In the dynamic and rapidly evolving landscape of Canadian technology and innovation, particularly within sectors like drones and Unmanned Aerial Vehicles (UAVs), understanding the intricacies of the Canadian tax system is not merely a compliance burden but a strategic imperative. The Goods and Services Tax (GST), and its harmonized counterpart, the Harmonized Sales Tax (HST), play a significant role in the financial operations of every tech startup, established innovator, and service provider across the nation. Far from being a dry administrative detail, mastering the nuances of GST/HST can impact cash flow, pricing strategies, and ultimately, the profitability and sustainability of a tech venture. This comprehensive guide aims to demystify GST Canada tax, offering an insightful perspective tailored for those operating at the forefront of innovation, from drone design and manufacturing to advanced aerial data solutions and autonomous flight systems.

Canada’s commitment to fostering a vibrant tech ecosystem means that innovators must navigate not just technical challenges but also the regulatory and financial frameworks that govern commerce. For drone companies, this includes everything from sourcing components globally to selling sophisticated aerial imaging services domestically or internationally. Understanding how and when to collect, remit, and reclaim GST/HST is fundamental to successful financial management and ensures that groundbreaking technological advancements are not hampered by avoidable tax missteps.

This article will delve into the core principles of GST/HST, explore its specific implications for the drone and broader tech innovation sector, guide businesses through compliance best practices, and offer strategic insights for tax planning that supports growth and resilience. By approaching GST Canada tax from the perspective of innovation, we aim to provide a practical and engaging resource for the pioneers building the future of flight technology and beyond.

The GST/HST Framework in Canada: A Primer for Tech Innovators

At its core, the Goods and Services Tax (GST) is a federal value-added tax levied on most goods and services sold in Canada. In several provinces, the GST has been harmonized with provincial sales taxes to form the Harmonized Sales Tax (HST). Understanding this fundamental distinction is the first step for any tech entrepreneur or innovator navigating the Canadian market.

Understanding the Basics: Goods and Services Tax (GST) and Harmonized Sales Tax (HST)

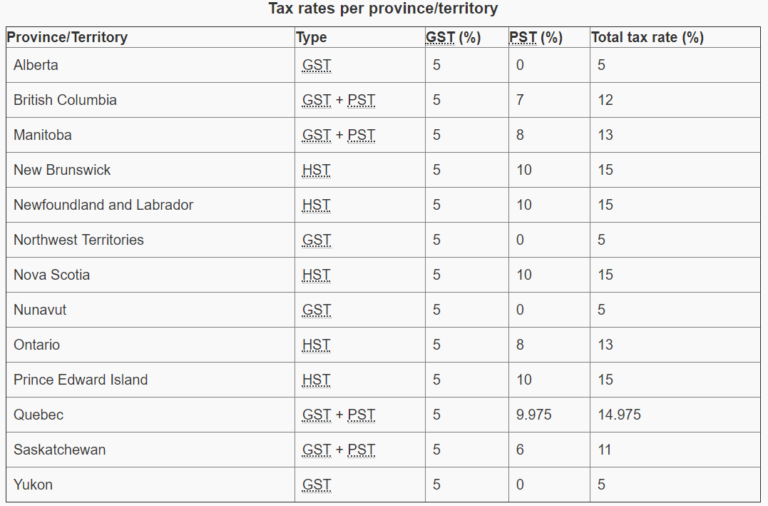

The GST is a 5% tax applied across all provinces and territories. In provinces that have harmonized their provincial sales tax with the GST, the HST is applied as a single, combined tax rate. For instance, in Ontario, the HST rate is 13%, comprising the 5% federal portion and an 8% provincial portion. Other HST provinces include New Brunswick, Newfoundland and Labrador, Nova Scotia, and Prince Edward Island, each with their own combined rate. In provinces without HST (British Columbia, Alberta, Saskatchewan, Manitoba, Quebec), only the 5% GST applies, and a separate provincial sales tax (PST) might be collected independently. This provincial variation is crucial for tech companies, particularly those offering services or selling products across provincial lines, as it dictates the tax rate they must charge their customers. For a drone manufacturing company, for example, selling a UAV to a client in Alberta (GST only) versus a client in Nova Scotia (HST) requires different invoicing and collection practices.

Who Needs to Register? Small Suppliers and the Threshold for Tech Startups

Not every business in Canada is required to register for a GST/HST account. The Canada Revenue Agency (CRA) defines a “small supplier” as a person or entity whose total taxable revenues (before expenses) from worldwide taxable supplies are $30,000 or less in a single calendar quarter or over four consecutive calendar quarters. For public service bodies (which could include some research and development non-profits in the tech sector), the threshold is $50,000.

