Understanding what income counts towards Medicaid eligibility is a crucial aspect of navigating the healthcare system for many individuals and families. Medicaid, a joint federal and state program, provides health coverage to millions of Americans, but its eligibility criteria, particularly regarding income, can be complex and vary significantly by state. This article aims to demystify the process, offering a clear and comprehensive overview of how income is assessed for Medicaid, with a particular focus on how various types of income are treated.

Understanding the Basics of Medicaid Income Eligibility

Medicaid eligibility is determined by a combination of factors, including income, household size, disability status, and other specific criteria that are largely set by individual states within federal guidelines. For the majority of Medicaid pathways, income is assessed against the Federal Poverty Level (FPL). This means that a household’s total annual income is compared to a set of poverty guidelines published annually by the U.S. Department of Health and Human Services.

The Federal Poverty Level (FPL) and Income Thresholds

The FPL serves as the benchmark against which most Medicaid income eligibility is measured. States can set their income thresholds higher than the federal minimum, and many do, especially for specific populations like pregnant women, children, and individuals with disabilities.

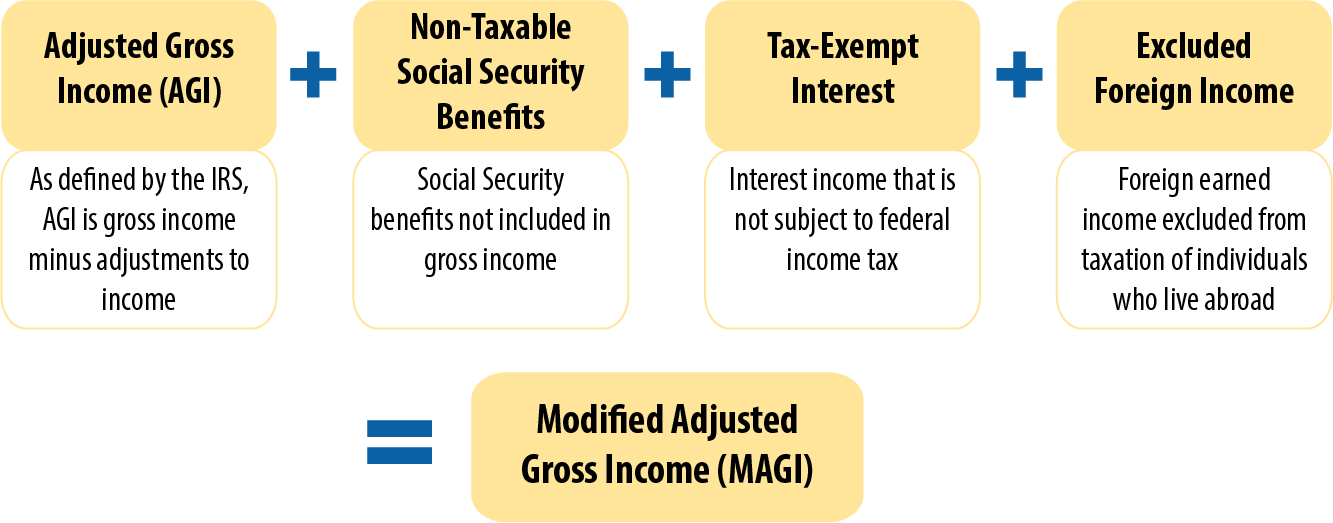

- Modified Adjusted Gross Income (MAGI): For many adults and children who do not qualify through specific disability or elderly pathways, income is calculated using the Modified Adjusted Gross Income (MAGI) methodology. This is the same income calculation used for the Affordable Care Act (ACA) marketplace plans. MAGI generally includes most forms of taxable income, such as wages, salaries, tips, self-employment income, unemployment benefits, interest, and dividends. It excludes certain deductions and non-taxable income.

- Non-MAGI Pathways: For individuals who are elderly or disabled, or who are seeking coverage through specific programs like Home and Community-Based Services (HCBS), a different income calculation known as “non-MAGI” may apply. This method often takes into account a broader range of income and allows for more deductions for medical expenses and other essential needs. It’s critical to understand which pathway applies to your situation.

Gross vs. Net Income: A Key Distinction

When discussing Medicaid income, it’s important to distinguish between gross income (total income before deductions) and net income (income after certain allowable deductions). While gross income is the starting point for most calculations, the actual “counted income” for Medicaid eligibility is often a net figure after specific adjustments.

- Standard Deductions and Allowances: Most states allow for standard deductions from gross income to arrive at the countable income. These deductions can vary by state and by the eligibility pathway. For example, a certain percentage of the gross income might be disregarded, or specific allowances might be made for work-related expenses.

- Household Size and Income: The size of the household is a significant factor in determining the FPL threshold. A larger household generally has a higher income limit for eligibility than a smaller one. Medicaid considers all individuals who live together and are financially dependent on each other as part of the household for income calculation purposes.

Types of Income That Count Towards Medicaid

The definition of “income” for Medicaid purposes is broad and encompasses most sources of money received by an applicant or recipient. However, there are nuances regarding what is considered taxable, what is considered a resource, and what is permanently excluded by law.

Earned Income: Wages, Salaries, and Self-Employment

Earned income, derived from working for an employer or through self-employment, is typically the primary component of income considered for Medicaid.

- Wages and Salaries: For individuals who are employed, their gross wages, including overtime and bonuses, are generally counted. However, as mentioned, deductions for taxes, Social Security, Medicare, and sometimes a portion of health insurance premiums may be allowed depending on the state and the specific eligibility category.

