While the term “company” often conjures images of bustling corporate offices, shareholder meetings, and publicly traded stocks, the legal landscape of business structures is far more varied. One fundamental distinction lies between incorporated and unincorporated entities. Understanding what an unincorporated company is—and what it is not—is crucial for entrepreneurs, investors, and anyone navigating the business world. At its core, an unincorporated company refers to a business that has not undergone the formal legal process of incorporation, meaning it is not recognized as a separate legal entity distinct from its owners. This fundamental difference has profound implications for liability, taxation, ownership, and operational flexibility.

The Nature of Unincorporated Business Structures

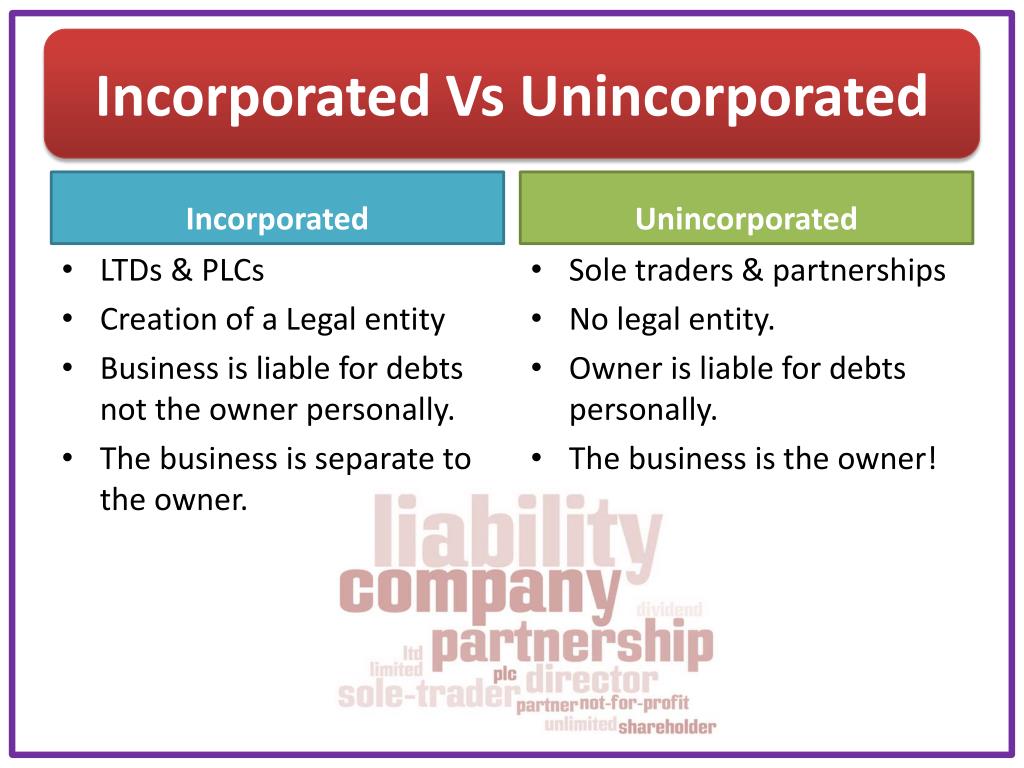

The defining characteristic of an unincorporated company is the absence of a legal separation between the business and its proprietor(s). This lack of distinct legal personhood shapes how the business operates, how its finances are managed, and how its liabilities are handled. Unlike an incorporated entity, which can enter into contracts, own property, and sue or be sued in its own name, an unincorporated business is essentially an extension of its owner(s).

Sole Proprietorships: The Simplest Form

The most common and straightforward example of an unincorporated company is a sole proprietorship. This business structure is owned and run by one individual, and there is no legal distinction between the owner and the business. All profits and losses are reported on the owner’s personal tax return. The proprietor has complete control over the business, making all decisions and retaining all profits. However, this absolute control comes with unlimited personal liability. If the business incurs debts or faces lawsuits, the owner’s personal assets—such as their home, car, and savings—are at risk. This is a critical point of distinction from incorporated entities, where the liability of the owners is generally limited to their investment in the company.

Partnerships: Shared Ownership, Shared Risk

A partnership is another prevalent form of unincorporated business. In a partnership, two or more individuals agree to share in the profits or losses of a business. Like sole proprietorships, partnerships are not separate legal entities. This means that the partners are personally liable for the debts and obligations of the business. If one partner incurs a debt or is sued, all partners can be held responsible, potentially jeopardizing their personal assets. There are different types of partnerships, such as general partnerships where all partners share in management and liability, and limited partnerships, which have at least one general partner with unlimited liability and one or more limited partners whose liability is limited to their investment. However, even in limited partnerships, the general partner(s) remain personally exposed.

