The Dupont equation is a foundational tool in financial analysis, providing a structured framework to dissect a company’s profitability. It breaks down Return on Equity (ROE) into its key components, offering a deeper understanding of how effectively a company is generating returns for its shareholders. Instead of just looking at a single ROE figure, the Dupont equation reveals the underlying drivers of that performance, allowing for more informed strategic decisions and more insightful comparisons between companies. Developed by the Dupont Corporation in the 1920s, this equation has stood the test of time due to its elegance and comprehensive nature.

The Genesis and Evolution of the Dupont Equation

The Dupont equation, also known as the Dupont identity or Dupont analysis, was originally conceived by Edmund Du Pont. At its core, it’s a method to decompose Return on Equity (ROE) into several key components, enabling a more granular understanding of a company’s financial health and operational efficiency.

The Original Three-Step Dupont Analysis

The initial and most fundamental form of the Dupont equation breaks ROE into three essential components:

Net Profit Margin

This component measures how much profit a company generates for every dollar of sales. It is calculated as:

Net Profit Margin = Net Income / Revenue

A higher net profit margin indicates that a company is more efficient at converting its sales into actual profit. It can be influenced by factors such as pricing strategies, cost control measures, and operational efficiency. A company with a strong net profit margin is often considered to be well-managed and capable of fending off competitive pressures.

Asset Turnover

This ratio measures how efficiently a company uses its assets to generate sales. It is calculated as:

Asset Turnover = Revenue / Average Total Assets

A higher asset turnover ratio suggests that a company is effectively utilizing its assets to produce revenue. Companies in certain industries, like retail, tend to have higher asset turnover ratios than those in capital-intensive industries, such as manufacturing. An increasing asset turnover can signal improved operational efficiency or a more effective sales strategy.

Equity Multiplier (Financial Leverage)

This component measures the extent to which a company uses debt financing to fund its assets. It is calculated as:

Equity Multiplier = Average Total Assets / Average Shareholders’ Equity

The equity multiplier highlights the impact of financial leverage on ROE. A higher equity multiplier indicates a greater reliance on debt. While leverage can amplify returns when a company performs well, it also magnifies losses during periods of underperformance and increases financial risk. It’s crucial to analyze this component in conjunction with the others to understand the risk profile associated with the generated ROE.

