Understanding the nuances of financial terminology is crucial, especially when it comes to investments, loans, and savings accounts. Two terms that often cause confusion are APY (Annual Percentage Yield) and APR (Annual Percentage Rate). While they both represent interest rates, they reflect different aspects of how that interest accrues and impacts your financial outcomes. This article will delve into the core differences between APY and APR, explaining what each signifies and how to interpret them for better financial decision-making.

Understanding the Basics: Interest Rate Fundamentals

At their core, both APY and APR are ways to express the cost of borrowing or the return on lending money over a year. However, the methods they use to calculate and present this information lead to significant distinctions.

The Foundation: What is Interest?

Interest is essentially the cost of borrowing money or the reward for lending it. When you borrow money, you pay interest to the lender. Conversely, when you lend money (e.g., by depositing it into a savings account or investing in a bond), you earn interest from the borrower. The rate at which this interest is calculated and applied is fundamental to understanding financial products.

Annualizing Rates: The Yearly Perspective

Both APY and APR are expressed as annual rates. This standardization allows for easy comparison across different financial products that might have varying compounding frequencies or fee structures. However, this annualization is where their paths begin to diverge. The “annual” aspect is key because it sets the benchmark for comparison, regardless of how often the interest is calculated within that year.

Compounding: The Power of Growth

A critical factor influencing the difference between APY and APR is compounding. Compounding occurs when the interest earned on an investment or loan is added to the principal amount. This new, larger principal then earns interest in subsequent periods. The more frequently interest compounds, the faster your money grows (or the more expensive your loan becomes). This concept is central to understanding why APY and APR can present such different figures.

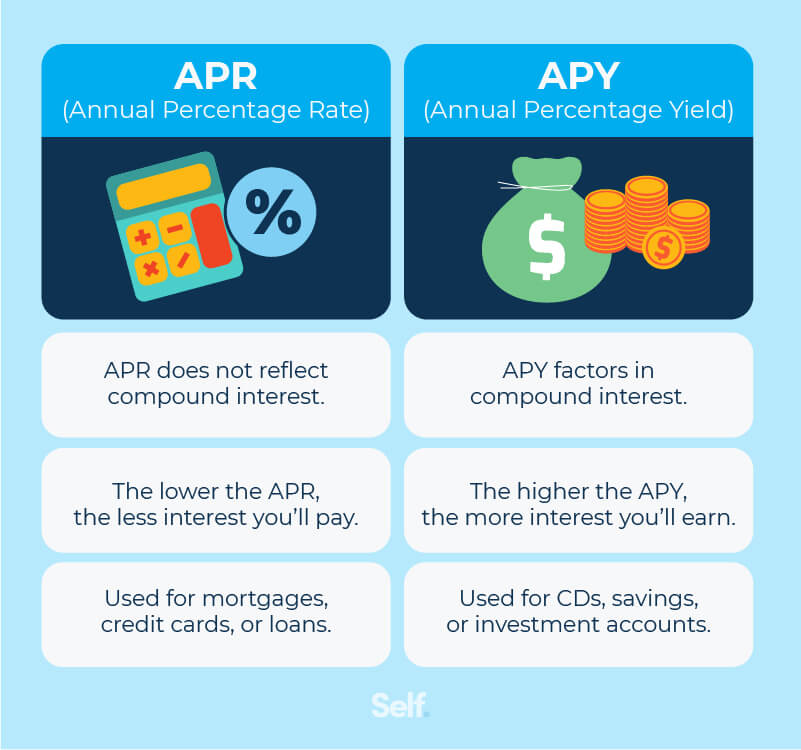

APR: The Annual Percentage Rate Explained

APR provides a broader picture of the cost of borrowing or the return on an investment, taking into account not just the simple interest rate but also any associated fees. It is designed to give a more realistic representation of the total financial commitment or benefit.

The Core Calculation: Simple Interest and Fees

At its most basic level, APR reflects the annual cost of a loan, including the interest rate and any other mandatory fees charged by the lender. For loans, this typically includes origination fees, processing fees, and other administrative charges that are a direct cost of obtaining the loan. When viewed as an investment, APR might represent the stated interest rate plus any upfront fees associated with the investment.

Fees Included in APR Calculations

The specific fees included in an APR calculation can vary depending on the type of financial product. For mortgages, this might include points, mortgage insurance premiums, and appraisal fees. For credit cards, it can encompass annual fees, late payment fees (though these are often handled separately), and balance transfer fees. Understanding which fees are incorporated is vital for a true cost assessment. It’s important to note that some fees, like late payment penalties, are often not included in the standard APR calculation but are separate charges.

APR on Loans: A True Cost Indicator

When you take out a loan, the APR is often the most important figure to consider because it represents the total cost of borrowing over the life of the loan, expressed as an annual rate. A loan with a lower APR will generally be cheaper than a loan with a higher APR, assuming all other factors are equal. This is because the APR attempts to quantify all the upfront and recurring costs associated with the loan into a single, comparable percentage.