Other Unincorporated Forms: Less Common but Relevant

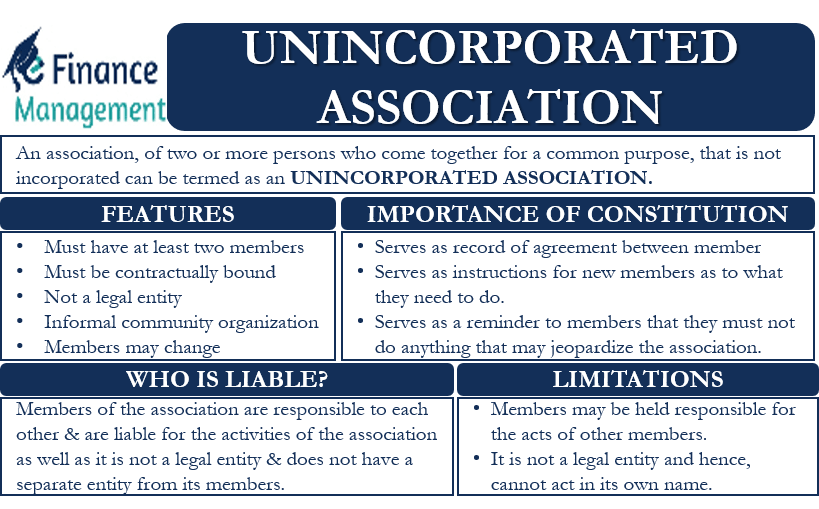

While sole proprietorships and general partnerships are the most frequently encountered unincorporated structures, other forms exist. For instance, unincorporated associations are groups of individuals who have banded together for a common purpose but have not formed a legal entity. These are often non-profit organizations, clubs, or societies. Similarly, trusts, while having specific legal structures, can sometimes operate in an unincorporated manner, with the trustees holding and managing assets on behalf of beneficiaries. The key unifying factor across these diverse forms is the lack of formal incorporation as a distinct legal entity.

Implications of Being Unincorporated

The decision to operate as an unincorporated company carries significant consequences that impact various facets of the business. These implications primarily revolve around liability, taxation, fundraising, and administrative burden. Understanding these downstream effects is vital for making informed strategic decisions.

Unlimited Personal Liability: The Double-Edged Sword

The most significant implication of being an unincorporated company is unlimited personal liability. This means that the owners are personally responsible for all business debts, obligations, and legal judgments. If the business fails to pay its creditors, faces a lawsuit, or incurs significant financial losses, the owner’s personal assets are on the line. This can include their home, savings accounts, vehicles, and any other personal property. For a sole proprietor, this is a direct risk. For partners, it means that each partner’s personal assets are exposed to the business’s liabilities, and potentially to the liabilities created by other partners. This lack of a protective shield is a primary reason why many businesses opt for incorporation as they grow and their risk exposure increases.

Taxation: Simplicity vs. Potential Disadvantage

Taxation for unincorporated companies is generally simpler than for their incorporated counterparts. Profits and losses are typically passed through directly to the owners and reported on their individual income tax returns. This “pass-through taxation” avoids the potential for “double taxation” that can occur with C-corporations, where profits are taxed at the corporate level and then again when distributed to shareholders as dividends. However, this simplicity can sometimes be a disadvantage. For businesses with significant profits, the individual income tax rates might be higher than corporate tax rates, leading to a greater overall tax burden. Furthermore, owners of unincorporated businesses often have to pay self-employment taxes (Social Security and Medicare) on their entire net earnings, whereas employees of corporations have these taxes split with their employer.

Operational Flexibility and Control

One of the advantages of an unincorporated structure is the inherent operational flexibility and direct control it affords the owner(s). With fewer formalities and reporting requirements compared to incorporated entities, decision-making can be quicker and more agile. Owners can easily access business funds for personal use (though this should be carefully managed to avoid commingling funds, which can blur legal lines). This direct control is particularly appealing to entrepreneurs who want to maintain complete autonomy over their business operations and strategy. There are no boards of directors to answer to, no shareholder meetings to convene, and fewer regulatory hurdles to navigate in day-to-day management.

Fundraising Challenges

Raising capital can be more challenging for unincorporated companies compared to incorporated ones. Investors, particularly venture capitalists and angel investors, often prefer to invest in corporations because the structure provides a clear framework for ownership, equity distribution, and investor protections. The limited liability offered by incorporation also makes it more attractive for external funding. Unincorporated businesses may have to rely more heavily on personal savings, loans from friends and family, or traditional bank loans, which can have stricter collateral requirements. Selling ownership stakes in an unincorporated business can also be more complex due to the lack of standardized share structures.

