The world of travel and accommodation is multifaceted, and understanding the various components that contribute to its economic and regulatory framework is crucial for both travelers and businesses. One such component, often encountered but not always fully understood, is the Transient Occupancy Tax (TOT). This tax, levied by local governments, plays a significant role in funding public services and infrastructure within communities. This article delves into the intricacies of TOT, exploring its definition, purpose, administration, and impact.

Understanding the Fundamentals of Transient Occupancy Tax

At its core, Transient Occupancy Tax is a tax imposed on individuals who occupy lodging for a short period. This distinction between “transient” and “permanent” occupancy is key to understanding the tax’s application. It is a local tax, meaning its rates, rules, and regulations can vary significantly from one city, county, or state to another.

![]()

Defining “Transient Occupancy”

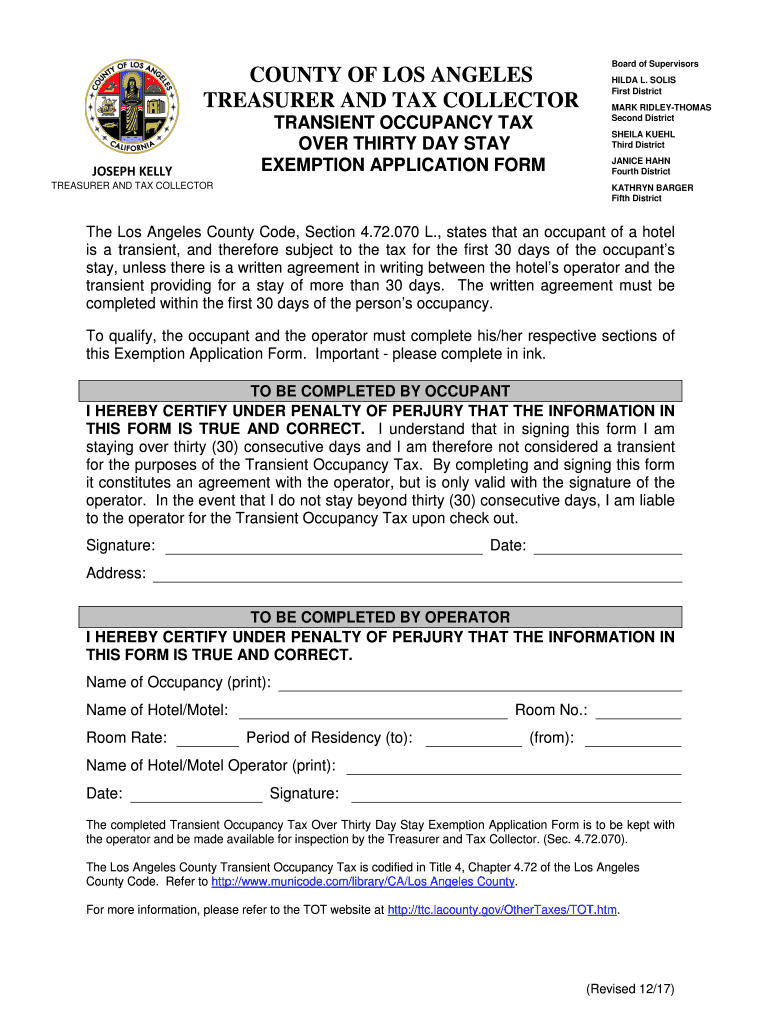

The term “transient occupancy” typically refers to the use or possession of any hotel, motel, inn, or other lodging establishment by a person who stays for less than a continuous period of 30 days. This definition is a cornerstone of TOT legislation. The “30-day rule” is a common benchmark, but it’s important to note that some jurisdictions may have different thresholds or specific exceptions. For instance, certain long-term rental agreements might be exempt, while others might still be subject to TOT if they don’t meet the strict definition of a permanent residence.