APR on Credit Cards: Understanding the Borrower’s Perspective

For credit cards, APR is the rate at which interest accrues on your outstanding balance. This rate is typically applied to purchases, balance transfers, and cash advances, though these may have different APRs. Crucially, the APR on a credit card is usually a variable rate, meaning it can change based on market conditions or the issuer’s discretion. Understanding the purchase APR, balance transfer APR, and cash advance APR is essential for managing credit card debt effectively.

APR vs. Simple Interest: A Distinctive Comparison

It’s important to distinguish APR from simple interest. Simple interest is calculated only on the principal amount. APR, on the other hand, aims to be a more comprehensive measure by incorporating fees. However, APR does not always account for compounding within the year. For loans, the APR often represents the sum of the interest rate and fees, divided by the loan principal, and then annualized. This means that while it captures fees, it might not fully reflect the impact of interest compounding throughout the loan term.

APY: The Annual Percentage Yield Explained

APY, on the other hand, focuses on the effective rate of return on an investment, taking into account the impact of compounding. It represents how much an investment will actually earn in a year if all the interest earned is reinvested.

The Magic of Compounding: APY’s Core Principle

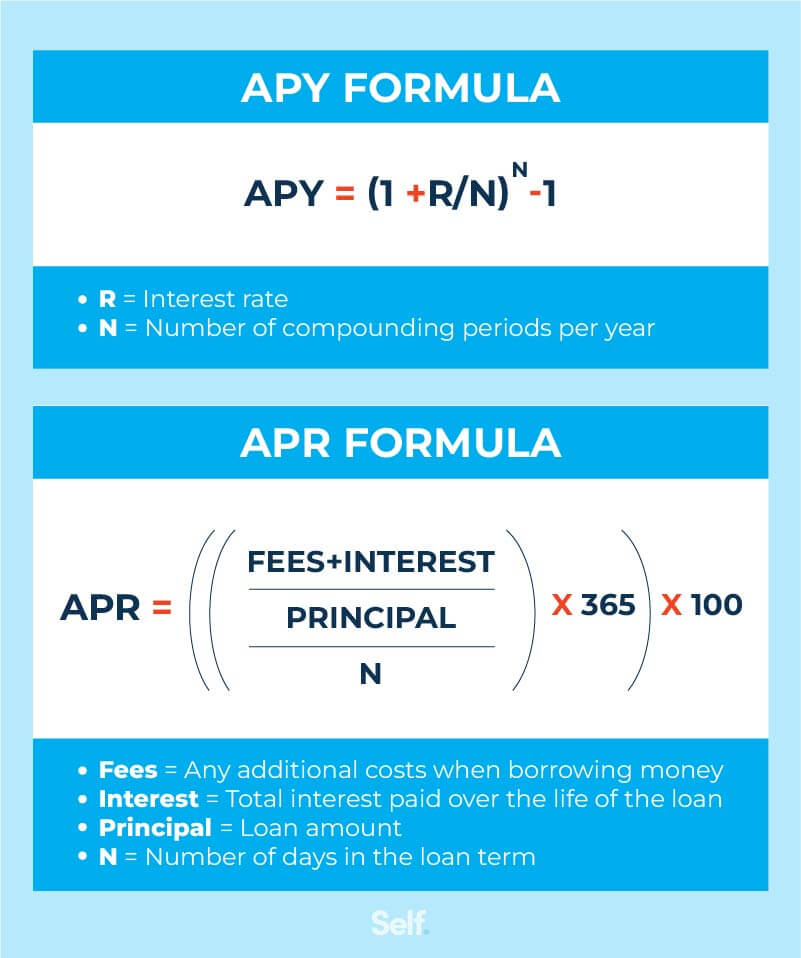

The key differentiator for APY is its inclusion of the effect of compounding. When interest is compounded more frequently than annually, the APY will be higher than the stated interest rate (which is often the APR when referring to savings accounts or certificates of deposit). This is because the interest earned in each compounding period is added to the principal, and then that larger principal earns interest in the next period.

How Compounding Frequency Affects APY

The more frequently interest is compounded (e.g., daily, monthly, quarterly), the higher the APY will be compared to the nominal interest rate. For instance, an account with a 5% nominal interest rate compounded daily will have a higher APY than an account with a 5% nominal interest rate compounded annually. This is because the daily compounding allows for more frequent “reinvestment” of earnings, leading to exponential growth over the year.

APY on Savings Accounts and Certificates of Deposit (CDs)

APY is most commonly used to describe the return on savings accounts, money market accounts, and certificates of deposit (CDs). When comparing different savings products, the APY is the most relevant metric to consider because it reflects the actual yield you can expect to earn after the effects of compounding are factored in. A higher APY means your money will grow faster.

