This question, seemingly rooted in administrative minutiae, holds significant weight within the realm of technology and innovation, particularly concerning the evolving landscape of freelance work and the traditional employee model. While the terms “1099” and “W2” might initially appear dry, they represent fundamental distinctions in how individuals are compensated and their legal standing within an organization, directly impacting how tech talent engages with companies, how projects are managed, and ultimately, the pace and nature of innovation itself. Understanding these differences is crucial for both the individuals contributing their skills and the organizations seeking to leverage them.

The Foundational Distinction: Employee vs. Independent Contractor

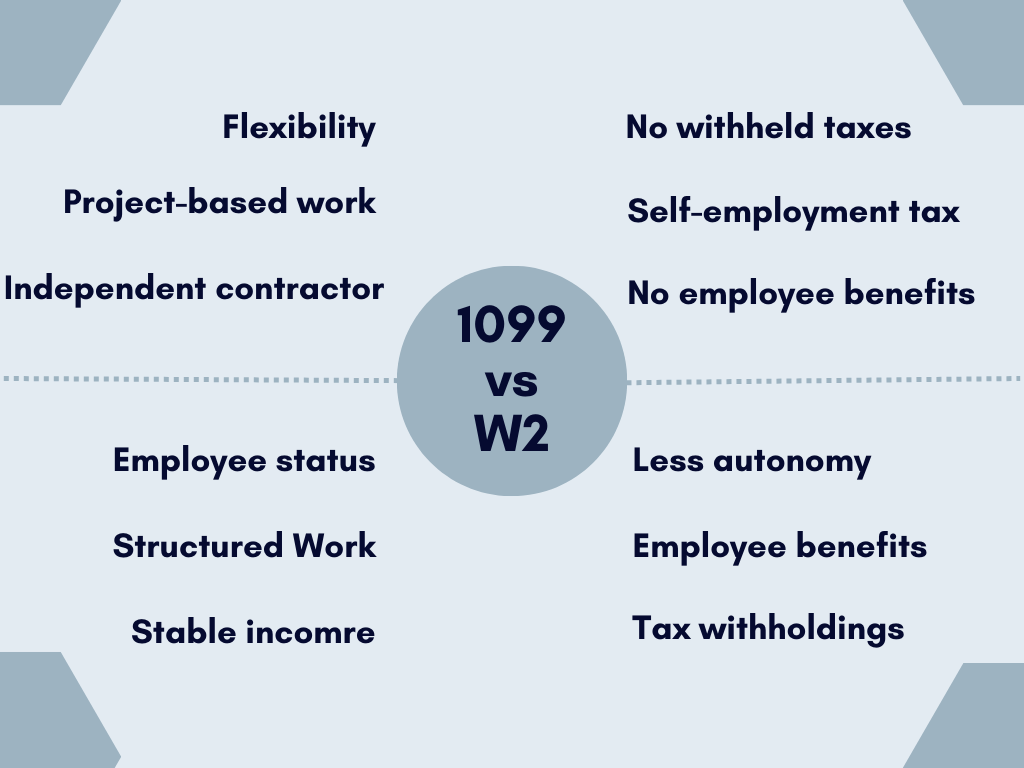

At its core, the difference between a W2 employee and a 1099 independent contractor boils down to their relationship with the hiring entity and the resultant tax and legal implications. This distinction is not merely semantic; it dictates benefits, liabilities, and the operational framework within which technological advancements are pursued.

W2 Employees: The Traditional Path of Integration and Benefits

A W2 employee is someone who is hired directly by a company and is considered an integral part of that organization. This employment classification comes with a specific set of responsibilities and benefits, both for the employee and the employer.

Rights, Responsibilities, and Employer Oversight

When an individual is classified as a W2 employee, they are subject to the direct control and supervision of their employer. This means the employer dictates their work hours, the tools they use, and often, the specific methods they employ to complete their tasks. The employer is also responsible for withholding income taxes (federal, state, and local), Social Security, and Medicare taxes from the employee’s paycheck. This withholding is then remitted to the government on behalf of the employee.

Furthermore, W2 employees are typically eligible for a range of benefits provided by the employer. These can include health insurance, dental insurance, vision coverage, paid time off (vacation, sick leave, holidays), retirement plans (like 401(k)s), life insurance, and disability insurance. These benefits are a significant component of the overall compensation package and contribute to the employee’s financial security and well-being.

Tax Implications and Employer Contributions

From a tax perspective, the employer bears a significant portion of the tax burden. They are responsible for paying half of the Social Security and Medicare taxes (known as FICA taxes) for each W2 employee. Additionally, employers must pay unemployment taxes, which fund unemployment benefits for former employees. This employer contribution is a substantial cost for businesses, but it also signifies a commitment to the employee’s long-term stability and economic security.