The Process and Benefits of Incorporation

Given the limitations and risks associated with unincorporated business structures, many entrepreneurs eventually consider incorporating their businesses. Incorporation is the legal process of creating a distinct corporate entity, separate from its owners. This process involves filing specific documents with the relevant state government agency and adhering to a set of legal and regulatory requirements. The benefits of this transformation are substantial and often outweigh the initial administrative effort.

Creating a Separate Legal Entity

The primary outcome of incorporation is the creation of a separate legal entity. This means the corporation can enter into contracts, own assets, incur debts, and sue or be sued in its own name. This separation is the foundation for many of the advantages of incorporation, most notably limited liability. The corporation itself is responsible for its debts and obligations, shielding the personal assets of its owners (shareholders) from business liabilities. This distinction is fundamental and provides a crucial layer of protection for individuals involved in commercial enterprises.

Limited Liability Protection

As mentioned, limited liability is perhaps the most significant benefit of incorporation. Shareholders in a corporation are generally only liable for the amount they have invested in the company. If the corporation faces financial difficulties, declares bankruptcy, or is sued, the personal assets of the shareholders are protected. This is a critical distinction from unincorporated businesses where personal assets are directly exposed. This protection encourages investment and allows businesses to take on greater financial risks necessary for growth and innovation without jeopardizing the personal wealth of their owners.

Enhanced Credibility and Fundraising Potential

Incorporation can significantly enhance a business’s credibility and its ability to attract investment. A formal corporate structure signals a level of seriousness, stability, and professionalism to potential investors, lenders, and customers. Investors, especially institutional ones, often have mandates that restrict them from investing in unincorporated entities. Furthermore, incorporated businesses can issue stock, providing a clear mechanism for raising capital through equity financing. This ability to sell ownership stakes in defined units (shares) simplifies the process of attracting external funding and can fuel substantial business expansion.

Tax Advantages and Benefits

While the tax implications of incorporation can be complex, there are potential advantages. As previously noted, C-corporations may benefit from lower corporate tax rates compared to high individual income tax rates. Additionally, incorporated businesses can offer more comprehensive employee benefits, such as health insurance and retirement plans, which can be tax-deductible for the corporation. There are also opportunities for strategic tax planning and the ability to retain earnings within the corporation for future reinvestment, potentially deferring personal income tax liabilities. However, it is crucial to consult with tax professionals to determine the most advantageous corporate structure and tax strategy for a specific business.

When is an Unincorporated Structure Appropriate?

Despite the inherent risks, unincorporated business structures remain a viable and even preferable choice for certain types of businesses and entrepreneurs. The decision hinges on a careful assessment of the business’s risk profile, growth trajectory, and the owner’s personal financial situation and risk tolerance.

Early-Stage Businesses and Solopreneurs

For many individuals starting a new venture, especially those operating as solopreneurs or with a very low-risk business model, an unincorporated structure can be ideal. The simplicity of setup, minimal administrative overhead, and direct control are highly attractive in the nascent stages of a business. For example, a freelance graphic designer, a writer offering services, or a small online retailer with minimal inventory and low overhead might find the ease of a sole proprietorship perfectly suited to their needs. The focus can remain squarely on building the business without being burdened by complex corporate formalities.

Businesses with Low Financial Risk and Minimal Debt

If a business model inherently involves low financial risk, minimal debt, and a limited potential for lawsuits, the unlimited liability of an unincorporated structure may be less of a deterrent. A small consulting firm with few employees and no significant physical assets, for instance, might operate for years without encountering major liability issues. In such cases, the administrative simplicity and direct control offered by a sole proprietorship or partnership might be sufficient. However, even in these scenarios, it is prudent to consider the potential for unforeseen events.

Testing Business Concepts and Side Hustles

Unincorporated structures are often used for “side hustles” or for testing out new business ideas before committing to the more formal and potentially costly process of incorporation. This allows entrepreneurs to explore their market, develop their product or service, and generate initial revenue with minimal upfront investment in legal and administrative setup. If the venture proves successful and shows potential for significant growth and increased risk, the entrepreneur can then transition to an incorporated structure. This phased approach allows for flexibility and minimizes initial commitment.

The Importance of Legal and Financial Advice

Regardless of the chosen business structure, seeking professional legal and financial advice is paramount. An experienced attorney can explain the nuances of different business entities, help with the formation process, and draft essential agreements. A qualified accountant or tax advisor can guide entrepreneurs through the tax implications of each structure, assist with compliance, and help optimize tax strategies. For unincorporated businesses, this advice is crucial for understanding the personal liability implications and for ensuring that personal and business finances are kept as separate as practically possible to maintain clear distinctions, even in the absence of formal legal separation. Making an informed decision about business structure is a foundational step towards long-term success and security.