Choosing the right bank is a foundational decision for any individual or business, impacting everything from daily transactions to long-term financial goals. In the rapidly evolving landscape of financial services, the concept of “what bank does one use” has expanded beyond traditional brick-and-mortar institutions. Today, a multitude of options exist, each with its unique set of offerings, technological capabilities, and customer service philosophies. This article delves into the considerations that should guide your choice, exploring the diverse spectrum of banking solutions available and how to align them with your specific needs.

Understanding Your Banking Needs: A Personalized Approach

Before even considering which institution to patronize, a thorough assessment of your personal or business financial requirements is paramount. This self-reflection is the cornerstone of making an informed decision, ensuring that the bank you choose will not only meet your current demands but also support your future growth and aspirations. The notion of a one-size-fits-all banking solution is increasingly outdated; instead, a tailored approach is essential.

Assessing Transactional Habits and Preferences

The most fundamental aspect of banking revolves around managing day-to-day transactions. Think about your typical financial activities: how often do you visit a physical branch? Do you primarily use online banking or mobile apps for transfers, bill payments, and checking balances? Are you frequently making international transfers, or do you rely heavily on cash deposits and withdrawals? Understanding these habits will help you prioritize banks that excel in the areas most important to you. For instance, if you are a digital native who rarely visits a physical branch, an online-only bank with a robust mobile platform might be ideal. Conversely, if you value face-to-face interaction and require services like notary publics or safe deposit boxes, a traditional bank with a strong branch network might be a better fit.

Evaluating Service Requirements: Beyond Basic Transactions

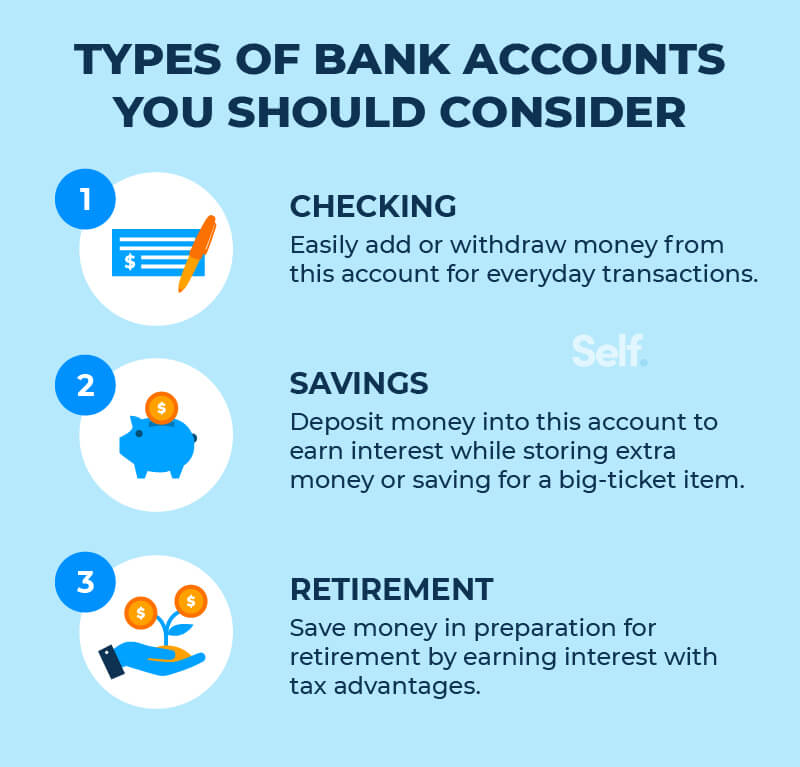

Beyond routine transactions, consider the broader range of services you might need. This could include savings accounts with competitive interest rates, robust investment options, loan products (mortgages, auto loans, personal loans), or business banking services such as merchant accounts and lines of credit. If you are a small business owner, you might need specialized services like payroll processing, cash management, or access to small business administration (SBA) loans. For individuals, services like financial planning, retirement accounts, or wealth management might be crucial. The more complex your financial life, the more important it becomes to partner with a bank that offers a comprehensive suite of services and expertise to support your multifaceted needs.

