The ability to earn income while working abroad presents a unique set of financial considerations, particularly when it comes to taxation. For many expatriates, a significant tax benefit is the Foreign Earned Income Exclusion (FEIE). This provision allows eligible U.S. citizens and resident aliens to exclude a portion of their foreign earnings from U.S. income tax. Understanding the intricacies of FEIE is crucial for anyone living and working outside the United States to ensure proper tax compliance and maximize their financial well-being.

Understanding the Fundamentals of Foreign Earned Income Exclusion

The Foreign Earned Income Exclusion is a powerful tool designed by the U.S. government to prevent double taxation on income earned by its citizens and residents working in foreign countries. It acknowledges the financial burdens and expenses often associated with living abroad, such as higher costs of living in certain regions or the necessity of maintaining a household in the U.S. while working overseas.

Eligibility Criteria for FEIE

To qualify for the Foreign Earned Income Exclusion, individuals must meet two primary requirements: they must have foreign earned income, and they must meet a bona fide residence test or a physical presence test.

Bona Fide Residence Test

This test determines if you have established a genuine home in a foreign country. It’s not merely about spending time abroad but about demonstrating an intent to reside there permanently or indefinitely. Several factors are considered by the IRS when evaluating bona fide residence, including:

- Your actions and intentions: Do you intend to make the foreign country your permanent home? Have you established a home there, or are you merely visiting temporarily?

- Location of your family: If you are married, where does your spouse and children reside? If they live with you in the foreign country, it strengthens your claim of bona fide residence.

- Your housing arrangements: Do you own or rent a home or apartment in the foreign country? Is it furnished and maintained for your regular use?

- Your business or professional ties: Do you have employment or business interests in the foreign country?

- Your social and cultural ties: Are you a member of local clubs or organizations? Do you participate in local community activities?

- Your visa status: The type of visa you hold in the foreign country can be indicative of your residency status.

- Your intent to return to the U.S.: While you can be a bona fide resident of a foreign country, you must not have a present intent to abandon your U.S. domicile. However, the IRS recognizes that individuals may have a desire to return to the U.S. at some point.

The bona fide residence test is generally more complex and subjective than the physical presence test. It requires a thorough examination of an individual’s personal and professional circumstances.

Physical Presence Test

Alternatively, you can qualify for FEIE if you meet the physical presence test. This test requires you to be physically present in a foreign country (or countries) for at least 330 full days during any consecutive 12-month period. This 12-month period does not need to coincide with the tax year. You can choose the 12-month period that yields the most favorable results for your tax situation.

- Counting the days: A “full day” is generally considered a period of 24 hours. You are considered present in a foreign country on a given day if you are physically present there at any time during that day. However, time spent in transit between two foreign countries is generally counted as time spent in a foreign country.

- Consecutive 12-month period: The crucial element is that the 330 days must be consecutive. For example, if you start working in a foreign country on January 1, 2023, you would need to be physically present for 330 days by December 31, 2023, or any other 12-month period thereafter.

- Travel days: Travel days between the U.S. and a foreign country, or between foreign countries, can be tricky. Generally, time spent on a “bona fide trip” to the U.S. does not count towards the 330 days. However, if your travel is incidental to your foreign employment, it might be counted differently. It’s essential to keep detailed records of your travel to accurately determine your qualifying days.

It’s important to note that the physical presence test is more objective and easier to document than the bona fide residence test, as it relies solely on your physical location.

Defining Foreign Earned Income

Foreign earned income is income you receive for services performed while you are a U.S. citizen or resident alien and are a bona fide resident of a foreign country or meet the physical presence test. This typically includes wages, salaries, bonuses, tips, and other compensation for personal services.

However, there are certain types of income that are not considered foreign earned income for the purposes of FEIE:

- Income earned while you are not a bona fide resident or do not meet the physical presence test: If you are in a foreign country for a short business trip and earn income, it will likely be subject to U.S. taxation as usual.