For a new tech startup developing innovative drone navigation systems or offering specialized aerial photography services, determining if they meet this threshold is critical. If a business’s revenue falls below this amount, they are not required to register for GST/HST, nor do they charge or collect it. However, they also cannot claim Input Tax Credits (ITCs) for the GST/HST they paid on their business expenses. Many tech startups, even those initially below the threshold, choose to voluntarily register. This allows them to reclaim ITCs, which can be a significant benefit when investing heavily in equipment, R&D, and operational overhead—costs that are prevalent in the capital-intensive drone and flight technology sectors. Voluntary registration can also project a more established and professional image to clients and investors.

GST/HST Implications for the Drone and UAV Sector

The burgeoning drone and UAV sector, characterized by rapid technological advancements and diverse applications, presents unique considerations for GST/HST. From the sale of sophisticated hardware to the provision of data analytics powered by aerial intelligence, every transaction is subject to specific tax rules.

Taxation of Drone Sales and Services

The sale of drones, components, and related software in Canada is generally subject to GST/HST at the applicable rate for the province of sale. This applies whether a company is selling a micro-drone for hobbyists, a high-end commercial UAV for precision agriculture, or an advanced FPV system for racing. Similarly, services provided by drone operators—such as aerial mapping, surveying, inspection, cinematography, or security surveillance—are also typically subject to GST/HST.

However, certain exceptions and nuances exist. For instance, services provided to non-residents that are performed entirely outside Canada may be zero-rated (taxed at 0%), as might certain international transportation services related to the export of drone technology. Understanding the “place of supply” rules is paramount, especially for tech firms engaging in cross-border e-commerce or providing remote services, as this determines which provincial tax rate applies. For a company offering AI-powered flight path optimization services, the location of the client, the location where the service is consumed, and the contractual terms will all influence the GST/HST treatment.

Importing Drone Technology and Parts

Canada’s drone industry relies heavily on imported technology, including specialized sensors, high-performance batteries, advanced propulsion systems, and sophisticated navigation components. When a Canadian tech company imports these items, they are generally required to pay GST (or the federal portion of HST) on the value of the goods at the time of importation. This GST paid on imports can typically be recovered as an Input Tax Credit (ITC) by GST/HST registrants, provided the goods are for commercial activity.

Furthermore, tariffs and duties may also apply to imported drone parts, adding to the overall cost. Tech innovators must factor these costs into their financial models and understand international trade agreements that might reduce or eliminate certain duties. Accurate classification of imported goods using the Harmonized System (HS) codes is crucial to ensure correct tax and duty assessment, preventing delays and unexpected costs that could impact project timelines for new drone development.

R&D and Innovation Credits: How GST/HST Applies

Canada actively supports research and development through various programs, most notably the Scientific Research and Experimental Development (SR&ED) program. While SR&ED offers tax credits on eligible expenditures, it’s important to understand how GST/HST fits into this. The GST/HST paid on expenses related to SR&ED activities (e.g., equipment purchases, salaries of R&D personnel, prototyping materials, software licenses) can generally be claimed as ITCs by GST/HST registrants. This effectively reduces the cost of innovation for companies engaged in developing cutting-edge drone technologies, whether it’s autonomous flight algorithms or new sensor integration methods.

However, the SR&ED tax credit itself is not subject to GST/HST. The interplay between these different tax mechanisms can be complex, and tech companies often benefit from professional advice to maximize their benefits and ensure compliance, thereby accelerating their innovation cycles without unnecessary financial burdens.

Navigating Compliance for Drone Businesses

Effective GST/HST compliance is more than just collecting and remitting tax; it’s about maintaining meticulous records, understanding reporting obligations, and strategically managing cash flow. For rapidly scaling drone businesses, robust compliance safeguards against penalties and frees up resources to focus on core innovation.

Invoicing and Collection Best Practices

For every taxable supply of a drone or service, a GST/HST registrant must issue an invoice that clearly indicates the amount of GST/HST charged, or states that the amount includes GST/HST and gives the applicable rate. Invoices should include the seller’s business name, GST/HST registration number, the date of the invoice, a description of the goods or services, and the customer’s name and address. For drone services, especially those with complex pricing structures or phased projects, clear itemization is crucial. Accurate invoicing not only ensures compliance but also facilitates the customer’s ability to claim their own ITCs if they are also a registrant. Tech companies should also have clear policies for handling returns, refunds, or service adjustments, ensuring that GST/HST is correctly adjusted in these scenarios.

