Understanding the Role of Escrow in Homeownership

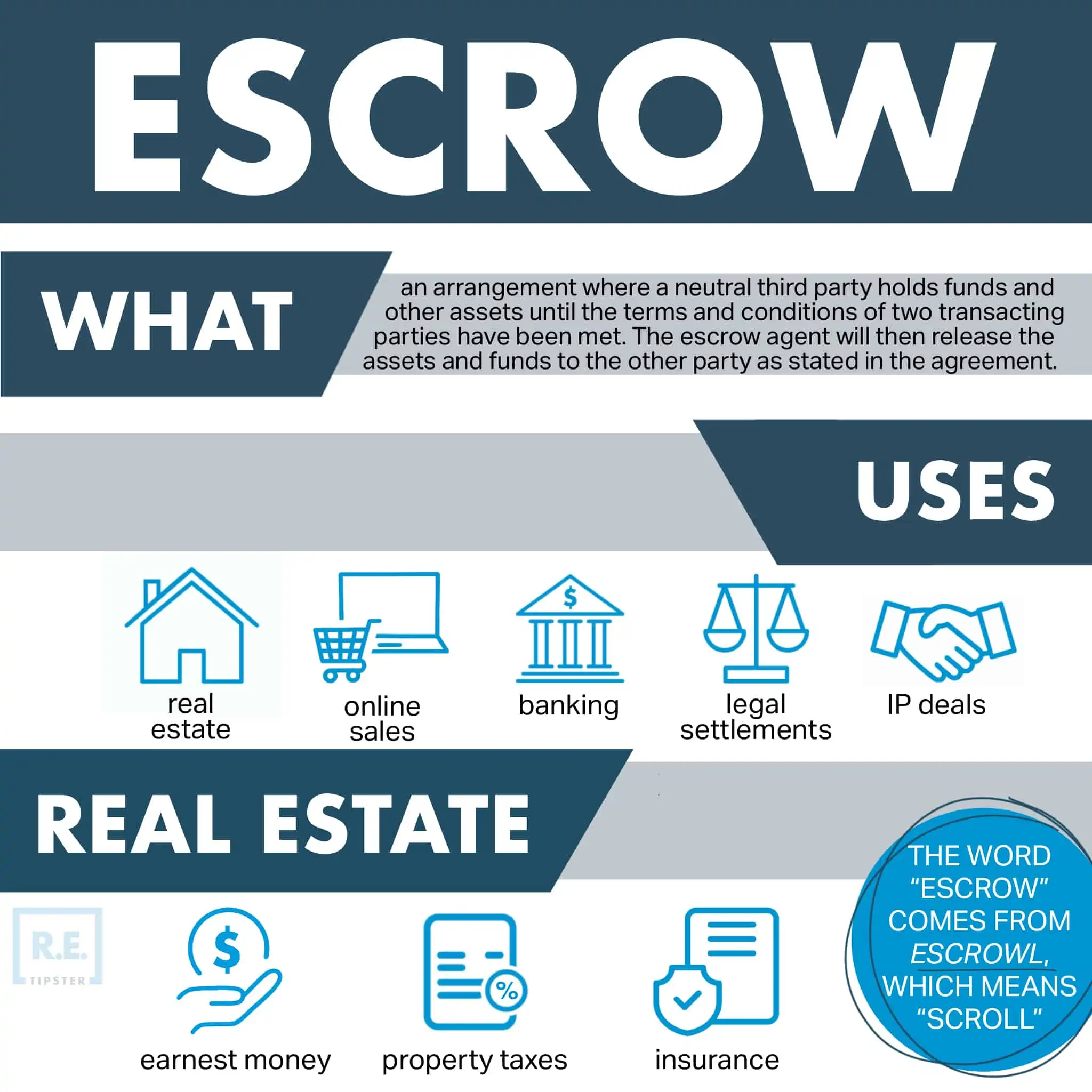

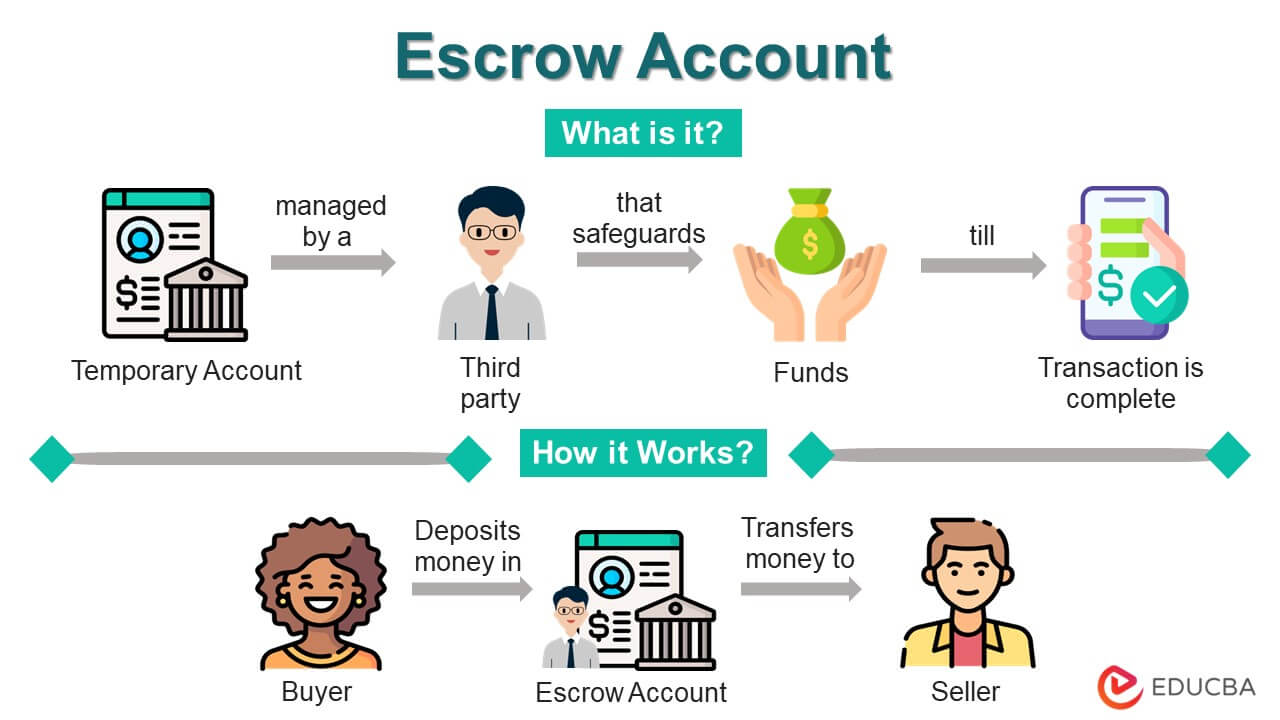

The term “escrow” can sound like a complex financial or legal jargon, especially when it’s introduced during the process of securing a home loan. However, at its core, escrow is a crucial mechanism designed to protect both the borrower and the lender throughout the life of the mortgage. It acts as a neutral third party that holds funds and documents related to your home loan, ensuring that specific obligations are met before these assets are released. Essentially, it’s a safeguard that simplifies and secures the intricate transaction of buying a home and managing ongoing mortgage responsibilities.

For many, the concept of escrow first surfaces when they are in the process of closing on a new home. At this stage, escrow is instrumental in ensuring all conditions of the purchase agreement are satisfied. Funds are deposited into an escrow account, and once all parties have fulfilled their promises – the buyer has secured financing, the seller has clear title, and all inspections are satisfactory – the escrow agent facilitates the transfer of ownership. But the role of escrow doesn’t end at closing. For the duration of your mortgage, an escrow account will continue to be managed to handle payments for property taxes and homeowner’s insurance, thereby protecting the lender’s investment and ensuring these vital homeowner obligations are met on time.

The Escrow Process at Closing

The period leading up to the finalization of a real estate transaction is often referred to as the “escrow period.” During this time, a neutral third party, known as the escrow officer or agent, acts as a custodian for all funds and documents related to the sale. This agent ensures that all contingencies outlined in the purchase agreement are met before the transaction is officially completed.

Holding Funds and Documents

