Secured transactions form the bedrock of commercial lending and credit, providing a crucial mechanism for lenders to mitigate risk when extending financing. At its core, a secured transaction involves a debtor granting a creditor a security interest in specific personal property. This security interest serves as collateral, giving the creditor a right to seize and sell the collateral if the debtor defaults on their obligations. Understanding the nuances of secured transactions is vital for businesses, financial institutions, and legal professionals alike, as it impacts everything from small business loans to large-scale asset financing.

The Uniform Commercial Code (UCC), particularly Article 9, governs secured transactions in the United States. It provides a comprehensive framework for creating, perfecting, and enforcing security interests, ensuring predictability and fairness for all parties involved. This article will delve into the fundamental concepts of secured transactions, exploring the elements that constitute a security interest, the methods for perfecting that interest, and the procedures for enforcing it in the event of a default. By demystifying these processes, we can better appreciate the role secured transactions play in facilitating commerce and economic growth.

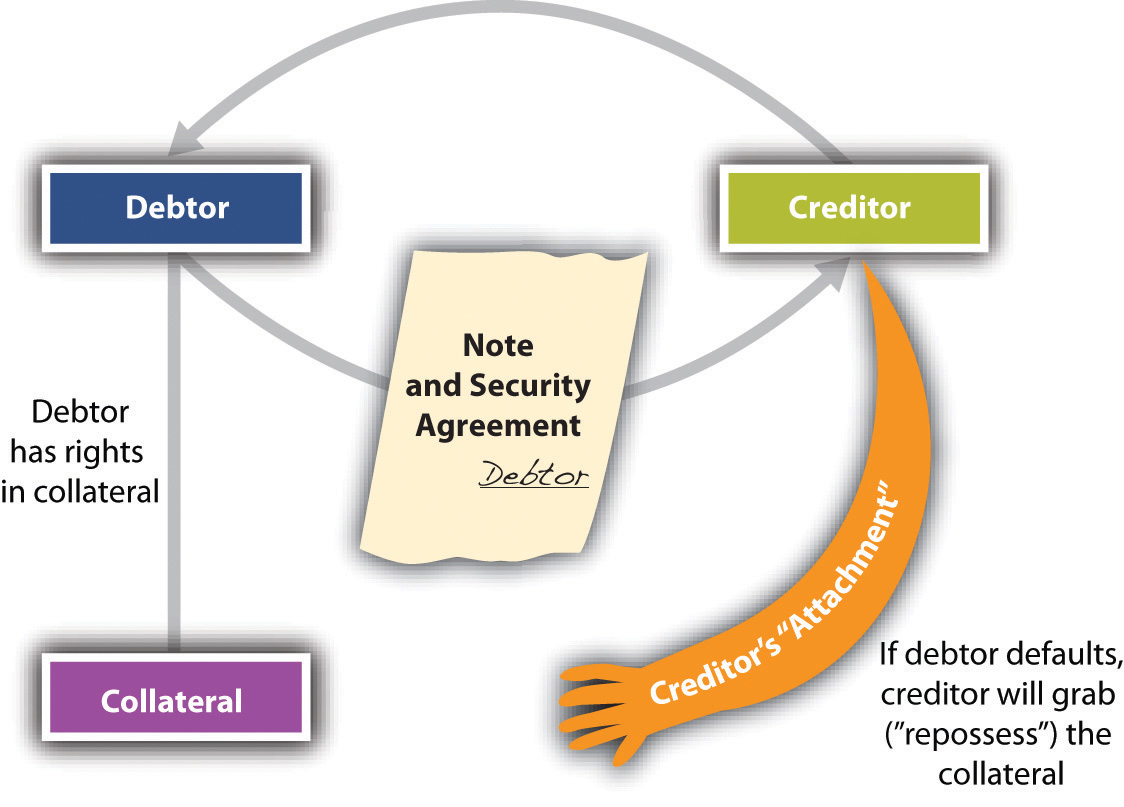

The Genesis of a Security Interest: Creation and Attachment

The creation of a security interest is the initial step in establishing a secured transaction. This process involves an agreement between the debtor and the creditor, which is then followed by “attachment.” Attachment signifies that the creditor’s security interest has become legally enforceable against the debtor. For attachment to occur, three essential conditions must be met:

Debtor’s Rights in the Collateral

The debtor must possess rights in the collateral being pledged. This can take several forms. The debtor might own the collateral outright, meaning they have full legal title and possession. Alternatively, the debtor might have a leasehold interest, a right to use the collateral for a specific period, or even a right to acquire the collateral. The critical point is that the debtor must have a possessory or proprietary interest that can be subjected to a security interest. For instance, a debtor cannot grant a security interest in property they do not own or possess, such as a car that is fully owned by their spouse and not in their possession. The extent of the debtor’s rights in the collateral will dictate the scope of the security interest the creditor can obtain.