Considering Technological Integration and User Experience

In the digital age, the banking technology offered by an institution is as important as its physical presence. Evaluate the user-friendliness of their online banking portal and mobile application. Features like intuitive navigation, robust security measures, real-time account alerts, mobile check deposit, and seamless integration with budgeting tools can significantly enhance your banking experience. If you are interested in emerging technologies, some banks offer advanced features like artificial intelligence-powered financial advice, peer-to-peer payment integrations, or even cryptocurrency services. The quality of the digital interface is no longer a secondary consideration; it is a primary determinant of convenience and efficiency.

Exploring the Banking Landscape: Traditional vs. Digital

The banking world can broadly be categorized into two primary models: traditional banks and digital banks (often referred to as challenger banks or neobanks). Each has its distinct advantages and disadvantages, catering to different customer segments and preferences. Understanding these fundamental differences is key to narrowing down your options.

The Enduring Strength of Traditional Banks

Traditional banks, with their established history and physical branch networks, offer a tangible sense of security and accessibility for many. They typically provide a full spectrum of financial services, from basic checking and savings accounts to complex lending products, wealth management, and international banking. For customers who prefer face-to-face interactions, personalized advice from a banker, or require services only available at a physical location, traditional banks remain a compelling choice. Their extensive branch networks can be particularly advantageous for businesses that rely on cash transactions or for individuals who appreciate the convenience of in-person assistance. Furthermore, many traditional banks have invested heavily in their digital platforms, offering sophisticated online and mobile banking services that rival their digital-only counterparts.

The Rise of Digital-First Banking

Digital banks, on the other hand, operate primarily or exclusively online, often without physical branches. This lean operational model allows them to offer highly competitive interest rates on savings accounts, lower fees, and innovative digital tools. They are built with a mobile-first philosophy, providing seamless and intuitive app experiences that cater to a tech-savvy clientele. Digital banks often excel in specific niches, such as offering specialized accounts for freelancers, providing budgeting and savings tools, or facilitating international money transfers with lower fees. For individuals who are comfortable managing their finances entirely through an app and prioritize cost savings and cutting-edge technology, digital banks present an attractive alternative to traditional institutions.

Key Factors for Differentiating Banking Institutions

Once you have a clear understanding of your needs and the broad categories of banks, it’s time to delve into the specific factors that differentiate one institution from another. These details can significantly influence your long-term satisfaction and the overall effectiveness of your banking relationship.

Fee Structures and Account Costs

Fees are a critical consideration, as they can erode the value of your deposits and increase the cost of your banking. Carefully examine the fee schedules for all account types you are considering. Look out for monthly maintenance fees, ATM fees (especially for out-of-network transactions), overdraft fees, wire transfer fees, and fees associated with specific services like paper statements or stop payments. Some banks offer fee waivers for maintaining minimum balances, direct deposit arrangements, or by opting for specific account tiers. Digital banks often boast lower or no fees for basic services, which can be a significant draw for cost-conscious consumers. However, it’s essential to compare the overall fee structure, as sometimes a traditional bank might have fewer fees for certain services if you meet their specific criteria.

Interest Rates and Returns on Savings

For savings accounts, checking accounts that earn interest, and certificates of deposit (CDs), the interest rate offered is a primary determinant of your financial growth. Compare Annual Percentage Yields (APYs) across different institutions. Digital banks, due to their lower overhead, often offer significantly higher APYs on savings accounts than traditional banks. This can lead to substantial differences in how much your savings grow over time. It’s also important to understand how interest is compounded (daily, monthly, etc.) and whether there are any tiered interest rates that reward larger balances. For investments, consider the breadth of investment products offered and the associated fees for managing those investments.

Customer Service and Support Channels

The quality of customer service can be a deal-breaker. While digital banks offer convenience, their customer support might be limited to online chat or email. Traditional banks, with their branch networks, provide the option of in-person assistance, which can be invaluable for resolving complex issues or for those who prefer a human touch. Evaluate the availability and responsiveness of customer support across all channels: phone, email, chat, and in-person. Consider reading customer reviews to gauge the typical experience with each bank’s support team. A bank that is difficult to reach or slow to resolve issues can lead to frustration and missed opportunities.

Security and Regulatory Compliance

Trust is paramount in banking, so understanding the security measures and regulatory oversight of an institution is crucial. Reputable banks are insured by governmental bodies like the Federal Deposit Insurance Corporation (FDIC) in the United States or similar agencies in other countries, which protects your deposits up to a certain limit. Look for banks that employ robust cybersecurity measures, including multi-factor authentication, encryption, and fraud monitoring. Be wary of any institution that seems too good to be true or lacks clear information about its security protocols and regulatory standing. A secure banking environment protects your funds and your personal information from potential threats.