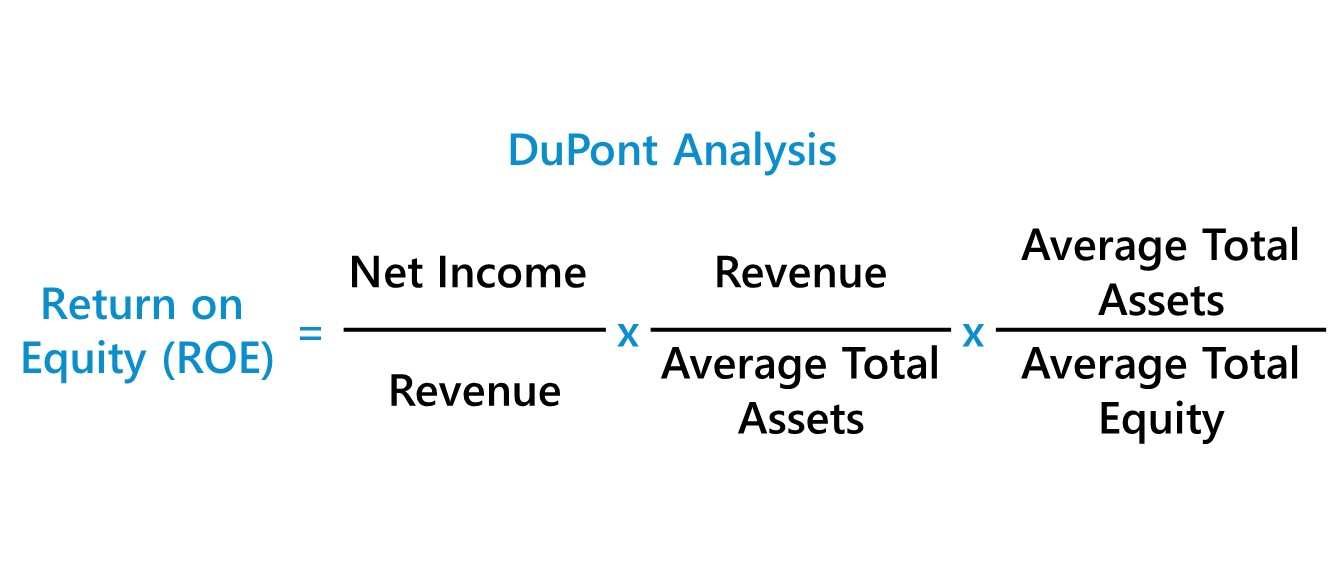

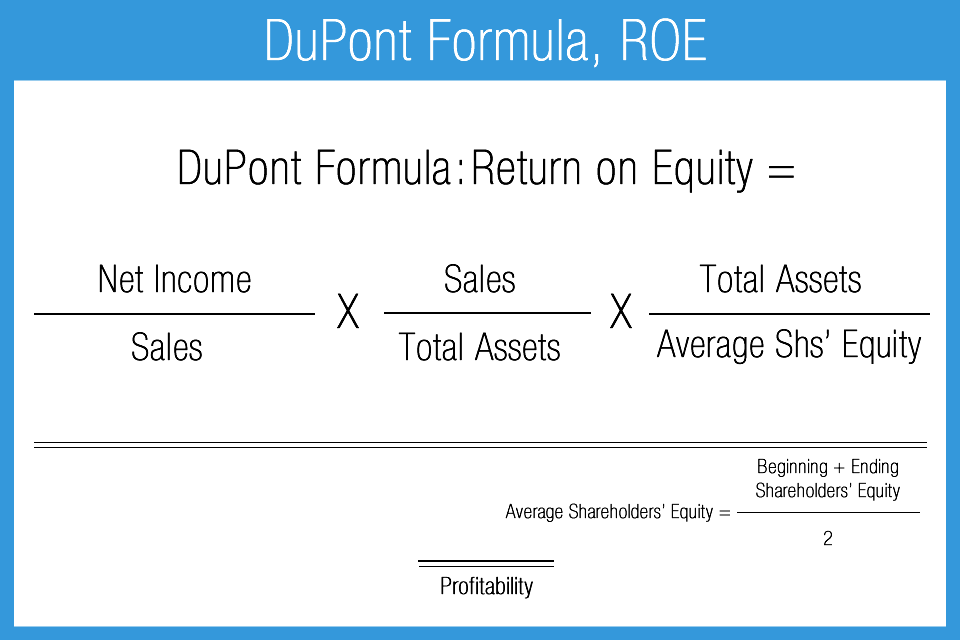

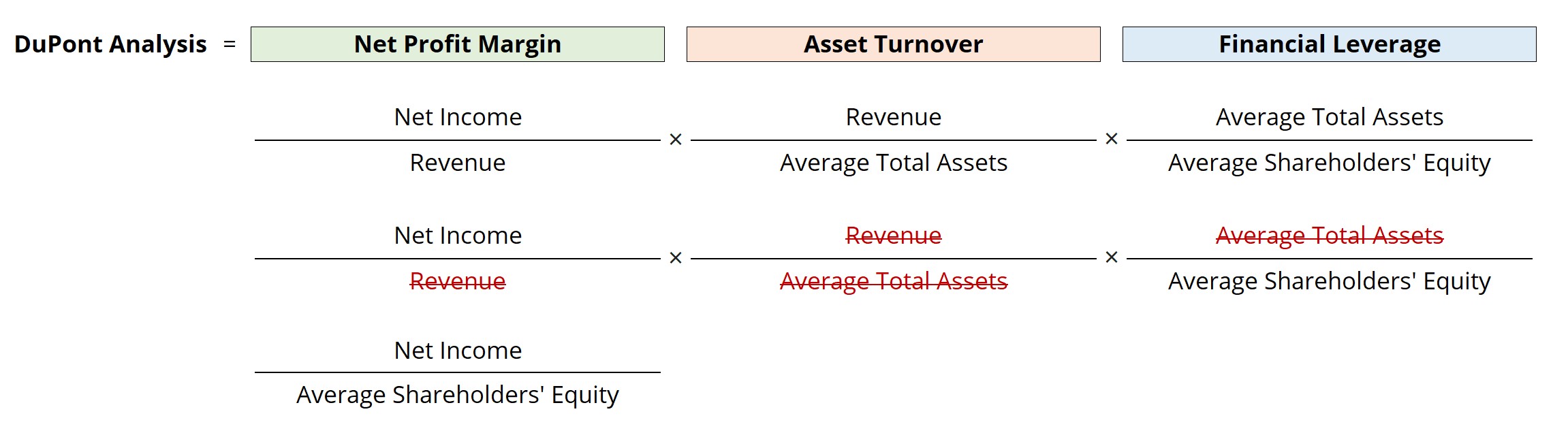

By multiplying these three components, we arrive at the Return on Equity:

ROE = Net Profit Margin × Asset Turnover × Equity Multiplier

ROE = (Net Income / Revenue) × (Revenue / Average Total Assets) × (Average Total Assets / Average Shareholders’ Equity)

This equation reveals that ROE can be improved through higher profitability, more efficient asset utilization, or increased financial leverage. The real power of the Dupont equation lies in its ability to pinpoint which of these areas a company should focus on for improvement.

The Extended Five-Step Dupont Analysis

As financial analysis evolved, the Dupont equation was further refined to provide even greater insight, particularly into the drivers of profitability. The extended five-step version breaks down the net profit margin further.

