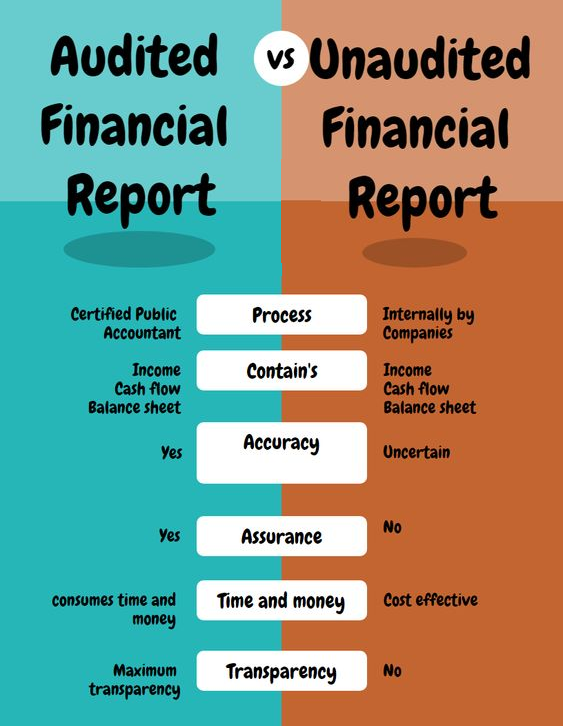

Audited financials represent a crucial cornerstone of transparency and trust within the business world. At their core, they are financial statements that have undergone a rigorous examination by an independent third-party auditor. This process aims to provide assurance that the company’s financial information is presented fairly, accurately, and in accordance with generally accepted accounting principles (GAAP) or other relevant accounting standards. For investors, creditors, regulators, and even internal management, audited financials offer a vital layer of credibility, enabling informed decision-making and fostering confidence in the organization’s financial health and operations.

The Purpose and Importance of Financial Audits

The fundamental purpose of an audited financial statement is to enhance the reliability and credibility of a company’s financial reporting. In today’s complex economic landscape, where stakeholders rely heavily on financial data to assess a company’s performance and prospects, the risk of misstatement or fraud, whether intentional or unintentional, is ever-present. An independent audit acts as a critical safeguard, providing an objective assessment that can uncover material inaccuracies.

Enhancing Stakeholder Confidence

For external stakeholders, such as potential investors, lenders, and suppliers, audited financials are often a prerequisite for engagement. Investors, in particular, need to be confident that the financial statements accurately reflect the company’s profitability, assets, liabilities, and cash flows before committing capital. Lenders rely on these statements to assess a company’s creditworthiness and its ability to repay loans. The auditor’s opinion, appended to the financial statements, serves as a signal of trust, indicating that a professional review has taken place. This confidence can translate into better access to capital, more favorable loan terms, and stronger business relationships.

Ensuring Compliance and Accountability

Audited financials also play a significant role in ensuring compliance with various regulatory requirements. Publicly traded companies, for instance, are mandated by securities regulators (like the Securities and Exchange Commission in the US) to have their financial statements audited annually. This ensures that these companies adhere to strict reporting standards and provide accurate information to the investing public. Beyond regulatory mandates, audits also promote internal accountability. They can highlight weaknesses in internal controls and financial processes, prompting management to implement improvements and prevent future errors or fraudulent activities. This focus on accountability strengthens the overall governance of the organization.

Facilitating Strategic Decision-Making

While the primary audience for audited financials is often external, they are also invaluable for internal decision-making. A comprehensive audit provides management with a deep understanding of the company’s financial position, its strengths, and its vulnerabilities. The insights gained from the audit process can inform strategic planning, identify areas for cost savings, optimize resource allocation, and guide investment decisions. By having a clear and accurate picture of the company’s financial performance, leadership can make more informed and effective strategic choices that drive long-term growth and sustainability.

The Audit Process: A Deep Dive

The process of auditing financial statements is a systematic and thorough endeavor, involving a series of steps designed to gather sufficient appropriate audit evidence and form an opinion on the fairness of the financial statements. This process is conducted by qualified and independent auditors, typically certified public accountants (CPAs) or chartered accountants (CAs).