The rationale behind this 30-day distinction is that individuals staying for longer periods are generally considered residents and are therefore subject to different tax structures, such as property taxes or standard sales taxes on rent. Transient stays, on the other hand, are seen as temporary and are often associated with tourism, business travel, or short-term visits, where the immediate community is providing services and infrastructure that benefit these temporary visitors.

The Purpose and Rationale Behind TOT

Local governments levy TOT for several critical reasons, primarily centered around generating revenue to support services that benefit both residents and visitors. The revenue generated from TOT is often earmarked for specific purposes, contributing to the vibrancy and functionality of the community.

Funding Local Services and Infrastructure

A significant portion of TOT revenue is typically allocated to enhance and maintain public services. This can include funding for local police and fire departments, parks and recreation facilities, public transportation, libraries, and cultural attractions. In tourist-dependent economies, TOT can be a vital source of funding that directly supports the amenities and infrastructure that attract visitors in the first place. For example, revenue might be used to improve beaches, maintain historical sites, or enhance event venues.

Supporting Tourism and Economic Development

Many jurisdictions use TOT revenue to directly promote tourism and support economic development initiatives. This can involve funding marketing campaigns to attract visitors, supporting local tourism bureaus, or investing in infrastructure projects that improve the visitor experience, such as convention centers or improved signage. By investing in these areas, communities aim to create a more attractive destination, leading to increased visitor spending and further economic benefits.

Mitigating the Impact of Tourism

While tourism brings economic benefits, it can also place a strain on local resources and infrastructure. TOT can be seen as a way to help mitigate these impacts. The revenue generated can help offset the costs associated with increased demand for public services, wear and tear on public facilities, and other externalities associated with a higher volume of visitors.

Key Players and Administration of TOT

The administration and collection of TOT involve several key entities, each with distinct roles and responsibilities. Understanding these players is crucial for both lodging providers and travelers.

Lodging Providers as Tax Collectors

For the most part, lodging providers—hotels, motels, short-term rental platforms, and similar businesses—act as the primary collectors of TOT. They are responsible for calculating the correct tax amount based on the room rate and applicable local tax rates, collecting this tax from their guests at the time of payment, and remitting it to the appropriate government agency. Failure to collect and remit TOT can result in significant penalties, including back taxes, interest, and fines.

Local Government Agencies and Oversight

The responsibility for administering and enforcing TOT typically falls to local government agencies, such as city finance departments, county tax collectors, or dedicated revenue departments. These agencies set the tax rates, define the rules and regulations for collection and remittance, issue permits to lodging providers, and conduct audits to ensure compliance. They are also responsible for processing the collected taxes and allocating the funds according to local ordinances.

Taxpayers: The Ultimate Burden

While lodging providers are the collectors, the ultimate burden of the Transient Occupancy Tax falls on the travelers who occupy the lodging. They pay the tax as an additional charge on their accommodation bills. For travelers, it’s important to be aware of TOT as it can add a noticeable amount to the overall cost of a stay, especially in areas with higher tax rates.

Navigating the Complexities of TOT Rates and Regulations

The transient occupancy tax landscape is characterized by its variability. Rates, exemptions, and reporting requirements can differ dramatically, making it essential for both businesses and travelers to stay informed.