- Self-Employment Income: For those who are self-employed, income is usually calculated as gross receipts from the business minus ordinary and necessary business expenses. This means that expenses directly related to running the business, such as rent for office space, supplies, and utilities, can be deducted. However, personal expenses or disproportionately high “business” expenses designed to reduce countable income may be scrutinized. Documentation of all income and expenses is crucial for self-employed individuals applying for Medicaid.

Unearned Income: Investments, Benefits, and Other Sources

Unearned income refers to income received from sources other than active work. This category can be particularly complex due to the variety of sources and varying rules.

- Retirement Benefits: Pensions, annuities, and distributions from retirement accounts (like 401(k)s or IRAs) are generally considered unearned income. The amount counted is typically the gross distribution received, though for non-MAGI pathways, there might be specific rules regarding lump-sum distributions or the treatment of funds held in trust.

- Social Security Benefits: Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI) have different treatments. SSI payments are generally not counted as income for most Medicaid eligibility calculations for the recipient themselves, as SSI is designed to meet basic needs. SSDI benefits, however, are typically counted as unearned income. Spousal and survivor benefits from Social Security are also considered unearned income.

- Unemployment Compensation: Payments received from state unemployment agencies are considered taxable income and therefore count towards Medicaid eligibility.

- Interest and Dividends: Income from savings accounts, bonds, stocks, and other investments is counted as unearned income. This includes both interest earned and dividends paid out.

- Alimony and Child Support: Received alimony is typically counted as unearned income for the recipient. Child support payments received for children in the household are usually counted towards the household’s total income. However, there can be variations based on state law and the specific circumstances.

- Gifts and Contributions: Cash gifts and regular financial contributions from friends or family can be considered income if they are substantial and recurring. The state will assess whether these are truly gifts or if they represent a form of ongoing support that should be counted.

Non-Countable Income and Exclusions

Fortunately, not all money received is considered for Medicaid eligibility. Certain types of income are legally excluded or are not counted due to their nature or purpose. Understanding these exclusions can significantly impact eligibility.

Excluded Income Categories

- Certain Federal and State Assistance Programs: Many needs-based assistance programs, such as Temporary Assistance for Needy Families (TANF) cash benefits, are often excluded from countable income. This is because these programs are already designed to provide a safety net, and double-counting them would be punitive.

- In-Kind Benefits: Benefits received in non-cash form, such as food stamps (SNAP benefits) or housing assistance (Section 8 vouchers), are generally not counted as income.

- Reimbursements for Expenses: Payments that reimburse you for expenses you have already incurred are typically not counted as income. This could include reimbursement for mileage for work-related travel or reimbursement for approved medical expenses.

- Certain Educational Grants and Scholarships: Grants and scholarships specifically for tuition, fees, and required educational expenses are often excluded. However, any portion of a scholarship or grant that is used for living expenses might be counted.

- Loans: Money received as a loan, where there is a clear intent to repay, is generally not considered income. This includes student loans, personal loans, and certain business loans. Documentation proving the loan agreement is essential.

- Home and Property: The value of a primary residence is generally not counted as income for Medicaid eligibility purposes, though it may be considered a resource in some long-term care eligibility scenarios (Medicaid Estate Recovery). Similarly, certain resources like a single vehicle used for transportation or household goods are typically excluded.

Income Deductions and Disregards

Beyond outright exclusions, states also offer various deductions and “disregards” that reduce the amount of income that counts towards the eligibility threshold.

- Earned Income Disregard: For MAGI pathways, states often disregard a certain percentage of earned income (e.g., 15% or 20%) to account for work-related expenses and encourage employment.

- Dependent Care Expenses: Costs incurred for the care of dependents (children or incapacitated adults) to allow the applicant to work may be deductible.

- Medical Expenses: In non-MAGI pathways, particularly for individuals with disabilities or the elderly, incurred medical expenses that are not covered by other insurance can often be deducted from income, effectively increasing eligibility. This is sometimes referred to as a “medical expense deduction” or “spend-down.”

- Child Support Paid to Others: If an applicant is legally obligated to pay child support for children who do not live in their household, these payments can be deducted from their income.

Navigating the Application Process and Seeking Assistance

Applying for Medicaid requires careful attention to detail and accurate reporting of all income and resources. Mistakes or omissions can lead to delays or denial of benefits.

Documentation is Key

When applying for Medicaid, be prepared to provide thorough documentation for all sources of income. This includes:

- Pay stubs for recent months.

- Tax returns (federal and state) from the previous year.

- Bank statements showing deposits and withdrawals.

- Letters or statements from Social Security, pensions, or other benefit providers.

- Documentation of any self-employment income and expenses.

- Loan agreements, gift letters, or any other documentation that clarifies the nature of money received.

State-Specific Variations and Resources

It is vital to remember that Medicaid rules, including income calculations, vary significantly from state to state. What counts as income in one state might be treated differently in another.

- State Medicaid Agencies: The most reliable source of information for your specific situation is your state’s Medicaid agency. Their websites typically provide detailed guides, eligibility calculators, and application forms.

- Navigators and Assisters: For individuals applying through the ACA marketplace or seeking general assistance, certified navigators and application assisters are available to help you understand your options and complete your application accurately, free of charge.

- Legal Aid Societies and Advocacy Groups: If you believe your income has been incorrectly assessed or if you face complex eligibility issues, legal aid societies and healthcare advocacy groups can provide invaluable assistance and representation.

In conclusion, understanding what income counts for Medicaid is a multifaceted process that involves understanding different methodologies like MAGI and non-MAGI, identifying various sources of earned and unearned income, and being aware of exclusions and deductions. By thoroughly documenting your financial situation and consulting with your state’s Medicaid agency or available assistance programs, you can navigate this complex system more effectively and secure the healthcare coverage you need.