Planning and Risk Assessment

The audit begins with extensive planning. Auditors meet with management to understand the company’s business, its industry, its organizational structure, and its internal control systems. A critical part of this phase is identifying and assessing risks of material misstatement. This involves considering factors such as the complexity of transactions, the likelihood of fraud or error, and the effectiveness of internal controls. The auditor’s risk assessment directly influences the nature, timing, and extent of audit procedures to be performed. For instance, areas with higher identified risks will necessitate more detailed and rigorous testing.

Performing Audit Procedures

Once the plan is established, auditors execute a range of procedures to gather evidence. These procedures can be broadly categorized into:

- Inquiry: Asking questions of management and other personnel within the organization.

- Observation: Witnessing processes or procedures being performed by others.

- Inspection: Examining documents, records, and other tangible assets. This might involve reviewing invoices, contracts, bank statements, and physical inventory counts.

- Confirmation: Obtaining direct verification from third parties, such as customers or suppliers, to corroborate balances or transactions.

- Recalculation: Checking the mathematical accuracy of documents or records.

- Analytical Procedures: Evaluating financial information by studying plausible relationships among both financial and non-financial data. This involves analyzing trends, ratios, and comparisons to identify any unusual fluctuations or inconsistencies.

These procedures are applied to all significant accounts and disclosures within the financial statements, including revenues, expenses, assets, liabilities, and equity.

Evaluation and Reporting

After gathering sufficient audit evidence, the auditor evaluates the findings. This involves assessing whether any identified misstatements are material, either individually or in aggregate, and whether they have been appropriately corrected by management. The auditor also evaluates the overall presentation of the financial statements to ensure they conform to the applicable accounting framework.

The culmination of the audit is the auditor’s report, which is an independent opinion on the financial statements. The most common type of report is an unqualified opinion (also known as a clean opinion), which states that the financial statements present fairly, in all material respects, the financial position of the company as of a given date and the results of its operations and its cash flows for the periods then ended. In certain circumstances, the auditor may issue a qualified opinion, an adverse opinion, or a disclaimer of opinion, depending on the scope and nature of any identified issues.

Types of Audited Financial Statements and Opinions

While the term “audited financials” generally refers to the complete set of financial statements, it’s important to understand which statements are typically included and the nuances of the auditor’s opinion.

Key Financial Statements

An audit typically covers the following core financial statements:

- Statement of Financial Position (Balance Sheet): This statement presents a company’s assets, liabilities, and equity at a specific point in time, offering a snapshot of its financial health.

- Statement of Comprehensive Income (Income Statement): This statement details a company’s revenues, expenses, gains, and losses over a specific period, demonstrating its profitability.

- Statement of Cash Flows: This statement tracks the movement of cash into and out of a company, categorized into operating, investing, and financing activities, providing insight into its liquidity.

