The world of finance and investment can often seem like a labyrinth of jargon and complex terminology. For individuals looking to understand the basics of the stock market, encountering terms like “par value” can be a point of confusion. While seemingly arcane, understanding stock par value is a foundational element in grasping the legal and historical context of corporate shares, and how they are represented on a company’s balance sheet. This article aims to demystify stock par value, exploring its origins, its modern-day significance, and why it holds a place, however diminished, in contemporary financial reporting.

The Historical Roots of Par Value

The concept of par value traces its origins back to the early days of corporate finance, a period when shares were often printed on physical certificates and represented a tangible claim on a company’s assets. In this era, par value served a more concrete purpose than it does today.

Establishing a Minimum Legal Capital

Historically, par value was intended to establish a minimum legal capital for a corporation. When a company issued stock, the aggregate par value of all issued shares was meant to represent a floor beneath which the company’s stated capital could not fall without formal legal procedures. This was crucial for protecting creditors. In essence, if a company were to liquidate, the par value provided a baseline assurance that there were sufficient assets to cover certain liabilities. This “stated capital” was a key component of a company’s financial structure, representing the capital contributed by shareholders in exchange for ownership.

The “No-Par Value” Movement

As corporate law evolved and the nature of share ownership became more abstract, the relevance of par value began to diminish. Many jurisdictions introduced provisions allowing for the issuance of “no-par value” stock. This meant that shares could be issued without a predetermined nominal value. The primary driver behind this shift was the recognition that par value, especially when set at an arbitrarily low figure, often bore little to no relation to the actual market value or true worth of the shares. This led to the proliferation of low-par value stock, where the stated par value was a fraction of a cent, serving little protective function for creditors.

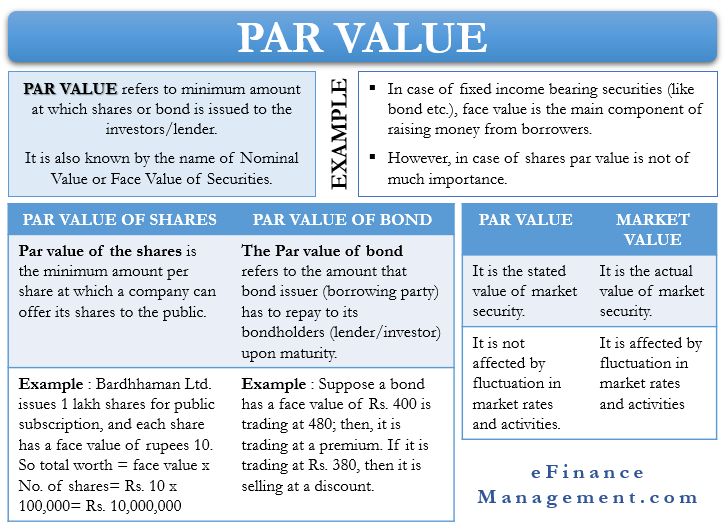

Par Value vs. Market Value

A critical distinction that emerged with the development of stock markets was between par value and market value. Par value is an arbitrary, nominal value assigned to a share by the issuing company. It is a figure set in the company’s charter and has no bearing on the share’s current trading price on an exchange. Market value, on the other hand, is determined by supply and demand in the open market and fluctuates constantly based on a company’s performance, industry trends, economic conditions, and investor sentiment. It is the market value that truly reflects the worth of a share to investors.

Par Value in Modern Corporate Finance

In today’s sophisticated financial landscape, the role of par value has been significantly reduced, yet it persists in several key areas, primarily for accounting and legal compliance rather than for substantive valuation.

Accounting Entries and Balance Sheets

When a company issues stock, the par value plays a role in the accounting entries on its balance sheet. The total amount of capital raised from issuing stock is recorded. A portion of this is allocated to the “Common Stock” or “Preferred Stock” account, valued at the par value per share multiplied by the number of shares issued. Any amount received above the par value is recorded in a separate account, typically called “Additional Paid-In Capital” or “Paid-in Capital in Excess of Par.” For instance, if a company issues 1,000 shares with a par value of $0.01 each for $10 per share, the accounting entry would debit cash for $10,000, credit Common Stock for $10 (1,000 shares * $0.01 par value), and credit Additional Paid-In Capital for $9,990 ($10,000 – $10). This breakdown helps to differentiate between the legally designated capital and the premium paid by investors.