- “Unreimbursed expenses” of employees: While employees can exclude certain unreimbursed business expenses, these are not directly part of the foreign earned income exclusion itself.

- “Paid by the employer on your behalf”: Amounts paid by your employer for your benefit, such as health insurance premiums, may not be considered directly earned by you.

- Income earned in U.S. possessions: Earnings from Puerto Rico, Guam, the U.S. Virgin Islands, or American Samoa are generally not considered foreign earned income.

- “Moving expenses”: Certain employer-provided moving expenses may be taxable.

- Certain allowances: Some allowances, like per diem payments for meals or lodging, may be treated differently depending on their nature and purpose.

- Income earned from services performed in international waters or outer space: These are generally not considered earned in a foreign country.

- Income earned from sources within the U.S.: Even if you are abroad, if the services for which you are paid are performed in the U.S., that income is not foreign earned.

Understanding what constitutes foreign earned income is critical to correctly calculating your exclusion amount.

Calculating and Claiming Your Foreign Earned Income Exclusion

The exclusion amount is not arbitrary; it’s tied to a specific limit set annually by the IRS, adjusted for inflation. Knowing how to calculate this limit and properly file the necessary forms is essential for benefiting from FEIE.

The Annual Exclusion Limit

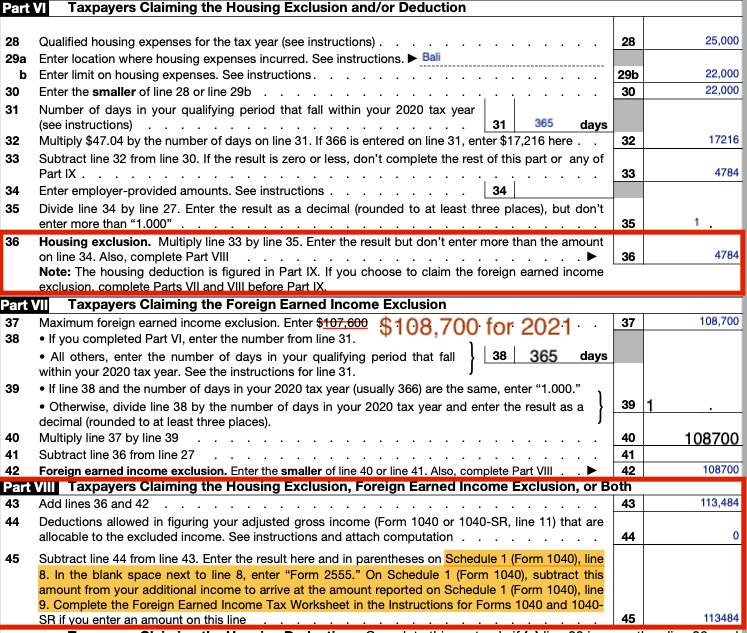

The maximum amount of foreign earned income you can exclude is adjusted annually for inflation. For example, for the tax year 2023, the maximum exclusion amount was $120,000. This means that if you earned $150,000 in foreign income and met the eligibility requirements, you could exclude up to $120,000 of that income from your U.S. taxable income. The remaining $30,000 would then be subject to U.S. income tax.

It’s important to note that the exclusion applies on a prorated basis if you do not meet the bona fide residence or physical presence test for the entire tax year. For instance, if you qualified for only half of the tax year, your maximum exclusion would be half of the annual limit.

The Foreign Tax Credit

While FEIE allows you to exclude income from U.S. taxation, the Foreign Tax Credit (FTC) offers an alternative or complementary approach. The FTC allows you to reduce your U.S. tax liability by the amount of income taxes you have paid to a foreign country.

- Choice between FEIE and FTC: In most cases, you cannot claim both the full FEIE and the full FTC on the same income. You generally have to choose which benefit to apply. However, there are situations where you might be able to use both. For example, if your foreign income exceeds the FEIE limit, you can exclude the portion up to the limit and then claim the FTC on the remaining income.

