Navigating the complexities of retirement savings, particularly the 401(k) plan, is a crucial aspect of long-term financial planning. While designed for future security, unforeseen circumstances can arise, prompting individuals to consider accessing these funds before retirement age. This is where the concept of a “hardship withdrawal” comes into play. Understanding what constitutes a qualifying hardship is paramount, as misinterpretations can lead to unexpected penalties and taxes, jeopardizing your financial future. This article delves into the intricacies of 401(k) hardship withdrawals, outlining the criteria, procedures, and important considerations to help you make informed decisions.

Understanding the Purpose and Restrictions of 401(k) Hardship Withdrawals

A 401(k) plan is a powerful tool for accumulating wealth for retirement. The funds contributed are intended to grow tax-deferred, providing a substantial nest egg for your later years. Because of this preferential tax treatment and the long-term nature of the investment, accessing these funds before retirement is generally discouraged and subject to strict rules. Hardship withdrawals are an exception to this rule, designed to offer relief during genuinely dire financial emergencies.

The Importance of Preservation for Retirement

The primary objective of a 401(k) is to provide financial security during retirement. When individuals withdraw funds prematurely, they not only lose the immediate capital but also forfeit the potential for future growth that those funds could have generated. Compounding, the process by which earnings generate their own earnings, is a cornerstone of long-term wealth accumulation. Early withdrawals interrupt this crucial growth cycle, significantly impacting the size of the retirement nest egg. For instance, withdrawing $10,000 at age 40 that could have grown at an average annual rate of 7% for 25 years would mean a loss of over $50,000 in potential retirement funds. This illustrates why regulatory bodies and plan administrators impose stringent conditions on hardship withdrawals.

Defining a “Hardship” Under IRS Guidelines

The Internal Revenue Service (IRS) provides the foundational definitions for what constitutes a hardship withdrawal. Generally, a hardship withdrawal is permitted only for “an immediate and heavy financial need” of the employee, and the amount withdrawn must be “not more than the amount of the need.” This means that the need must be pressing and the withdrawal should be limited to the exact amount required to address the specific emergency. The IRS has identified several categories of expenses that are typically considered qualifying hardships. It’s important to note that not all expenses that feel like a hardship to an individual will necessarily meet the IRS definition.

Qualifying Hardship Events: Specific Circumstances Permitted

The IRS has outlined specific situations that are generally recognized as qualifying hardship events. These are typically situations where an individual faces significant and unavoidable expenses or losses. It’s crucial to understand that the employer’s 401(k) plan document will detail the specific hardships they recognize, and while these generally align with IRS guidelines, there can be subtle differences. Always consult your plan administrator for the most accurate information regarding your specific plan.

Medical Expenses

One of the most commonly recognized hardship events is the need to pay for certain medical expenses. This can include costs for the employee, their spouse, dependents, or even beneficiaries. The IRS generally allows hardship withdrawals for expenses incurred for:

- Diagnosis, cure, mitigation, treatment, or prevention of disease: This covers a broad range of medical treatments and procedures.

- Accident or illness: This includes expenses related to sudden and unexpected medical conditions.

- Disability: Expenses related to a diagnosed disability.

Crucially, these medical expenses must not be covered by insurance. This means you must have exhausted any available health insurance benefits before seeking a hardship withdrawal for medical costs. Furthermore, the withdrawal should only cover the amount of the medical expenses that are not reimbursed by other sources.

Education Expenses

Another category of qualifying hardship involves expenses related to post-secondary education. This typically refers to tuition, fees, and other necessary costs for courses taken at an eligible educational institution for:

- The employee: For their own continued education.

- The employee’s spouse: For their educational pursuits.

- The employee’s dependents: For their college or university expenses.

Similar to medical expenses, the withdrawal should only cover the amount needed for tuition and other essential educational costs for the current academic period. It’s important to verify with your plan administrator what constitutes an “eligible educational institution” and what specific costs are permissible. General costs of living or non-essential educational supplies may not qualify.