Once a buyer and seller have agreed on the terms of a sale and signed a purchase agreement, the buyer typically deposits an earnest money deposit into an escrow account. This deposit signifies the buyer’s serious intent to purchase the property. The escrow agent holds these funds securely. Additionally, important documents such as the deed, mortgage note, and title insurance policies are also held in escrow. The escrow agent acts as a central repository, ensuring that no party can unilaterally alter or withdraw from the agreement without the consent of the other, or without fulfilling the agreed-upon conditions.

Verifying and Fulfilling Contingencies

The escrow period is also when various contingencies are addressed. These can include the buyer securing final mortgage approval, a satisfactory home inspection, an appraisal that meets or exceeds the purchase price, and a clear title search. The escrow agent works with all parties – the buyer, seller, lender, title company, and sometimes attorneys – to ensure that each of these conditions is met according to the terms of the contract. For example, the escrow agent will coordinate with the lender to confirm the buyer’s financing is in place and will receive the loan funds from the lender. They will also ensure that any necessary repairs identified during the inspection are completed.

Facilitating the Transfer of Ownership

Upon successful fulfillment of all contingencies, the escrow agent orchestrates the final closing. This involves disbursing funds from the escrow account to the seller, paying off any existing liens on the property, covering closing costs for both parties, and issuing payments to real estate agents, inspectors, and other service providers. Simultaneously, the deed is recorded with the appropriate government office, officially transferring ownership of the property to the buyer. The escrow agent ensures that all parties have signed the necessary paperwork and that all financial obligations have been settled before releasing the deed to the new homeowner. This systematic process, managed by the escrow agent, provides a secure and orderly transfer of property and funds.