- Tax brackets: The FEIE is calculated on a “last-in, first-out” basis. This means that the excluded income is treated as the highest-taxed portion of your income. This can impact the tax bracket for your remaining U.S. taxable income.

- Benefits of FTC: The FTC can be particularly beneficial if you are in a country with a higher tax rate than the U.S., as it can potentially eliminate your U.S. tax liability altogether. It also doesn’t reduce your total income in the same way FEIE does, which can sometimes be advantageous for certain government benefits or deductions that are based on your gross income.

Filing Requirements: Form 2555

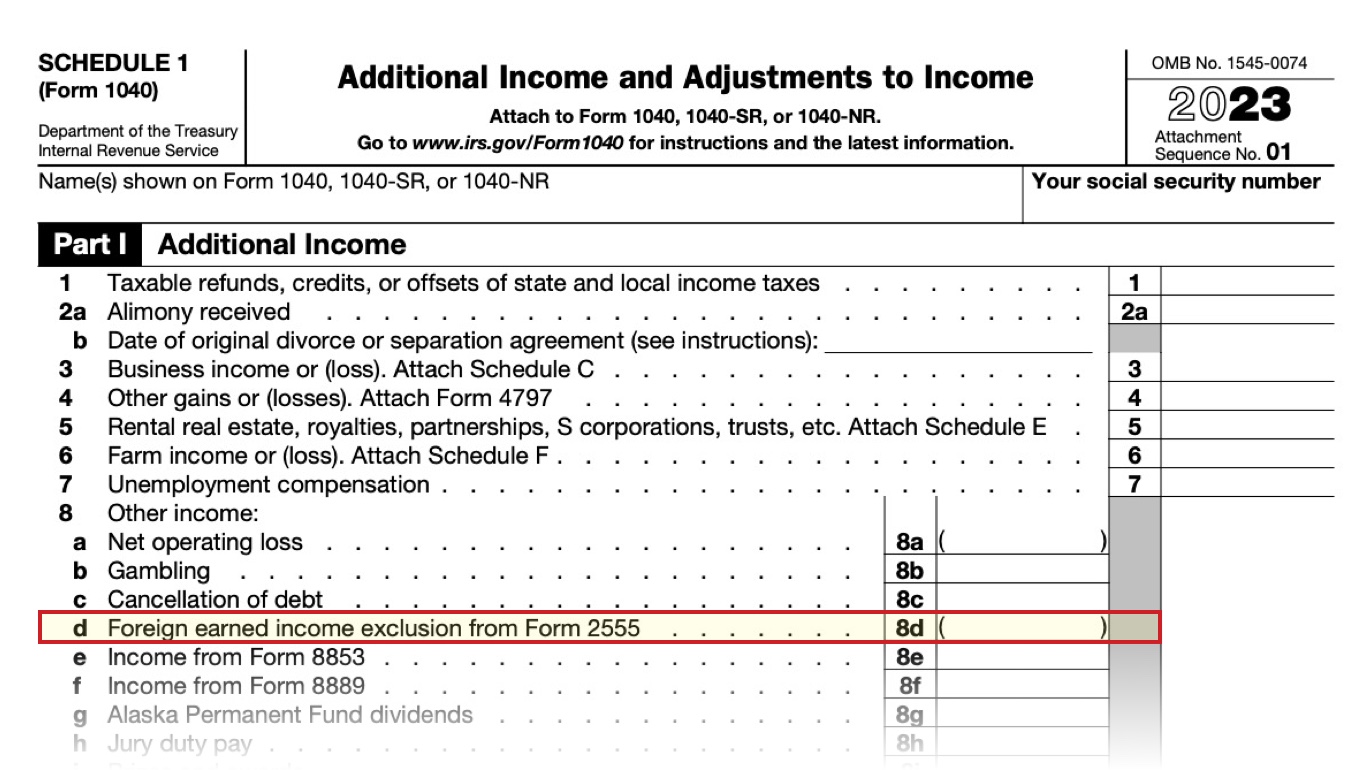

To claim the Foreign Earned Income Exclusion, you must file Form 2555, Foreign Earned Income Exclusion, with your U.S. federal income tax return (Form 1040). This form is where you will detail your foreign earned income, the period during which you qualified for the exclusion, and the calculated exclusion amount.