Operating Efficiency (Net Profit Margin Decomposition)

The net profit margin can be further broken down to understand the sources of operating profit. This is achieved by considering the impact of taxes and interest expense. The five-step analysis typically separates the impact of these two crucial elements.

Tax Burden

This component reflects the proportion of pretax income that a company retains after paying taxes. It is calculated as:

Tax Burden = Net Income / Earnings Before Tax (EBT)

A lower tax burden is generally favorable, indicating that a company is paying a smaller percentage of its pretax profits in taxes. This can be due to tax planning strategies, favorable tax jurisdictions, or tax credits.

Interest Burden (or Financial Expense Ratio)

This component measures the proportion of pretax income that remains after accounting for interest expense. It is calculated as:

Interest Burden = Earnings Before Tax (EBT) / Earnings Before Interest and Tax (EBIT)

A lower interest burden signifies that a company has lower interest expenses relative to its operating profits. This implies a healthier debt structure or a lower cost of debt.

The five-step Dupont equation is thus expressed as:

ROE = Tax Burden × Interest Burden × Asset Turnover × Equity Multiplier

ROE = (Net Income / EBT) × (EBT / EBIT) × (Revenue / Average Total Assets) × (Average Total Assets / Average Shareholders’ Equity)

This expanded version allows analysts to distinguish between improvements in operating performance (reflected in EBIT), the impact of financing decisions (interest burden), and tax management. For instance, if ROE is declining, the five-step analysis can reveal whether the issue stems from shrinking operating margins, an increased interest expense burden, inefficient asset use, or excessive leverage.

Applications and Significance of the Dupont Equation

The Dupont equation is not merely an academic exercise; it is a practical and invaluable tool for various stakeholders in the financial world.

For Investors

Investors use the Dupont equation to assess the quality of a company’s ROE. A high ROE driven by aggressive leverage might be seen as riskier than a comparable ROE generated through strong profit margins and efficient asset utilization. It helps investors understand whether a company is a sustainable performer or one that relies on financial engineering. By comparing the components of the Dupont equation across different companies in the same industry, investors can identify those that are outperforming their peers and understand the reasons why.

For Management

For company management, the Dupont equation serves as a vital performance management tool. It highlights specific areas that require attention and strategic focus. If the net profit margin is declining, management might investigate cost-saving measures or pricing strategies. If asset turnover is low, they might explore ways to improve inventory management, streamline production, or optimize the use of fixed assets. Understanding the leverage component is also crucial for making informed decisions about capital structure and debt management. It provides a roadmap for improving overall shareholder value.

For Creditors and Lenders

Creditors and lenders utilize the Dupont equation to assess a company’s financial health and its ability to service debt. A declining ROE, particularly if driven by a shrinking profit margin or increasing leverage, can be a red flag indicating potential financial distress. The analysis of asset turnover can also shed light on how effectively the company is generating cash flow to meet its obligations.

Industry Comparisons

The Dupont equation is particularly useful for making cross-company comparisons within the same industry. Different industries have distinct characteristics regarding profit margins, asset intensity, and typical leverage levels. By decomposing ROE, analysts can normalize these differences and identify which companies are achieving superior returns through operational excellence rather than simply industry norms. For example, a low profit margin company might still achieve a high ROE if it has a very high asset turnover, indicating an efficient business model.

Limitations and Considerations

While powerful, the Dupont equation is not without its limitations. It is a historical analysis, relying on past financial data. Future performance may differ. Furthermore, the interpretation of each component can be subjective and requires an understanding of the specific industry in which the company operates.

Industry-Specific Benchmarks

What constitutes a “good” or “bad” net profit margin or asset turnover ratio can vary significantly across industries. A high-margin luxury goods company will have different metrics than a low-margin supermarket. Therefore, comparing these components requires careful consideration of industry benchmarks.

Accounting Practices

The results of the Dupont equation can be influenced by different accounting methods and policies adopted by companies. For instance, different depreciation methods can impact asset values and thus asset turnover.

Qualitative Factors

The Dupont equation primarily focuses on quantitative financial data. It does not capture qualitative factors such as management quality, brand reputation, competitive landscape, or technological innovation, which can also significantly impact a company’s long-term success.

Dynamic Nature of Business

The business environment is constantly evolving. Market conditions, competition, and regulatory landscapes can change rapidly, affecting the components of the Dupont equation. A snapshot analysis based on past data might not always predict future outcomes accurately.

Conclusion

The Dupont equation remains an indispensable tool in the financial analyst’s toolkit. By dissecting Return on Equity into its core drivers – profitability, asset efficiency, and financial leverage – it provides a comprehensive and nuanced understanding of a company’s financial performance. Whether in its three-step or extended five-step form, the Dupont equation empowers investors, managers, and creditors to move beyond superficial financial ratios and delve into the fundamental mechanics of how a company creates value. Its enduring relevance lies in its ability to illuminate the path to sustainable profitability and superior shareholder returns, guiding strategic decisions and fostering a deeper appreciation for the intricacies of corporate finance.