Expenses Related to Preventing Eviction or Foreclosure

Protecting one’s primary residence is a significant concern, and the IRS recognizes this by allowing hardship withdrawals to prevent imminent loss of housing. This can include:

- Eviction from your principal residence: If you are facing eviction due to non-payment of rent, a hardship withdrawal may be permissible to cover the back rent owed.

- Foreclosure on your principal residence: If you are at risk of losing your home through foreclosure due to missed mortgage payments, a hardship withdrawal can be used to cover the overdue mortgage payments.

The key here is “imminent.” This means there must be a genuine and immediate threat of losing your home. You will likely need to provide documentation demonstrating this threat, such as eviction notices or foreclosure warnings. The withdrawal should be limited to the amount necessary to prevent the eviction or foreclosure.

Other Qualifying Hardship Events (Plan-Specific)

While the IRS specifies core hardship categories, some 401(k) plans may allow for additional qualifying events, often referred to as “deemed” hardships. These are often less common but can provide crucial relief in specific situations. These may include:

- Funeral expenses: Costs associated with the death of a spouse, dependent, or other family member. This is often a time of significant financial strain, and the IRS may allow withdrawals to cover these immediate costs.

- Disaster relief: Expenses incurred due to a federally declared disaster affecting your principal residence, such as damage from a hurricane, earthquake, or flood. This aims to help individuals rebuild and recover from catastrophic events.

- Victim of domestic violence: In some cases, plans may allow for withdrawals to help victims of domestic violence escape abusive situations, which can involve significant relocation and safety expenses.

It is imperative to consult your 401(k) plan’s Summary Plan Description (SPD) or speak directly with your plan administrator to understand the full scope of what your specific plan considers a qualifying hardship.

The Application Process and Required Documentation

Requesting a hardship withdrawal is not as simple as making a phone call. It involves a formal application process with your 401(k) plan administrator and requires substantial documentation to substantiate your claim. This process is designed to ensure that withdrawals are made only for legitimate hardship reasons and to prevent misuse of retirement funds.

Submitting a Formal Request and Plan Administrator Review

The first step in initiating a hardship withdrawal is to formally request it from your 401(k) plan administrator. This typically involves obtaining and completing a specific hardship withdrawal application form provided by the plan. This form will ask for detailed information about your financial situation, the nature of the hardship, and the amount you are requesting.

Once submitted, the plan administrator will review your application to determine if it meets the criteria for a hardship withdrawal as defined by the IRS and your specific plan document. They will assess the validity of your claim and the amount requested against the available documentation. This review process can take some time, so it’s advisable to be prepared for a waiting period.

Essential Documentation to Substantiate Your Claim

The success of your hardship withdrawal request hinges on the quality and completeness of the documentation you provide. Without proper substantiation, your request is likely to be denied. The specific documents required will vary depending on the nature of your claimed hardship, but generally include:

-

Proof of the Hardship Event:

- Medical Expenses: Medical bills, hospital statements, invoices from healthcare providers, and documentation showing that insurance did not cover the expenses (e.g., Explanation of Benefits statements).

- Education Expenses: Invoices from the educational institution, enrollment verification, and proof of tuition and fees.

- Eviction/Foreclosure: Copies of eviction notices, foreclosure warnings, lease agreements, mortgage statements showing overdue payments, and documentation of communication with landlords or lenders.

- Funeral Expenses: Death certificates, funeral home invoices, and burial or cremation costs.

- Disaster Relief: Documentation of the disaster (e.g., FEMA declaration), repair estimates, or receipts for essential rebuilding supplies.

-

Proof of Income and Financial Need:

- Pay stubs, bank statements, and tax returns may be required to demonstrate your current financial situation and the extent of your need.

- A sworn statement or affidavit explaining the circumstances of the hardship and why the withdrawal is necessary may also be requested.

