distinction can help manage expectations.

The Influence of Banking Technology and Infrastructure

The technological sophistication of both your employer’s bank and your own bank plays a significant role. Banks that have invested heavily in modern payment infrastructure, including real-time processing capabilities and robust API integrations, are more likely to offer faster deposit times.

Legacy Systems vs. Modern Payment Platforms

Institutions still relying on older, legacy banking systems may experience longer processing times. These systems are often less flexible and designed for batch processing. In contrast, banks that have embraced modern payment platforms and APIs can facilitate near-instantaneous transfers, effectively bringing the “hit” time closer to the moment of initiation.

The Future of Direct Deposit: Predictive Technology and Seamless Financial Integration

The trajectory of financial technology points towards a future where direct deposits are not just faster, but also more intelligent and seamlessly integrated into our digital lives. Predictive analytics and advanced automation are poised to redefine our experience, making the question of “what time will it hit?” increasingly irrelevant as transactions become virtually instantaneous and ubiquitous.

Leveraging AI and Machine Learning for Predictive Deposits

Artificial Intelligence (AI) and Machine Learning (ML) are set to revolutionize how financial transactions are managed. These technologies can analyze patterns in spending, income, and financial obligations to predict cash flow needs and proactively manage fund movements.

Proactive Cash Flow Management

Imagine a system that, based on your past spending habits, anticipated bill payments, and regular income, could automatically orchestrate the movement of funds to ensure you never face a shortfall. This could involve pre-emptively moving anticipated direct deposit funds to cover upcoming expenses, or even optimizing savings and investment allocations in real-time. AI could analyze economic indicators and even your personal calendar to anticipate when funds will be needed and ensure they are readily available.

The Rise of Embedded Finance and Invisible Transactions

The concept of embedded finance refers to the integration of financial services directly into non-financial platforms and applications. This trend is making financial transactions increasingly invisible, occurring in the background without requiring active user intervention.

Seamless User Experiences

In the future, direct deposits might not even be a concept you actively think about. As services become more integrated, your income could be automatically distributed to various accounts – a primary checking account, investment portfolios, or even for loan repayments – the moment it’s received, without any manual action on your part. This “invisible banking” leverages robust APIs and data analytics to ensure funds are allocated precisely where and when they are needed.

Enhanced Security Through Biometrics and Decentralized Ledgers

As financial transactions become more immediate and automated, security remains paramount. Future advancements will likely see the integration of more sophisticated security measures.

Biometric Authentication and Decentralized Finance (DeFi)

Biometric authentication (fingerprint, facial recognition) is already becoming commonplace for accessing financial accounts. In the future, it could be integral to authorizing even micro-transactions. Furthermore, the principles of decentralized finance (DeFi), built on blockchain technology, offer potential for greater transparency, reduced reliance on intermediaries, and enhanced security through distributed ledger systems. While still nascent for direct deposits, these technologies represent a significant shift towards a more secure and potentially faster financial future.

The question of “what time will my direct deposit hit?” is evolving. It’s moving from a query about a specific moment in time to a broader appreciation of the technological sophistication that underpins our financial infrastructure. As we witness the continuous innovation in payment systems, AI, and embedded finance, the certainty of timely financial access will become less about waiting and more about seamless, intelligent automation. The future of financial transactions is not just about speed; it’s about a more integrated, secure, and intuitive experience, where your funds are precisely where they need to be, exactly when they need to be there.