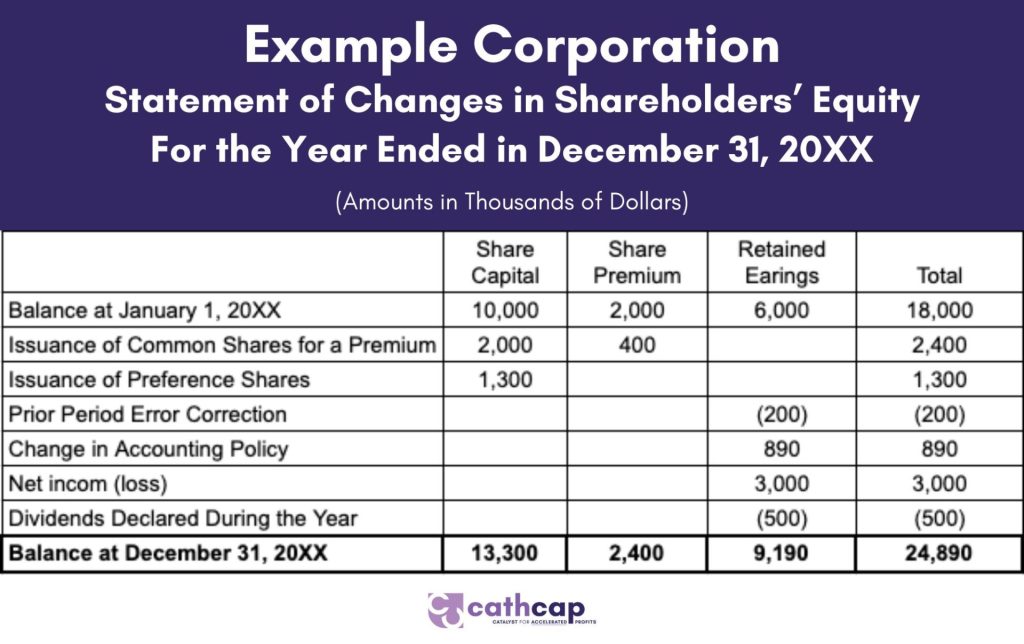

- Statement of Changes in Equity: This statement reconciles the beginning and ending balances of equity accounts, showing how changes in retained earnings, share capital, and other equity components have affected the overall equity of the company.

These statements, along with accompanying notes and disclosures, form the comprehensive financial package that is subjected to audit.

Auditor’s Opinions

The auditor’s opinion is the formal conclusion of the audit and is crucial for interpreting the reliability of the financial statements.

- Unqualified Opinion: This is the most common and favorable opinion. It indicates that the financial statements are presented fairly in all material respects, in accordance with the relevant accounting standards. This provides the highest level of assurance to stakeholders.

- Qualified Opinion: Issued when the auditor concludes that, except for a specific matter, the financial statements are presented fairly. This exception could be due to a scope limitation (where the auditor could not obtain sufficient evidence for a particular area) or a departure from accounting principles that is material but not pervasive.

- Adverse Opinion: This is the most severe type of opinion. It is issued when the auditor concludes that the financial statements, taken as a whole, do not present fairly, in accordance with the relevant accounting standards, due to a material and pervasive departure from these principles. An adverse opinion signals significant problems with the financial reporting.

- Disclaimer of Opinion: This occurs when the auditor is unable to obtain sufficient appropriate audit evidence to form an opinion on the financial statements. This can happen if the scope of the audit is significantly limited, preventing the auditor from gathering the necessary information to support a conclusion.

Understanding the type of opinion provided is as important as understanding that the financials have been audited.

Who Needs Audited Financials?

The requirement and benefit of audited financials extend across a broad spectrum of entities and situations. While public companies are legally obligated, many private entities also find audits essential for their operations and growth.

Publicly Traded Companies

As previously mentioned, companies whose shares are traded on public stock exchanges are subject to stringent regulatory oversight. These regulations mandate annual audits to protect public investors. This is to ensure transparency and prevent the kind of financial misconduct that can erode investor confidence and destabilize markets.

Private Companies Seeking Investment or Loans

Even without a public listing, private companies often require audited financials when seeking significant external funding. Venture capitalists, private equity firms, and traditional lenders will almost invariably demand audited statements as part of their due diligence process. This allows them to independently verify the financial claims made by the company and assess the associated investment or lending risks.

Businesses Involved in Mergers and Acquisitions

During the process of buying or selling a business, audited financial statements are a critical component of the transaction. They provide potential buyers with a clear and independently verified picture of the target company’s financial performance and health, which is essential for valuation and negotiation. Similarly, sellers may want audited financials to present their company in the most favorable and credible light.

Non-Profit Organizations

Non-profit organizations, while not profit-driven, still require transparency and accountability to their donors, grantors, and the public. Many grant-making bodies and government agencies mandate audits for non-profits to ensure that funds are being used effectively and for their intended purposes. Audited financials help build trust and demonstrate responsible stewardship of resources.

Businesses Experiencing Growth or Complexity

As businesses grow and their operations become more complex, the need for robust financial reporting and assurance increases. Even if not legally required, a private company that is expanding rapidly, entering new markets, or undertaking significant new projects may benefit from an audit to ensure its internal financial reporting systems are sound and its financial position is accurately understood by management. In essence, audited financials are a mark of financial maturity and a vital tool for building trust and facilitating responsible business practices across diverse organizational structures.