Value Given by the Creditor

The creditor must give value to the debtor. “Value” is broadly defined under the UCC and encompasses more than just the direct disbursement of cash. It includes:

- An Executory Promise: This refers to a promise to extend credit or perform some future obligation. For example, a bank might agree to lend a business a certain amount of money over the next year. The promise of future funds constitutes value.

- The Creation or Enforcement of a Security Interest: Sometimes, a creditor might be providing new value in exchange for a security interest in collateral that already exists.

- The Satisfaction or Securing of a Pre-existing Claim: This is known as “past consideration.” If a debtor owes a creditor a pre-existing debt, and the creditor agrees to take a security interest in collateral to secure that debt, the pre-existing debt itself serves as value.

This requirement ensures that the debtor receives something tangible or a binding commitment in exchange for encumbering their property. It prevents a creditor from claiming a security interest in property without having provided any benefit to the debtor.

The Security Agreement

A security agreement is the cornerstone of any secured transaction. It is a contract between the debtor and the creditor that clearly describes the collateral and grants the creditor a security interest in it. For a security agreement to be enforceable, it generally must:

- Be Authenticated by the Debtor: This means the debtor must sign the agreement or otherwise indicate their assent in a manner that is recorded or transmitted. Electronic signatures are typically accepted.

- Describe the Collateral with Reasonable Particularity: The description of the collateral must be sufficient to identify it. Overly broad or vague descriptions may render the agreement unenforceable. For example, simply stating “all personal property” might not be sufficient. Specificity is key.

While a written security agreement is the most common and recommended method, a security interest can also be created without a written agreement if the creditor takes possession of the collateral. This is known as a possessory security interest, which is discussed further in the perfection section.

Establishing Priority: Perfection of Security Interests

Attachment makes a security interest enforceable against the debtor, but perfection is what makes it enforceable against third parties. Perfection is the process by which a creditor gives public notice of their security interest in collateral. This notice is crucial because it establishes the creditor’s priority position relative to other potential creditors or purchasers of the collateral. The UCC outlines several methods of perfection, with the most common being the filing of a financing statement.

Filing a Financing Statement

The most prevalent method of perfection is filing a UCC-1 financing statement with the appropriate state filing office. This statement provides public notice that a creditor has a security interest in certain collateral. A financing statement generally includes:

- The Names of the Debtor and Secured Party: Accurate identification is paramount.

- An Indication of the Collateral: This description can be less specific than that required in a security agreement, as long as it sufficiently identifies the collateral. It can refer to categories of goods or specific items.

The UCC-1 is typically filed in the state where the debtor is located. For most businesses, this is the state where they are incorporated or have their chief executive office. For individuals, it’s generally their principal residence. Once filed, the financing statement remains effective for a period of five years and can be renewed. The date of filing is critical, as it generally determines the secured party’s priority.

Possession of the Collateral

In certain circumstances, a creditor can perfect a security interest simply by taking physical possession of the collateral. This method is commonly used for tangible assets like jewelry, precious metals, or negotiable instruments. When a creditor has possession, it serves as a strong form of public notice, as anyone dealing with the debtor would be aware that the property is not solely under the debtor’s control.

Possession is the exclusive method of perfection for certain types of collateral, such as:

![]()

- Money: Cash is perfected by possession.

- Certificated Securities: Physical certificates representing ownership of securities.

- Negotiable Documents: Documents that represent title to goods, like bills of lading.

For other types of collateral, like goods or instruments, possession can be an alternative to filing.

Control of the Collateral

For certain intangible assets, such as deposit accounts, investment property, and electronic chattel paper, perfection is achieved through “control.” Control is a more stringent standard than possession and typically requires the secured party to have the ability to use or dispose of the collateral without the debtor’s further assent.