- When to file: Form 2555 should be filed with your annual U.S. federal income tax return. If you are living abroad and unable to meet the filing deadline, you can typically request an automatic extension by filing Form 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return.

- Accuracy is key: It is crucial to accurately complete Form 2555, providing all necessary documentation and calculations. Errors or omissions can lead to penalties and interest.

- Record keeping: Maintaining detailed records is paramount for supporting your FEIE claim. This includes:

- Pay stubs and employment contracts showing your foreign earnings.

- Records of your physical presence in foreign countries (e.g., flight itineraries, passport stamps).

- Documentation to support your bona fide residence if you are using that test (e.g., lease agreements, utility bills, tax returns from the foreign country).

Strategic Considerations for Expatriates

Beyond the basic mechanics of FEIE, there are strategic decisions expatriates should make to optimize their tax situation. This includes understanding the implications of FEIE on other tax benefits and planning for potential changes in tax laws.

Impact on Other Tax Benefits

Claiming the Foreign Earned Income Exclusion can have ripple effects on other tax benefits and deductions. Since FEIE reduces your adjusted gross income (AGI), it can affect the deductibility of certain expenses and the eligibility for various credits.

- IRA Contributions: The ability to contribute to a Traditional IRA is generally limited to the amount of compensation you have earned. If your compensation is significantly reduced by FEIE, your ability to contribute to an IRA may also be limited. However, if you have other compensation that is subject to U.S. tax, you might still be able to contribute.

- Deductible Medical Expenses: The deduction for medical expenses is subject to a percentage of your AGI. A lower AGI due to FEIE can reduce the amount of medical expenses you can deduct.

- Child Tax Credit: While the FEIE itself doesn’t directly disallow the Child Tax Credit, it’s essential to meet the residency requirements for the credit, which generally means having a Social Security number and living in the U.S. for more than half the year. Expatriates may need to carefully consider their U.S. residency status in relation to claiming this credit.

- Student Loan Interest Deduction: This deduction is also phased out based on your AGI. A lower AGI from FEIE can affect your ability to claim this deduction.

Tax Treaty Considerations

Many countries have tax treaties with the United States. These treaties are designed to prevent double taxation and often include provisions that can affect how foreign earned income is treated.

- Eliminating double taxation: Tax treaties can clarify which country has the primary right to tax certain types of income. In some cases, a treaty might override U.S. tax laws or provide additional exemptions or credits.

- Specific provisions: Some treaties may have specific clauses related to pensions, social security, or other forms of income that could impact an expatriate’s tax liability.

- Understanding treaty benefits: It’s crucial for expatriates to understand if a tax treaty exists between the U.S. and their country of residence and to review its provisions to ensure they are taking full advantage of any available benefits.

Planning for Repatriation and Future Tax Implications

As expatriates plan their return to the United States, understanding the implications of FEIE on their future tax situation is vital.

- Deemed Sale of Foreign Assets: Upon returning to the U.S., certain foreign assets might be subject to U.S. taxation. Understanding the basis of these assets and potential capital gains tax implications is important.

- Foreign Tax Credits: Any foreign taxes paid while abroad may be eligible for carryover to future U.S. tax years, which can help offset U.S. tax liability on foreign-source income earned after repatriation.

- Changing Tax Laws: Tax laws are subject to change. Expatriates should stay informed about any updates to FEIE or other relevant tax provisions that could affect their financial planning. Consulting with a tax professional experienced in international taxation is highly recommended to navigate these complexities effectively.

The Foreign Earned Income Exclusion is a significant tax provision that can greatly benefit U.S. citizens and resident aliens working abroad. By understanding the eligibility requirements, calculation methods, and strategic considerations, expatriates can effectively manage their U.S. tax obligations and ensure their financial well-being while living and working internationally.