Navigating the complexities of medical insurance can often feel like deciphering a foreign language, especially when you’re unsure of your current coverage. This is a common predicament, arising from job changes, shifts in personal circumstances, or simply a lack of clear documentation. Fortunately, uncovering the details of your medical insurance is a straightforward process if you know where to look and what information to gather. This guide will walk you through the most effective methods to determine exactly what medical insurance you have, ensuring you can access the care you need with confidence.

Understanding Your Potential Insurance Avenues

Before delving into the specifics of how to find your insurance, it’s crucial to consider the most common ways people obtain medical coverage. This understanding will help you target your search more effectively. Whether you’re employed, self-employed, a student, or reliant on government programs, each scenario presents unique avenues for obtaining insurance.

Employer-Sponsored Insurance

For many individuals, medical insurance is a benefit provided by their employer. This is often the most comprehensive and cost-effective option available. If you are currently employed or have recently left a job, this is a primary area to investigate. Employers typically offer a selection of plans, and the specifics of your coverage will depend on the plan you or your employer selected.

- During Employment: If you are currently working, your employer’s Human Resources (HR) department is your first point of contact. They manage all employee benefits, including health insurance. They can provide you with your plan documents, explain your coverage options, and answer any questions you might have about deductibles, co-pays, co-insurance, and out-of-pocket maximums. It’s a good practice to request a summary of benefits and coverage (SBC) document, which clearly outlines what your plan covers and at what cost.

- After Employment (COBRA/State Continuation): If you have recently lost your job, you may be eligible to continue your employer-sponsored health insurance through COBRA (Consolidated Omnibus Budget Reconciliation Act) or a state continuation program. These programs allow you to maintain your existing coverage for a limited period, though you will likely be responsible for paying the full premium, which can be significantly higher than what you paid while employed. Your former employer should have provided you with COBRA election paperwork. If not, contact their HR department immediately to inquire about your continuation rights.

Government-Sponsored Health Insurance Programs

In the United States, several government programs provide health insurance to eligible individuals and families. Understanding these programs is vital, especially if you don’t have employer-sponsored coverage.

- Medicare: Medicare is a federal health insurance program primarily for people aged 65 or older, certain younger people with disabilities, and people with End-Stage Renal Disease. If you are in one of these categories, you might have Medicare. You can check your eligibility and enrollment status by visiting the official Medicare website (medicare.gov) or by contacting the Social Security Administration. Your Medicare card will have your Medicare number and the effective dates of your coverage.

- Medicaid: Medicaid is a joint federal and state program that helps cover medical expenses for people with limited income and resources. Eligibility varies by state. If you believe you might qualify for Medicaid, you should contact your state’s Medicaid agency or visit the healthcare marketplace website for your state. You can typically apply online or by mail.

- Children’s Health Insurance Program (CHIP): CHIP provides low-cost health coverage to children in families who earn too much money to qualify for Medicaid but cannot afford private insurance. Similar to Medicaid, CHIP programs are managed at the state level. You can find information and application details through your state’s CHIP website or the healthcare marketplace.

- Affordable Care Act (ACA) Marketplace: The ACA Marketplace (healthcare.gov or your state’s specific marketplace website) is a crucial resource for individuals and families who do not have access to employer-sponsored insurance, Medicare, or Medicaid. You can browse and compare different health plans offered by private insurers and enroll in a plan during the annual open enrollment period or if you qualify for a Special Enrollment Period due to a qualifying life event (e.g., losing other coverage, getting married, having a baby).

Private Health Insurance

If you don’t have coverage through an employer or government program, you likely obtained private health insurance on your own. This could be through the ACA Marketplace or directly from an insurance company.

- Purchased Through the ACA Marketplace: If you enrolled in a plan through healthcare.gov or your state’s marketplace, your insurance provider and plan details will be listed on your enrollment confirmation documents. You can log back into your Marketplace account to access this information, or you can contact the specific insurance company directly.

- Purchased Directly from an Insurer: If you purchased insurance directly from an insurance company without using the Marketplace, you will have received policy documents from that insurer. Your insurance card will also list the company’s name. If you’ve misplaced your documents, the best course of action is to contact the insurance company directly.

Practical Steps to Uncover Your Insurance Details

Once you have an idea of where your insurance might be coming from, you can take specific steps to find out the exact details. This involves gathering documentation, contacting relevant parties, and utilizing online resources.