For a deposit account, control is achieved when the secured party is the bank with which the account is maintained, or when the debtor has agreed in writing that the bank will follow the secured party’s instructions concerning the account. For investment property, control is established through various means depending on the nature of the property, such as holding the securities directly, or having arrangements with intermediaries that ensure the secured party’s ability to direct sales or encumbrances.

Automatic Perfection

In a limited number of situations, a security interest is perfected automatically upon attachment, without any further action required by the creditor. The most significant example is a Purchase Money Security Interest (PMSI) in consumer goods. A PMSI arises when a seller or lender finances the purchase of goods for a debtor, and the goods themselves serve as collateral for the loan. If the collateral is consumer goods (goods primarily for personal, family, or household use), the security interest is automatically perfected upon attachment. This means that if a consumer buys a television on credit from a retailer, and the retailer retains a security interest in the television, that interest is perfected as soon as the consumer takes possession and the security agreement is in place.

The Enforcement of Secured Transactions: Remedies Upon Default

When a debtor fails to fulfill their obligations under a secured loan agreement, the creditor has the right to enforce their security interest. The UCC provides a structured process for creditors to repossess and dispose of collateral to satisfy the outstanding debt. This process is designed to be commercially reasonable, protecting both the creditor’s interests and, to some extent, the debtor’s residual rights.

Repossession of Collateral

Upon default, the secured party has the right to repossess the collateral. This can be done through self-help, meaning the creditor can take possession of the collateral without judicial intervention, provided it can be done without breaching the peace. A breach of the peace occurs if the repossession involves violence, threats, breaking and entering into a debtor’s dwelling, or other unlawful acts. If self-help repossession is not feasible or would likely result in a breach of the peace, the secured party must resort to a judicial action, such as replevin, to obtain possession of the collateral.

Notice of Disposition

After repossessing the collateral, the secured party must generally provide the debtor with reasonable notice of the intended disposition of the collateral. This notice requirement is crucial for ensuring that the debtor has an opportunity to protect their interests, such as by finding a buyer for the collateral or arranging to redeem it. The notice typically must:

- Describe the Debtor and Secured Party: Clearly identify the parties involved.

- Describe the Collateral: Provide a clear description of the property being sold.

- State the Method of Disposition: Indicate whether the sale will be public or private.

- Specify the Time and Place of Public Disposition (if applicable): For public sales, the exact details must be provided.

- Detail the Terms of any Private Disposition (if applicable): For private sales, information about how the sale will be conducted is required.

There are exceptions to the notice requirement, such as when the collateral is perishable, threatens to decline speedily in value, or is of a type customarily sold on a recognized market.

Commercial Reasonableness of Disposition

The UCC mandates that every aspect of the disposition of collateral, including the method, manner, time, place, and other terms, must be commercially reasonable. This means that the sale must be conducted in a way that a prudent person would conduct a sale of similar property. The goal is to obtain the highest possible price for the collateral.

- Public Disposition: This involves selling the collateral at an auction or similar event open to the public.

- Private Disposition: This typically involves negotiating a sale with a third party.

If the disposition is not commercially reasonable, the secured party may be liable to the debtor for any damages caused by the unreasonable disposition.

![]()

Application of Proceeds and Deficiency Judgments

The proceeds from the disposition of collateral are applied in a specific order:

- Expenses of Repossession and Sale: Costs incurred in repossessing and preparing the collateral for sale.

- Satisfaction of the Secured Obligation: The outstanding debt owed to the secured party.

- Satisfaction of Subordinate Security Interests: If there are other creditors with perfected security interests in the same collateral, their claims are paid from any remaining proceeds, in order of their priority.

If the proceeds from the sale are insufficient to satisfy the entire debt, the secured party may be entitled to pursue a deficiency judgment against the debtor for the remaining balance. Conversely, if there are excess proceeds after satisfying all secured obligations and junior liens, the surplus must be returned to the debtor.

In conclusion, secured transactions are a vital legal and financial mechanism that underpins much of modern commerce. By understanding the creation, perfection, and enforcement of security interests, individuals and businesses can navigate the complexities of lending and borrowing with greater confidence and security. The UCC provides a robust framework, but careful attention to detail and adherence to its provisions are paramount for all parties involved.