-

Amount Requested Justification:

- Detailed breakdown of the costs you intend to cover with the withdrawal, clearly linking them to the hardship event. For example, if it’s for medical bills, list each bill and its amount. If it’s for back rent, show the total rent owed and the period it covers.

It is crucial to gather all relevant documentation before submitting your application. Incomplete applications are a common reason for denial. Your plan administrator can provide a detailed list of the specific documents they require for each type of hardship.

The Consequences of Hardship Withdrawals: Taxes and Penalties

While hardship withdrawals offer a lifeline during emergencies, they come with significant financial implications that individuals must be prepared for. These consequences are designed to discourage premature access to retirement savings and to recoup some of the tax benefits that were provided.

Income Tax Liability

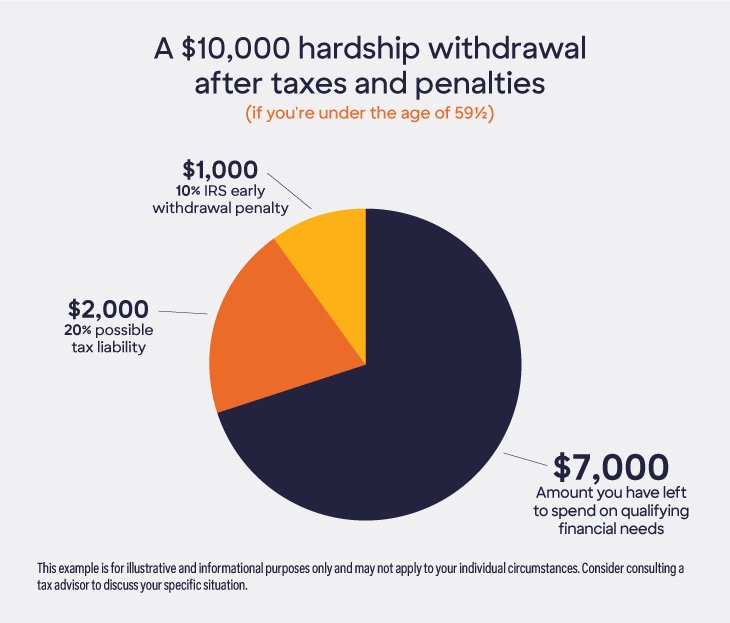

Hardship withdrawals are considered taxable income in the year they are taken. This means that the amount you withdraw will be added to your gross income and taxed at your ordinary income tax rate. The IRS does not allow for the deferral of taxes on hardship withdrawals. This can lead to a substantial tax bill, potentially pushing you into a higher tax bracket for that year. For example, withdrawing $15,000 could result in thousands of dollars in additional income taxes, depending on your overall income.

Early Withdrawal Penalties

In addition to income taxes, withdrawals made before age 59½ are generally subject to a 10% early withdrawal penalty imposed by the IRS. This penalty is applied to the taxable portion of the withdrawal. Therefore, if you withdraw $15,000 and it’s all taxable, you could face an additional $1,500 penalty. This penalty is intended to further discourage early access to retirement funds.

There are some limited exceptions to the 10% early withdrawal penalty, even for hardship withdrawals. For instance, if you are separating from service in the year you turn 55 or older, the 10% penalty may not apply to those withdrawals. However, these exceptions are specific and should be confirmed with a tax advisor or your plan administrator.

Impact on Your Retirement Savings

As previously mentioned, the most profound consequence of a hardship withdrawal is the direct reduction of your retirement savings. Not only do you lose the principal amount withdrawn, but you also lose all the potential future earnings that money could have generated. This can have a compounding negative effect on your retirement security, potentially requiring you to work longer or adjust your retirement lifestyle significantly. It’s essential to view a hardship withdrawal as a last resort, after exhausting all other available financial resources.

