The concept of “stable value” in the context of financial instruments, particularly within retirement plans, refers to a type of investment designed to preserve capital while offering modest, consistent returns. Unlike traditional market investments that fluctuate with economic conditions, stable value funds aim to provide a predictable outcome for investors. This predictability is achieved through a combination of asset allocation, insurance wrappers, and sophisticated hedging strategies. Understanding stable value is crucial for anyone participating in employer-sponsored retirement plans like 401(k)s or 403(b)s, as it often represents a significant portion of available investment options.

The Fundamentals of Stable Value Funds

Stable value funds are structured to provide a high degree of principal protection and liquidity, making them attractive to investors who are risk-averse or nearing retirement. Their primary objective is to deliver returns that are competitive with short-term fixed-income investments while minimizing volatility. This unique characteristic sets them apart from mutual funds that directly invest in equities or bonds, which are subject to market price fluctuations.

Capital Preservation as a Cornerstone

At the heart of stable value lies a commitment to capital preservation. This means that the fund’s primary goal is to ensure that the initial investment amount remains intact, regardless of market downturns. While this does not guarantee against all possible losses, it significantly reduces the risk of principal erosion that is inherent in many other investment vehicles. This focus on preservation appeals to a broad range of investors, especially those who prioritize security over aggressive growth.

Consistent, Predictable Returns

In addition to capital preservation, stable value funds aim to provide consistent and predictable returns. These returns are typically generated through a diversified portfolio of high-quality fixed-income securities, such as government bonds, corporate bonds, and mortgage-backed securities. The weighted average maturity of these underlying assets is carefully managed to align with the fund’s objectives. While the returns are generally lower than those of equity investments, they offer a more stable and reliable stream of income over time, which can be particularly beneficial for long-term financial planning.

Liquidity and Accessibility

A key feature of stable value funds, especially within retirement plans, is their liquidity. Participants can typically withdraw their invested principal and accumulated interest without penalty or significant delay. This accessibility is vital for individuals who may need to access their funds for unexpected expenses or to rebalance their portfolios. The underlying structure of stable value funds, which often includes wrap contracts with insurance companies, plays a critical role in ensuring this liquidity, even during periods of market stress.

The Mechanics Behind Stable Value

The stability and predictability of stable value funds are not accidental; they are the result of a carefully orchestrated combination of investment strategies, risk management techniques, and contractual agreements. Understanding these underlying mechanics is essential to appreciating how these funds achieve their unique characteristics.

Diversified Investment Portfolio

The core of a stable value fund is its investment portfolio, which is predominantly composed of high-quality fixed-income instruments. These can include:

- Government Securities: U.S. Treasury bills, notes, and bonds, known for their low credit risk.

- Corporate Bonds: Investment-grade corporate debt issued by financially sound companies.

- Mortgage-Backed Securities (MBS): Securities backed by pools of mortgages, carefully selected for their credit quality and duration.

- Asset-Backed Securities (ABS): Securities backed by other forms of receivables, such as auto loans or credit card receivables.

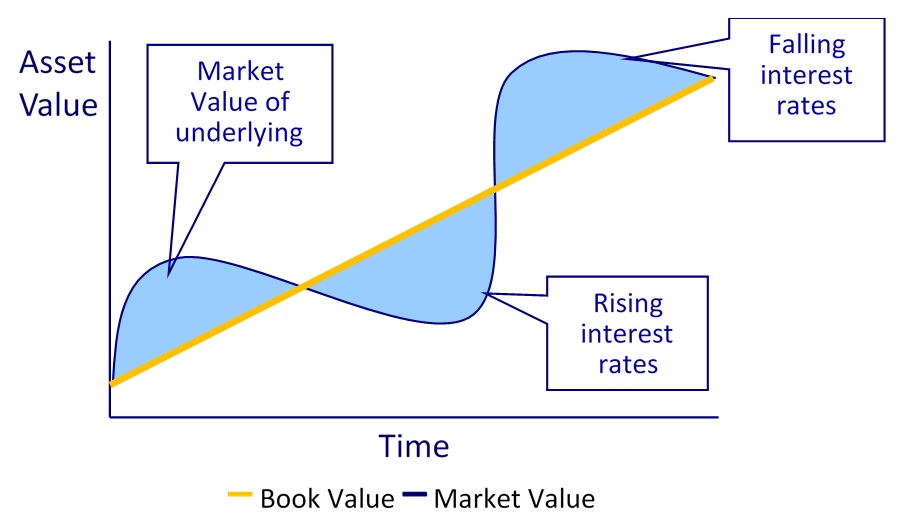

The selection and management of these assets are crucial. Fund managers focus on instruments with strong credit ratings and manage the portfolio’s duration (a measure of interest rate sensitivity) to mitigate the impact of rising interest rates. A shorter duration generally leads to less price volatility.