Diverse Tax Rates Across Jurisdictions

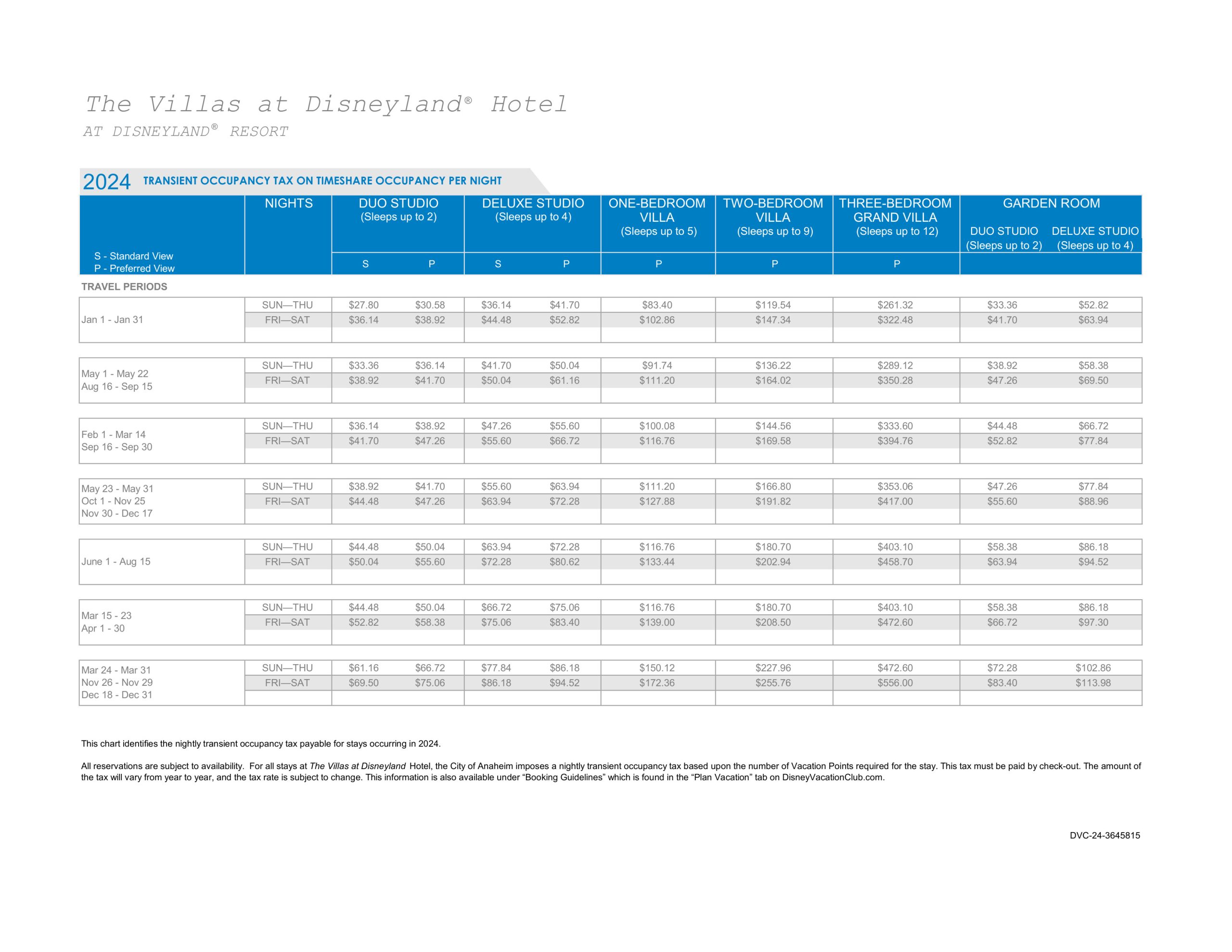

The tax rate for TOT is not uniform. It is determined by the specific local jurisdiction and can range from a few percent to well over 15% in some high-demand tourist destinations. Factors influencing these rates include the local government’s budget needs, the importance of tourism to the local economy, and the desire to fund specific public services. For example, a major city with extensive public transit and cultural amenities might have a higher TOT than a smaller town.

State, County, and City Taxes

It’s also important to recognize that TOT can be levied at multiple levels of government. A single stay might be subject to state, county, and city TOT. For instance, a hotel in a California city might have a state sales tax, a county sales tax, and a city TOT, all of which are collected by the hotel and remitted to the respective government entities. Understanding the combination of these taxes is crucial for accurate calculation and reporting.

Exemptions and Special Cases

While the general rule applies to most short-term stays, there are often specific exemptions and special cases that can affect TOT liability. These are designed to address particular situations or to provide relief to certain types of occupants or establishments.