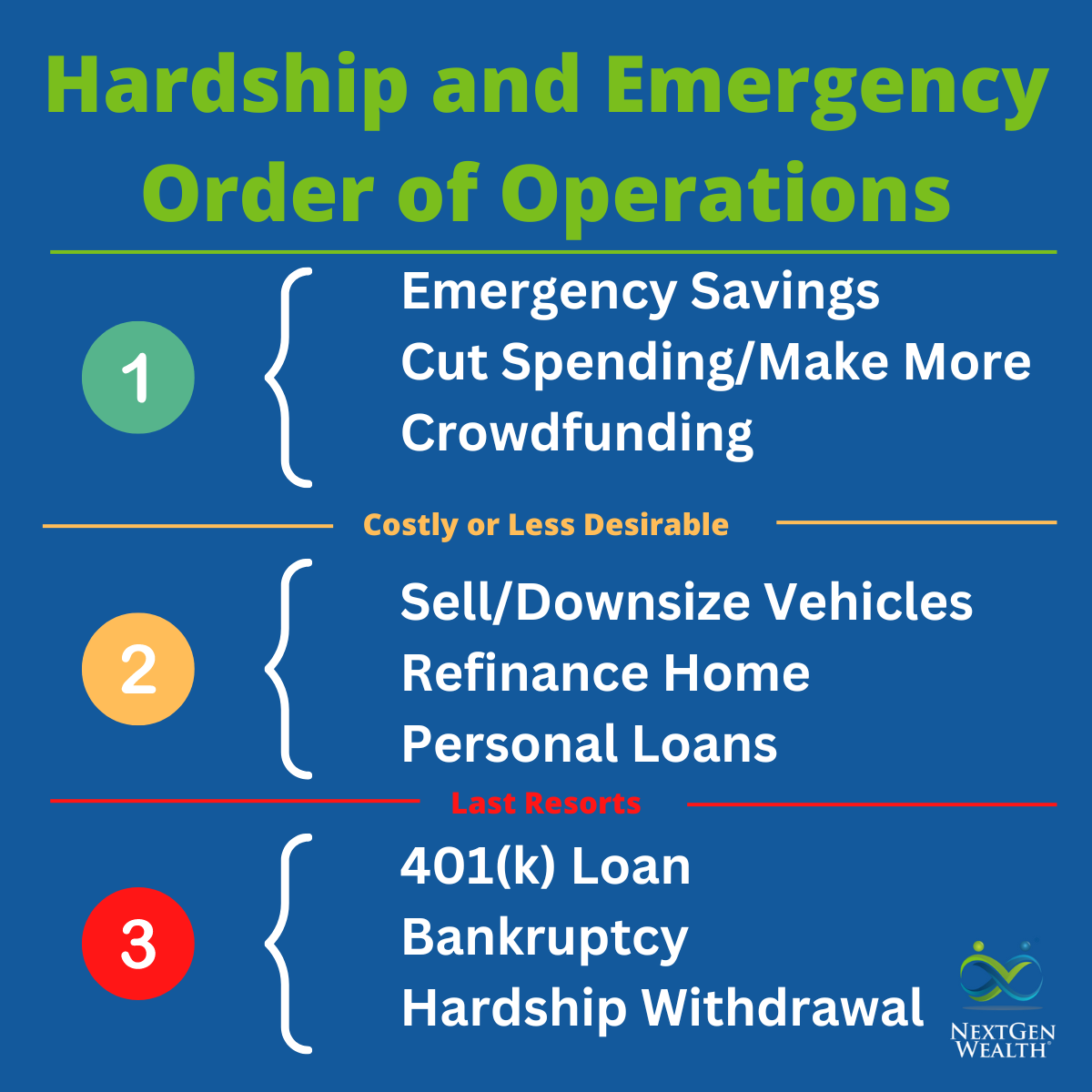

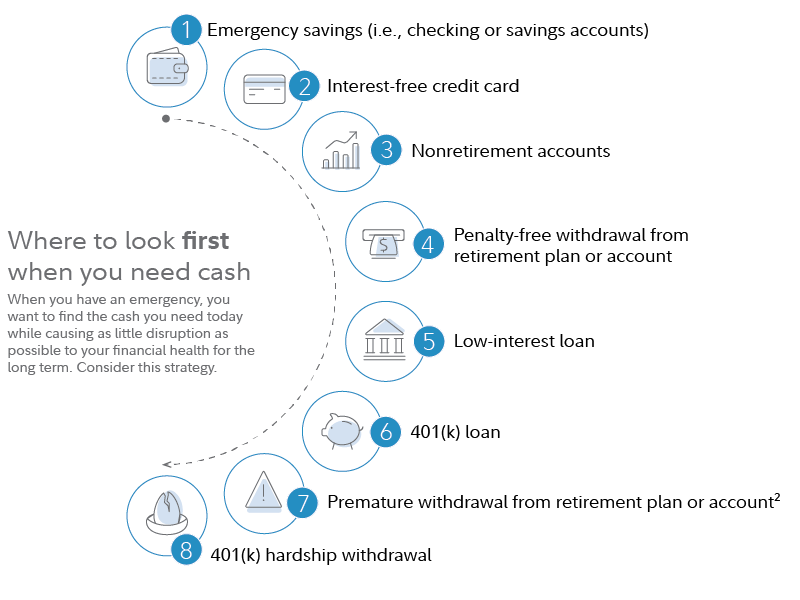

Alternatives to Hardship Withdrawals: Exploring Other Options

Before resorting to a hardship withdrawal, it is strongly advisable to explore all other available financial avenues. Hardship withdrawals should be considered only when all other options have been exhausted, due to their immediate tax and penalty implications and the long-term impact on your retirement savings.

Loans from Your 401(k) Plan

Many 401(k) plans offer the option of taking a loan against your vested balance. A 401(k) loan allows you to borrow money from your own retirement account, which you then repay with interest back into your account. The interest you pay goes back to your account, so you are essentially paying yourself.

Key advantages of 401(k) loans include:

- No immediate tax liability: Loan proceeds are not considered taxable income at the time of disbursement.

- No early withdrawal penalty: You avoid the 10% penalty typically associated with early withdrawals.

- Reasonable interest rates: Interest rates are generally competitive.

However, there are important considerations:

- Repayment is mandatory: Loans typically must be repaid within five years (or longer for loans to purchase a primary residence), and failure to do so can result in the outstanding balance being treated as a taxable withdrawal and subject to the 10% penalty.

- Lost growth potential: While you’re repaying yourself, the money borrowed is not invested and therefore not earning potential market returns during the loan period.

- Impact of job loss: If you leave your employer before repaying the loan, the outstanding balance may become due immediately or be treated as a taxable distribution.

Other Savings and Investment Accounts