Making the Final Decision: Aligning Choice with Lifestyle

The decision of “what bank does one use” ultimately boils down to aligning the offerings of a financial institution with your individual lifestyle, financial goals, and comfort level with technology. There is no single “best” bank, but rather the “best” bank for you.

Prioritizing Convenience and Accessibility

For some, convenience and accessibility are paramount. This might mean choosing a bank with a branch in their neighborhood for easy access to cash deposits or to speak with a banker. For others, convenience means having a top-tier mobile app that allows them to manage all their finances from anywhere in the world. Consider your daily routine and how your banking needs fit into it. If you’re a frequent traveler, a bank with a strong international presence or excellent mobile banking capabilities for foreign transactions might be your priority.

Aligning with Financial Goals and Future Aspirations

Your choice of bank should also support your long-term financial aspirations. If you are saving for a down payment on a house, a bank offering competitive mortgage rates and financial advisory services could be beneficial. If you are focused on retirement planning, an institution with robust investment and wealth management services might be the best fit. For business owners, the availability of business loans, lines of credit, and merchant services can be critical for growth and expansion. A bank that understands and can support your future goals will be a valuable partner throughout your financial journey.

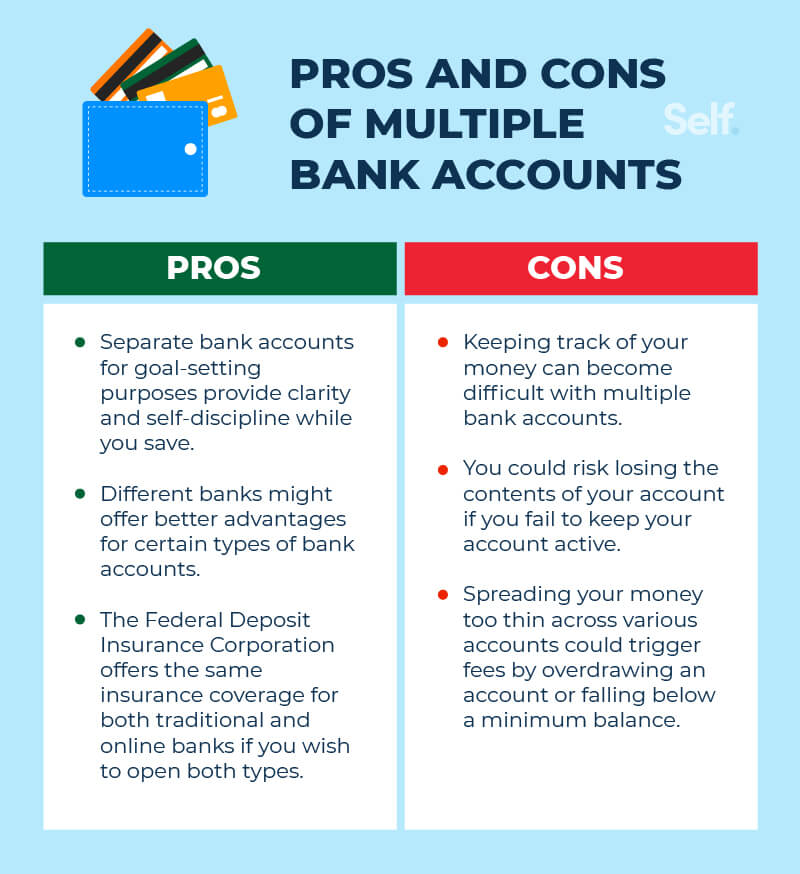

The Power of Multiple Banking Relationships

It’s also important to recognize that you are not limited to a single banking relationship. Many individuals and businesses utilize multiple banks to leverage the strengths of different institutions. For example, you might keep your primary checking account with a traditional bank for its convenient branch access and use a digital bank for your savings to earn a higher interest rate. You might also have a separate investment account with a specialized brokerage firm. This diversified approach can help you optimize your banking experience, mitigate risks, and take advantage of the best offerings available in the market. By carefully considering your needs and exploring the diverse landscape of financial institutions, you can make an informed decision that sets you on a path to financial success.