APY vs. Interest Rate: The True Yield

While a savings account might advertise a specific interest rate (often equivalent to the APR for such products), the APY reveals the true yield you will receive after accounting for compounding. For example, if a savings account offers a 4% interest rate compounded monthly, the APY will be slightly higher than 4%. This difference, while seemingly small, can add up significantly over time, especially with larger balances.

APY for Investors: Maximizing Returns

For investors, understanding APY is crucial for evaluating the performance of interest-bearing investments. It provides a clear, standardized way to compare the potential returns of different investment vehicles, such as bonds, dividend stocks (when considering the dividend yield and its reinvestment), and various savings instruments.

Key Differences Summarized: APR vs. APY

The fundamental distinction between APR and APY lies in what they measure and the factors they include. While both are expressed as annual rates, their scope and purpose differ significantly.

APR: The Cost of Borrowing and Fees

APR is primarily concerned with the total cost of borrowing or the stated rate of return on an investment, including any associated fees. It is a more comprehensive measure of the upfront and ongoing expenses related to a loan or financial product. Think of APR as the “sticker price” plus mandatory add-ons.

APY: The Effective Return with Compounding

APY, on the other hand, focuses on the actual return an investment will yield over a year, taking into account the power of compounding. It shows how much your money will grow if all earned interest is reinvested. APY is the “actual growth” after accounting for reinvested earnings.

When to Use Which: Practical Application

In practice, you’ll encounter APR and APY in different contexts:

- Loans (Mortgages, Auto Loans, Personal Loans, Credit Cards): APR is the critical metric to compare the cost of borrowing. A lower APR generally means a cheaper loan.

- Savings Accounts, CDs, Money Market Accounts: APY is the metric to compare returns. A higher APY means your money will grow faster.

- Investments: APY can be used to compare the effective yield of various interest-bearing investments, especially those with compounding features.

The Impact on Your Wallet: Why It Matters

Understanding the difference between APY and APR can have a substantial impact on your financial well-being.

- For Borrowers: A lower APR on a loan translates to less money paid in interest and fees over time. It’s essential to shop around and compare APRs from different lenders to secure the best possible terms.

- For Savers and Investors: A higher APY on savings accounts or investments means your money is working harder for you, leading to greater wealth accumulation over the long term. Choosing accounts or investments with higher APYs can significantly boost your returns.

By paying close attention to these seemingly subtle differences, you can make more informed decisions about borrowing, saving, and investing, ultimately leading to better financial outcomes.

Navigating Financial Products: A Comparative Approach

To solidify your understanding, let’s explore how APR and APY function in real-world financial scenarios and how to use them effectively for comparison.

Scenario 1: Comparing Loans

Imagine you are looking for a personal loan and find two options:

- Loan A: Offers a 7% interest rate with a $500 origination fee on a $10,000 loan.

- Loan B: Offers a 7.5% interest rate with a $100 origination fee on a $10,000 loan.

If you only looked at the interest rate, Loan A might seem better. However, calculating the APR provides a clearer picture of the total cost. While the exact APR calculation can be complex and often provided by the lender, the concept is that the fees are factored into the annualized rate. In this simplified example, Loan A has a higher upfront fee, which would likely result in a higher APR than Loan B, despite the lower stated interest rate.

Scenario 2: Comparing Savings Accounts

Consider two savings accounts:

- Account X: Offers a 2.00% interest rate compounded annually.

- Account Y: Offers a 1.98% interest rate compounded daily.

In this case, Account X has a slightly higher nominal interest rate. However, Account Y, with daily compounding, will likely have a higher APY.

- For Account X, the APY is 2.00%.

- For Account Y, the APY would be calculated as: $(1 + frac{0.0198}{365})^{365} – 1 approx 0.0200198$, or approximately 2.002%.

While the difference is small in this example, it demonstrates that daily compounding in Account Y yields a slightly better return than annual compounding in Account X, even with a lower stated interest rate. This highlights the importance of APY for comparing savings products.

The Importance of Full Disclosure

Financial institutions are required to disclose both APR and APY for their products. It is imperative to read all disclosures carefully and ask questions if anything is unclear. The Truth in Lending Act (TILA) in the United States mandates the disclosure of APR for most consumer loans, providing consumers with a standardized way to compare credit offers. Similarly, regulations often require financial institutions to display the APY for deposit accounts.

Beyond the Numbers: Other Factors to Consider

While APR and APY are critical, they are not the only factors to consider:

- Loan Terms: Loan duration, repayment schedules, and prepayment penalties can significantly affect the total cost of a loan, even with a favorable APR.

- Fees: Be aware of all potential fees, including hidden fees, overdraft fees, ATM fees, and transaction fees, which might not be fully captured in either APR or APY.

- Risk: For investments, the potential for loss of principal is a major consideration that APY alone does not address.

- Convenience and Accessibility: For savings accounts, factors like ease of access to funds, minimum balance requirements, and online banking features can also influence your choice.

By understanding and utilizing both APR and APY, you equip yourself with powerful tools to navigate the complex world of finance, making informed decisions that align with your financial goals.