Filing GST/HST Returns: Frequency and Methods

The frequency with which a business must file GST/HST returns depends on its annual taxable revenues. Businesses with annual taxable supplies of $1.5 million or less generally file annually. Those with taxable supplies between $1.5 million and $6 million file quarterly, and businesses with over $6 million in taxable supplies file monthly. Many growing drone companies will transition through these thresholds, necessitating adjustments to their filing routines.

Returns can be filed electronically through the CRA’s My Business Account portal or via GST/HST NETFILE. Electronic filing is generally recommended for its efficiency and accuracy. Even if no GST/HST was collected or paid in a reporting period, a “nil” return must still be filed. Timely filing and remittance are critical to avoid penalties and interest charges, which can quickly erode the thin margins often characteristic of early-stage tech ventures.

Common Pitfalls for Tech Entrepreneurs

One of the most common pitfalls for tech entrepreneurs, especially those in the early stages, is failing to register for GST/HST when their taxable revenues exceed the small supplier threshold. This can result in retroactive tax assessments, penalties, and interest. Another frequent issue is misclassifying supplies as exempt or zero-rated when they are in fact taxable, or conversely, charging GST/HST on exempt supplies. Incorrectly determining the “place of supply” can also lead to charging the wrong provincial tax rate.

For drone companies specifically, distinguishing between hardware sales, software licensing, and service delivery can sometimes blur tax lines. Miscalculating ITCs, either by claiming ITCs on non-eligible expenses or by failing to claim all eligible ITCs, also represents a significant compliance challenge and a missed financial opportunity. Robust accounting systems and, crucially, access to expert tax advice, are indispensable for mitigating these risks within the dynamic tech environment.

Strategic Tax Planning for Growth in Tech & Innovation

Beyond mere compliance, proactive tax planning for GST/HST can be a powerful tool for accelerating growth and optimizing financial performance within the tech and innovation sector. Strategic management of ITCs and an understanding of cross-provincial variations are key.

Input Tax Credits (ITCs) for Operational Expenses

Input Tax Credits (ITCs) are fundamental to the GST/HST system and are particularly beneficial for capital-intensive tech companies. An ITC allows a GST/HST registrant to recover the GST/HST paid on purchases and expenses incurred for their commercial activities. This means the GST/HST paid on drone components, R&D equipment, office rent, utilities, marketing services, legal fees, and even employee travel expenses can be reclaimed, effectively reducing the net cost of these inputs.

For drone manufacturers and service providers, maximizing ITC claims is crucial for cash flow management. This requires meticulous record-keeping of all business expenses and corresponding GST/HST amounts. Companies should have clear processes for tracking all eligible inputs, ensuring no reclaimable tax is overlooked. For instance, the GST/HST paid on a new 3D printer for prototyping drone parts or on cloud computing services for data analysis are all eligible ITCs, making innovation more cost-effective.

Cross-Provincial Sales and HST Variations

As Canada’s tech companies expand their reach, cross-provincial sales become a common occurrence. The differing provincial GST/HST rates (or GST + PST in non-HST provinces) necessitate careful attention to the “place of supply” rules. These rules determine which provincial tax rate applies based on factors such as where the goods are delivered, where services are performed, or the location of the recipient.

For a drone software company selling licenses to clients across Canada, understanding these rules is vital to avoid charging too much or too little tax. Inaccurate application of provincial rates can lead to either customer dissatisfaction (due to overcharging) or CRA assessments (due to undercharging). Implementing robust sales tax software or consulting with tax professionals familiar with the nuances of provincial taxation is highly recommended for tech businesses with a national footprint.

Future Considerations for Emerging Drone Technologies

The drone industry is not static; it’s constantly evolving with breakthroughs in AI, autonomous flight, remote sensing, and urban air mobility. This rapid pace of innovation can create new tax complexities. For example, how will “drone-as-a-service” models, where access to a drone fleet is licensed rather than sold, be taxed? What about blockchain-secured drone data or entirely new forms of aerial transportation?

As new business models and technologies emerge, tax authorities will adapt, and new guidelines may be issued. Tech innovators in the drone space must remain vigilant, staying abreast of changes in tax legislation and proactively engaging with tax advisors. Strategic planning today, grounded in a solid understanding of GST/HST, will ensure that Canadian tech companies can continue to innovate, grow, and compete effectively on the global stage, free from unforeseen tax liabilities or compliance burdens. The GST Canada tax, therefore, is not just a regulatory obligation but an integral component of the financial strategy for any successful tech and innovation enterprise.