Identifying Your Insurance Card

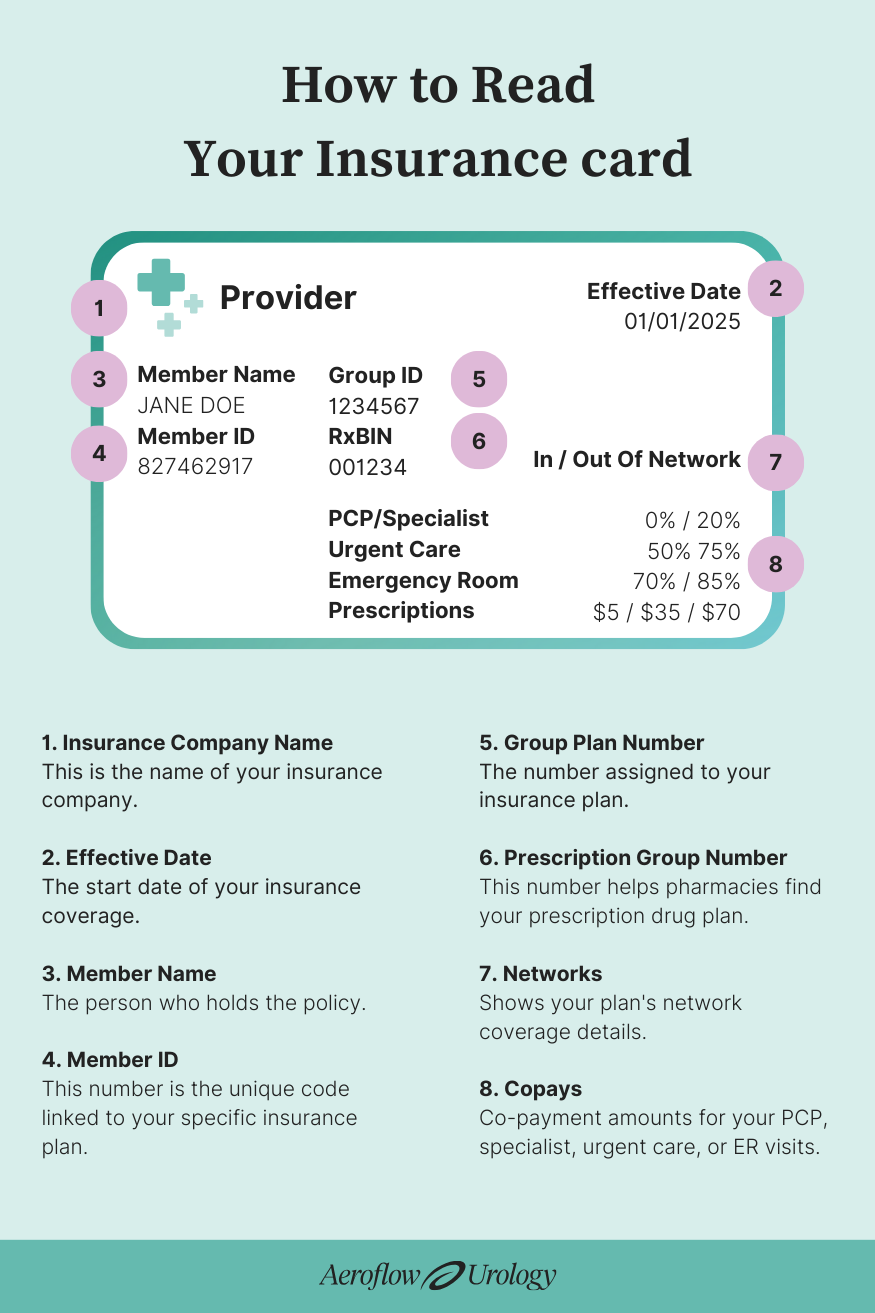

Your health insurance card is your most immediate and vital piece of information. It serves as proof of your coverage and contains all the essential details needed to identify your plan and insurer.

- Locate Your Card: Search your wallet, purse, or any place you typically keep important documents. If you’ve recently changed plans, you might have an old card that no longer applies, so ensure you’re looking for the most current one.

- Essential Information on the Card: A typical insurance card will prominently display:

- Insurance Company Name and Logo: This clearly identifies the provider.

- Member Name: Your name and potentially the names of covered dependents.

- Policy or Group Number: A unique identifier for your plan.

- Member or Subscriber ID Number: Your personal identification number with the insurer.

- Phone Numbers: A customer service number for questions about benefits, claims, and finding providers.

- Website: The insurer’s website for managing your account and finding information.

- Type of Plan (e.g., PPO, HMO, EPO): This indicates the structure of your network and how you access care.

- Rx BIN and PCN (if applicable): These are for prescription drug benefits.

If you cannot find your physical card, don’t worry. The information on it can usually be retrieved through other means.

Contacting Key Entities

Depending on how you obtain your insurance, different entities will hold the information you need. Reaching out to them directly is often the most efficient way to get clarity.

- Human Resources Department (for Employer-Sponsored Insurance): As mentioned, your employer’s HR department is the primary resource. They can provide copies of your enrollment forms, plan summaries, and contact information for the insurance carrier. Even if you’ve left the company, they can often provide information regarding your coverage up to your termination date and details about COBRA continuation.