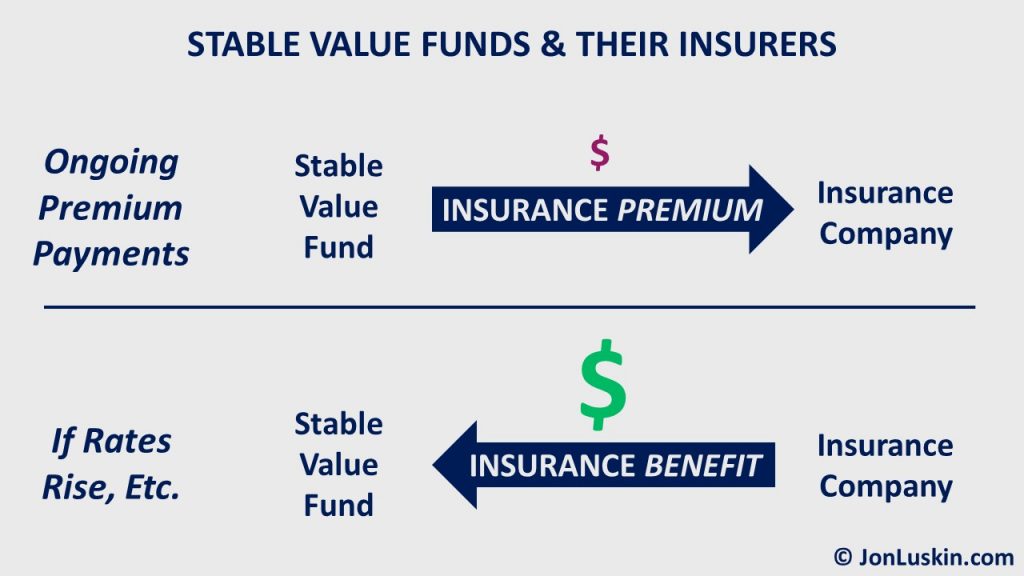

The Role of Insurance Wraps

A defining feature of most stable value funds is the presence of “wrap contracts” or “guarantees” provided by insurance companies. These contracts are essential to the fund’s ability to provide guaranteed principal and stable crediting rates.

- How Wraps Work: The insurance company, in exchange for a fee, agrees to guarantee the principal and provide a stable crediting rate for the fund’s assets. This means that even if the underlying portfolio experiences some market depreciation, the insurance company is obligated to make up the difference, ensuring that the participant’s investment value remains protected.

- Types of Wraps: Common types of wrap contracts include Synthetic Guaranteed Investment Contracts (GICs) and traditional GICs. Synthetic GICs often involve a combination of insurance and derivative strategies to achieve the guarantee.

- Insurance Company Strength: The financial health and creditworthiness of the insuring insurance company are paramount. Investors are implicitly relying on the insurer’s ability to meet its obligations. Therefore, the selection of financially strong and reputable insurance providers is a critical aspect of stable value fund management.

Contractual Arrangements and Rebalancing

Stable value funds operate under specific contractual arrangements that define how the fund’s assets are managed and how returns are credited.

- Crediting Rate: The “crediting rate” is the rate of return that stable value participants actually earn. This rate is typically reset periodically (e.g., monthly or quarterly) and reflects the performance of the underlying assets, adjusted for expenses and the cost of the wrap contract. The crediting rate is designed to be relatively stable, smoothing out market fluctuations.

- Rebalancing and Duration Management: Fund managers actively manage the portfolio’s duration to maintain alignment with the fund’s objectives and the terms of the wrap contracts. This involves rebalancing the portfolio by buying or selling securities to adjust the average maturity and interest rate sensitivity. This active management helps to ensure that the fund can meet its obligations and maintain its stable value characteristic.

Stable Value in Retirement Planning

The primary application of stable value funds is within employer-sponsored retirement savings plans, such as 401(k)s, 403(b)s, and governmental 457(b)s. They serve as a valuable component of a diversified retirement portfolio, particularly for individuals who are approaching retirement or who have a low-risk tolerance.

A Safe Harbor for Retirement Savings

For participants in retirement plans, stable value funds often function as a “safe harbor” for a portion of their savings. This is especially true for those who are:

- Nearing Retirement: As individuals get closer to retirement, their priority often shifts from aggressive growth to capital preservation. Stable value offers a way to protect accumulated savings while still earning a modest return.

- Risk-Averse: Some investors are inherently risk-averse and prefer to avoid the volatility associated with stock and traditional bond funds. Stable value provides a more predictable investment experience.

- Seeking Diversification: Within a broader retirement portfolio, stable value can act as a diversifier, providing a counterbalance to more volatile assets like equities.

Comparison to Other Investment Options

Understanding how stable value funds compare to other common retirement plan investments is key to making informed decisions.

- Money Market Funds: While both offer stability, money market funds invest in very short-term debt instruments and typically yield less than stable value funds. Stable value funds, with their longer durations and wrap contracts, generally aim for higher, albeit still modest, returns.

- Bond Funds (e.g., Intermediate-Term Bond Funds): Traditional bond funds are subject to market interest rate risk. If interest rates rise, the value of existing bonds falls. Stable value funds, through their hedging and wrap contracts, aim to mitigate this risk and maintain a stable unit value.

- Equity Funds: Equity funds, which invest in stocks, offer the potential for higher returns but come with significantly higher risk and volatility. Stable value funds are not designed for aggressive growth and are therefore much less volatile.

Considerations for Participants

While stable value funds offer many advantages, participants should be aware of a few considerations:

- Limited Growth Potential: The emphasis on capital preservation means that stable value funds typically offer lower potential returns compared to equity investments. They are not designed for aggressive capital appreciation.

- Interest Rate Sensitivity: Although managed to be stable, the crediting rate of a stable value fund can be influenced by broader interest rate movements over the longer term. When interest rates rise significantly, the crediting rate may adjust upwards, but this adjustment is often smoother and less immediate than in traditional bond funds.

- Underlying Insurance Company Risk: As mentioned, the stability of the fund is dependent on the financial strength of the insurance company providing the wrap contract. While rare, the failure of an insurer could theoretically impact the fund. However, reputable fund providers meticulously vet their insurance partners to minimize this risk.

- Exit Strategies: In some cases, especially for larger institutional investors, there might be restrictions or surrender charges associated with withdrawing significant amounts of capital from stable value funds quickly. However, for typical retirement plan participants, liquidity is generally not an issue for routine withdrawals.

By understanding these nuances, individuals can effectively integrate stable value funds into their retirement savings strategies, leveraging their unique benefits for a more secure financial future.