Before considering your 401(k), assess all other liquid assets you may have. This could include:

- Savings accounts and money market accounts: These offer easy access to funds with no penalties or taxes.

- Taxable brokerage accounts: Investments in these accounts can be sold, though capital gains taxes may apply if you sell at a profit.

- Emergency funds: If you have an established emergency fund, this is precisely what it’s intended for.

Personal Loans and Lines of Credit

Consider exploring personal loans from banks or credit unions, or utilizing existing lines of credit. While these may have interest rates, they do not jeopardize your long-term retirement savings in the same way a hardship withdrawal does. The terms and interest rates will vary, so compare options carefully.

Family and Friends

In some situations, borrowing from family or trusted friends might be an option. While this can be a sensitive topic, it can offer a more flexible and interest-free solution in a true emergency.

Government Assistance Programs

Depending on the nature of your hardship, you might be eligible for government assistance programs, such as unemployment benefits, food stamps, or housing assistance. Researching these options could provide crucial support without impacting your retirement funds.

In conclusion, understanding the stringent criteria for 401(k) hardship withdrawals is essential. While they offer a safety net during genuine financial emergencies, the associated taxes, penalties, and long-term impact on retirement savings necessitate careful consideration and the exploration of all alternative financial resources first. Always consult with your plan administrator and a qualified financial advisor to make the most informed decision for your unique circumstances.