- Insurance Carrier Directly: Once you know the name of your insurance company (from your card or other documents), you can call their customer service number. Be prepared to provide your name, date of birth, and potentially your Social Security number to verify your identity. The representative can then look up your policy details, explain your benefits, and answer specific questions about your coverage. Many insurance companies also have secure online portals where you can log in and view your plan information, claims history, and provider network.

- Healthcare Provider’s Office: If you have recently seen a doctor or visited a hospital, their billing or administrative staff can often tell you what insurance information they have on file for you. While they might not have your complete policy details, they can confirm if your insurance is active and provide the basic information they have on record. This can be a useful starting point if you’re completely unsure of your insurer.

- Social Security Administration (for Medicare): If you suspect you have Medicare, the Social Security Administration (SSA) is the agency that manages enrollment and eligibility. You can contact them by phone or visit their website (ssa.gov) to inquire about your Medicare status and coverage.

Utilizing Online Resources and Documentation

In today’s digital age, many insurance details are accessible online or through physical documentation you may have received.

- Review Past Explanation of Benefits (EOBs): An EOB is a statement sent by your insurance company after you receive medical services. It details what the medical provider billed, what the insurance company paid, and what you owe. EOBs contain crucial information about your plan, including deductibles, co-pays, and co-insurance. If you have old EOBs, they can help you identify your insurer and understand your coverage.

- Check Your Health Insurance Marketplace Account: If you purchased insurance through the ACA Marketplace, log in to your account on healthcare.gov or your state’s marketplace website. All your enrollment confirmations, plan details, and subsidy information will be stored there.

- Insurance Company Websites and Member Portals: Most insurance companies offer online portals for their members. After creating an account (or if you already have one), you can log in to view your plan documents, check coverage details, find in-network providers, and access your claims history.

- Your Bank Statements: If you have automatic payments set up for your health insurance premiums, your bank statements can be a good indicator of which company you are paying. The payee name on the statement should correspond to your insurance provider.

Understanding Key Insurance Terms

Once you have identified your insurance plan, familiarizing yourself with common insurance terminology will help you understand your coverage more effectively and utilize your benefits wisely.

Core Coverage Concepts

Understanding these fundamental terms will demystify your insurance policy and empower you to make informed decisions about your healthcare.

- Premium: This is the amount you pay to the insurance company for your health coverage, typically on a monthly basis. It’s the cost of having insurance.

- Deductible: This is the amount you pay out-of-pocket for covered healthcare services before your insurance plan starts to pay. For example, if your deductible is $2,000, you will pay the first $2,000 of your covered medical costs yourself.

- Co-payment (Co-pay): This is a fixed amount you pay for a covered healthcare service after you’ve met your deductible. For instance, you might have a $20 co-pay for a doctor’s visit.

- Co-insurance: This is your share of the costs of a covered healthcare service, calculated as a percentage (e.g., 20%) of the allowed amount for the service. You pay co-insurance after you meet your deductible. So, if your co-insurance is 20% and the allowed amount for a service is $100, you would pay $20.

- Out-of-Pocket Maximum: This is the most you will have to pay for covered services in a plan year. After you spend this amount on deductibles, co-pays, and co-insurance, your health plan pays 100% of the costs of covered benefits for the rest of the year.

- Network: This refers to the doctors, hospitals, and other healthcare providers that your insurance plan has contracted with to provide services at a discounted rate. Plans often have different cost-sharing structures for in-network versus out-of-network providers.

- In-Network vs. Out-of-Network: Using providers within your plan’s network generally results in lower costs for you. Out-of-network providers are not contracted with your plan, and you will typically pay more for their services, or they may not be covered at all.

- Pre-authorization/Prior Authorization: For certain medical services, procedures, or medications, your insurance company may require your doctor to get approval before you receive the care. Failure to obtain pre-authorization can result in the service not being covered.

Navigating Your Coverage Choices

Once you understand the basics, you can explore how your specific plan works and make the most of your benefits.

- Finding In-Network Providers: Your insurance company’s website or member portal is the best place to find a directory of in-network doctors, hospitals, and specialists. It’s crucial to verify that a provider is in-network before receiving services, as insurance networks can change.

- Understanding Prescription Drug Benefits: Your insurance card will usually indicate if you have prescription drug coverage. The details of this coverage, including which drugs are covered (the formulary) and the co-pays or co-insurance, can be found on your insurer’s website or by contacting them directly.

- Emergency Care: Most health insurance plans cover emergency services. However, it’s important to understand what constitutes an emergency and whether you are expected to use in-network facilities if possible.

- Preventive Care: Many plans cover a range of preventive services, such as annual physicals, vaccinations, and certain screenings, at no cost to you, even before you meet your deductible. Understanding your plan’s preventive care benefits can help you stay healthy and manage your healthcare costs.

By systematically exploring these avenues and understanding the essential components of your insurance, you can confidently determine what medical insurance you have and how to best utilize its benefits for your health and well-being.