Government and Non-Profit Exemptions

Many jurisdictions exempt stays by government employees on official business or by individuals representing non-profit organizations. These exemptions are typically granted to alleviate the financial burden on public entities or charitable organizations. Proper documentation, such as a government-issued identification or a non-profit tax-exempt status letter, is usually required to claim these exemptions.

Long-Term Stays and Permanent Residents

As previously mentioned, the distinction between transient and permanent occupancy is critical. Stays exceeding a certain continuous period, usually 30 days, are often exempt from TOT. However, the specific rules for defining “permanent residency” can be complex and may involve written lease agreements and other proof of intent to reside. It’s crucial for lodging providers to have clear policies and procedures for identifying and managing long-term guests to ensure compliance.

Specific Types of Lodging

Some jurisdictions may have different rules for different types of lodging. For instance, campgrounds, RV parks, or specific types of vacation rentals might have their own TOT regulations or be exempt altogether. These variations are often due to the differing service levels and amenities provided by these establishments compared to traditional hotels.

Ensuring Compliance and Best Practices for Lodging Providers

For businesses operating in the hospitality sector, understanding and adhering to TOT regulations is paramount. Non-compliance can lead to severe financial and legal repercussions.

Registration and Permitting Requirements

Before collecting and remitting TOT, lodging providers are generally required to register with the relevant local government agencies and obtain the necessary permits or licenses. This registration process typically involves providing information about the business, its location, and the types of lodging offered. It ensures that the local government is aware of all entities responsible for collecting and remitting the tax.

Maintaining Accurate Records

Meticulous record-keeping is fundamental to TOT compliance. Lodging providers must maintain accurate records of all occupied rooms, the duration of each stay, the room rates charged, the amount of TOT collected, and the amounts remitted to the government. These records are crucial for demonstrating compliance during audits and for resolving any discrepancies that may arise.

Timely Remittance and Reporting

TOT is typically collected on a regular basis, often monthly or quarterly. Lodging providers must ensure that the collected taxes are remitted to the appropriate government agency by the designated deadline. This usually involves filing a TOT return, which details the total revenue generated and the tax amounts collected. Late remittances are often subject to penalties and interest.

Understanding Audit Processes

Local government agencies periodically conduct audits of lodging providers to verify compliance with TOT regulations. These audits may involve reviewing financial records, guest registers, and remittance reports. Lodging providers should be prepared for these audits by maintaining organized and accurate records. Cooperative and transparent engagement with auditors is generally the best approach.

The Impact of TOT on Travelers and the Hospitality Industry

Transient Occupancy Tax has a tangible effect on both the cost of travel and the operational landscape of the hospitality sector.

The Traveler’s Perspective: Added Costs

For travelers, TOT represents an additional cost on top of the room rate, resort fees, and other expenses. While often a small percentage of the total bill, it can add up, particularly for longer stays or in high-tax destinations. Travelers should factor TOT into their budget when planning trips and be aware that the advertised room rate may not be the final price paid.

The Hospitality Industry: Revenue Generation and Operational Challenges

For the hospitality industry, TOT is a double-edged sword. On one hand, it contributes revenue that can be reinvested in community amenities and tourism promotion, ultimately benefiting the industry. On the other hand, the complexities of varying rates, regulations, and reporting requirements can pose significant operational challenges for lodging providers, especially smaller businesses or those operating in multiple jurisdictions. Ensuring accurate calculation, collection, and remittance requires dedicated effort and expertise. The rise of online travel agencies (OTAs) and short-term rental platforms has also introduced new layers of complexity in ensuring TOT compliance across a diverse range of lodging options.

In conclusion, Transient Occupancy Tax is an integral part of the economic and regulatory fabric of communities worldwide. By understanding its definition, purpose, the intricacies of its rates and regulations, and the responsibilities of both lodging providers and travelers, stakeholders can navigate this tax more effectively, contributing to the financial health and continued development of the places we visit.