Legal and Regulatory Considerations

Despite its diminished practical significance, par value continues to hold some legal and regulatory weight. Corporate statutes in many jurisdictions still require companies to have a par value for their stock, even if it is nominal. This can influence certain corporate actions, such as stock splits or dividend distributions, though these are now largely governed by market value and board decisions. Furthermore, in the event of bankruptcy or liquidation, the historical par value might still be referenced in legal proceedings, although the primary focus will always be on the actual assets and liabilities of the company.

The Prevalence of Low Par Value Stock

The overwhelming majority of publicly traded companies today issue stock with a very low par value. Common figures include $0.01, $0.001, or even $0.0001 per share. This practice is a vestige of the historical need for a nominal value while acknowledging that this nominal value has no correlation with the share’s true worth. Issuing stock with such a low par value minimizes the amount booked into the “Common Stock” account and maximizes the “Additional Paid-In Capital” account, which is generally seen as a more flexible form of equity capital from an accounting perspective.

Distinguishing Par Value from Related Concepts

To fully understand par value, it is essential to differentiate it from other financial terms that are often associated with stock valuation and corporate capital.

Par Value vs. Stated Value

While similar, “stated value” is a term that sometimes replaces or clarifies the concept of par value, particularly for no-par stock that the board of directors has assigned a “stated value.” The board can declare a stated value for no-par stock, which then functions similarly to par value in accounting. This stated value also contributes to the legal capital of the corporation. However, the key difference is that par value is typically set in the corporate charter, whereas a stated value is determined by a resolution of the board of directors. If no par value or stated value is assigned to shares, then the entire proceeds from the sale of such shares are typically recorded as Additional Paid-In Capital.

Par Value vs. Book Value

Book value, often referred to as the “net asset value” of a company, is a measure of a company’s net worth based on its accounting records. It is calculated by subtracting a company’s total liabilities from its total assets. This figure is then divided by the number of outstanding shares to arrive at the book value per share. Book value represents the theoretical value of a company’s equity if it were to be liquidated at its recorded asset values. It is a historical cost-based valuation and often differs significantly from the market value of a company’s stock, which reflects future earnings potential and market sentiment. Par value, in contrast, is a nominal, assigned value per share with no relation to the company’s assets or liabilities.

Par Value vs. Market Price (Revisited)

As mentioned earlier, the market price is the price at which a stock trades on an exchange. This is the figure that investors use to buy and sell shares and is determined by market forces. Par value, on the other hand, is a fixed, nominal value established at the time of incorporation or stock issuance. It is a legal and accounting construct. For example, a stock might have a par value of $0.01, but its market price could be $50 or $100 or even less than $1, depending on the company’s performance and market conditions. The disparity between par value and market price highlights why par value is no longer a reliable indicator of a stock’s true worth or a company’s financial health.

The Diminishing Significance of Par Value

In the modern era, the practical relevance of par value for the average investor has waned considerably. While it remains a component of corporate accounting and legal frameworks, its influence on investment decisions and company valuations is negligible.

Why Investors Don’t Focus on Par Value

Investors are primarily concerned with a company’s profitability, growth prospects, and competitive position. They analyze financial statements, earnings reports, and market trends to make informed decisions. The par value of a stock is irrelevant to these considerations. A high par value does not indicate a healthy company, nor does a low par value signify financial weakness. Instead, investors look at metrics such as earnings per share (EPS), price-to-earnings (P/E) ratios, revenue growth, and dividend payouts to gauge a stock’s attractiveness.

Par Value and Corporate Actions

While par value has minimal impact on day-to-day trading, it can still play a minor role in specific corporate actions. For instance, stock splits are often described in terms of how they affect the par value per share. A two-for-one stock split, for example, would typically halve the par value per share to maintain the same total par value for the issued stock. Similarly, in some jurisdictions, there might be restrictions on dividend distributions based on the capital represented by par value, although these are largely superseded by statutory provisions regarding distributable earnings.

The Future of Par Value

The trend toward no-par value stock, or stock with nominal par values, is likely to continue. As corporate governance and financial reporting standards become more transparent and sophisticated, the emphasis is shifting towards metrics that provide genuine insight into a company’s performance and value. While par value will likely persist as a legal and accounting formality in many regions, its role as a substantive financial concept has largely been relegated to history. For investors, understanding that par value is a historical artifact and not an indicator of a stock’s true worth is a key takeaway for navigating the complexities of the financial markets.