Ongoing Escrow for Mortgage Payments

Beyond the initial closing, escrow plays a vital ongoing role in managing your mortgage. Most mortgage lenders require an escrow account to be set up as a condition of the loan. This account is used to collect funds from the borrower on a monthly basis to cover property taxes and homeowner’s insurance premiums, ensuring these critical expenses are paid on time and protecting the lender’s interest in the property.

Collecting and Holding Funds for Taxes and Insurance

Each month, as part of your total mortgage payment, a portion is allocated to your escrow account. This amount is calculated based on the estimated annual costs of your property taxes and homeowner’s insurance. The lender, or a third-party servicer acting on their behalf, manages this account. They collect these funds from you and hold them until the tax bills or insurance premiums are due. This system essentially allows you to pay for these significant annual expenses in smaller, manageable monthly installments, preventing a large, unexpected financial burden.

Paying Property Taxes and Homeowner’s Insurance

When your property tax bills are issued by your local government, the lender will use the funds held in your escrow account to pay them on your behalf. Similarly, when your homeowner’s insurance policy renews, the premium will be paid from your escrow account. This proactive payment system ensures that your taxes are always up-to-date, preventing potential tax liens, and that your property remains insured, protecting it from damage and loss. Lenders require this to safeguard their investment; if taxes are unpaid, the government could place a lien on the property, which would take priority over the mortgage. Likewise, without insurance, the property’s value could be significantly diminished by an unforeseen event, leaving the lender with little recourse.

Annual Escrow Analysis and Adjustments

Once a year, the entity managing your escrow account (typically your mortgage lender or their servicing company) will conduct an escrow analysis. This process reviews the actual costs of your property taxes and homeowner’s insurance over the past year and compares them to the amount collected in your escrow account. Based on this analysis, they will determine if there is a surplus or a deficit in your account.

If there is a surplus, meaning you’ve paid more than was needed, the excess funds will typically be refunded to you. If there is a deficit, meaning you haven’t paid enough to cover the upcoming tax and insurance bills, your monthly escrow payment will be adjusted upwards to compensate for the shortfall. This adjustment ensures that there are sufficient funds in the account to cover future expenses. The lender is legally obligated to provide you with an escrow statement detailing this analysis and any resulting changes to your payment. While these adjustments can sometimes lead to an increase in your monthly payment, they are a necessary part of ensuring your ongoing financial obligations are met.

Benefits and Potential Drawbacks of Escrow

The escrow system, both at closing and for ongoing mortgage payments, offers distinct advantages that contribute to a smoother and more secure homeownership experience. However, like any financial arrangement, there are also potential downsides to consider. Understanding these aspects can help homeowners navigate the escrow process more effectively.

Advantages for Borrowers and Lenders

For borrowers, the primary advantage of an ongoing escrow account is the convenience and predictability it offers for managing large, periodic expenses like property taxes and homeowner’s insurance. Instead of having to save up a significant sum annually, homeowners can spread these costs out over twelve months, making budgeting much easier and reducing the risk of being caught off guard by large bills. This also removes the stress of remembering payment due dates and the potential for late fees or penalties.

From a lender’s perspective, escrow is an essential risk management tool. By ensuring that property taxes are paid, they protect their collateral from government liens. By ensuring that homeowner’s insurance is maintained, they protect their investment from damage. This significantly reduces the likelihood of a borrower defaulting due to these critical expenses, ultimately contributing to the stability of the mortgage market. The escrow process at closing also provides a layer of security by ensuring that all contractual obligations are met before the property and funds are transferred, preventing potential disputes and ensuring a clean transaction.

Potential Concerns and Considerations

While beneficial, the escrow system isn’t without its potential concerns. One common point of frustration for homeowners is the lack of direct control over the funds held in escrow. The money is managed by the lender or servicer, and while it’s intended for specific purposes, homeowners don’t have immediate access to it. Furthermore, escrow accounts do not typically earn interest, meaning that the funds held within them are not generating any return for the homeowner, while the lender may be able to benefit from the float.

Another consideration is the potential for escrow payment adjustments. While necessary for accuracy, increases in monthly escrow payments can sometimes be unexpected and can strain a household budget. Homeowners should stay informed about their escrow statements and understand the factors that influence these adjustments, such as rising property tax rates or increased insurance premiums. It’s also important to be aware of potential errors; while rare, mistakes can happen in escrow accounting. Regularly reviewing your escrow statements and mortgage statements can help identify and rectify any discrepancies promptly. Understanding your rights and responsibilities regarding escrow can empower you to manage this aspect of your home loan with greater confidence.