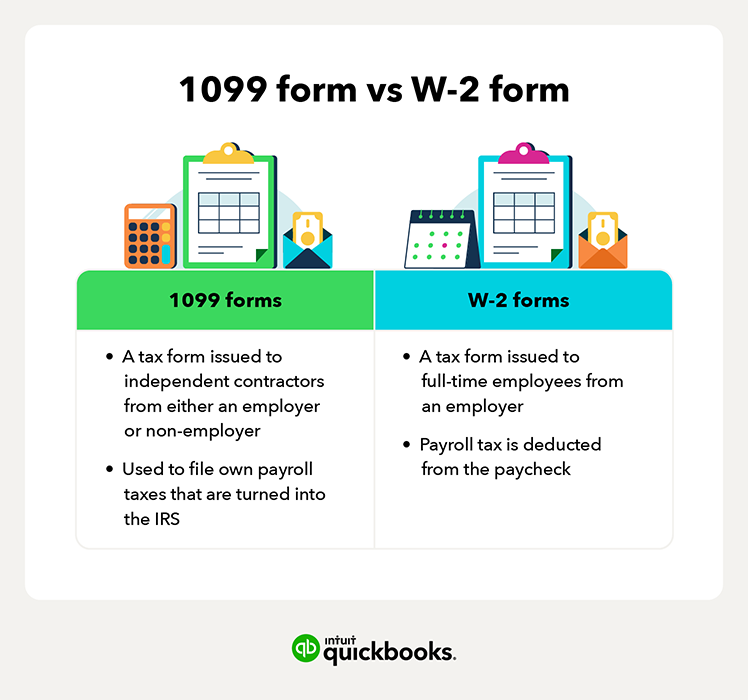

For the W2 employee, tax filing is generally simpler. They receive a W2 form at the end of the year from their employer, which details their total earnings and the taxes already withheld. They then use this form to file their annual income tax returns.

1099 Independent Contractors: The Autonomous Contributors

In contrast, a 1099 independent contractor is not an employee of the hiring entity. Instead, they are considered self-employed individuals or business entities who provide services to a client or company. This model is increasingly prevalent in the tech industry, enabling companies to access specialized skills and flexibility.

Autonomy, Control, and Project-Based Work

The defining characteristic of a 1099 contractor is their autonomy. They typically have control over how, when, and where they perform their work. While they are engaged to deliver specific results or complete particular projects, the hiring entity generally does not dictate the minute details of their process. This freedom allows contractors to manage their own schedules, utilize their preferred tools and software, and often work on multiple projects for different clients simultaneously.

This autonomy is a significant draw for many tech professionals, offering flexibility and the opportunity to diversify their experience and income streams. It’s particularly relevant in rapidly evolving fields like AI development, cybersecurity, and specialized software engineering, where niche expertise is in high demand.

Tax Responsibilities and Self-Employment

The tax responsibilities for a 1099 contractor are fundamentally different. They are responsible for paying both the employee and employer portions of Social Security and Medicare taxes. This is known as self-employment tax, which is currently 15.3% of their net earnings from self-employment. They are also responsible for paying their own federal, state, and local income taxes.

Contractors typically make estimated tax payments quarterly throughout the year to avoid penalties for underpayment. At the end of the year, the hiring entity sends the contractor a Form 1099-NEC (Nonemployee Compensation), detailing the total amount paid to them. The contractor then uses this information, along with their own business expenses, to file their tax returns.

Navigating the Tech Landscape: Implications for Innovation and Talent Acquisition

The prevalence of both W2 employees and 1099 contractors profoundly shapes the operational dynamics and innovation strategies within the tech sector. Companies must carefully consider which model best suits their needs for specific roles and projects.

W2 Model in Tech: Building Core Teams and Long-Term Development

For roles requiring deep integration into a company’s culture, long-term strategic development, and proprietary knowledge acquisition, the W2 model is often preferred. Companies building foundational technology, developing core intellectual property, or requiring highly coordinated team efforts often lean on W2 employees.

Fostering Company Culture and Knowledge Retention

W2 employees are more likely to be invested in the long-term success and culture of a company. Their engagement extends beyond individual projects to encompass the overall mission and vision. This fosters a sense of loyalty and commitment, which is invaluable for knowledge retention and the development of institutional expertise. When a company is working on complex, multi-year projects, having a stable core of W2 employees ensures that critical knowledge and skills remain within the organization.

Access to Benefits and Stability for Talent

The comprehensive benefits packages offered to W2 employees provide a strong incentive for top talent seeking stability and long-term career prospects. Health insurance, retirement plans, and paid time off are significant factors for individuals and families, making W2 positions attractive, especially for those prioritizing work-life balance and a predictable income. This stability can be crucial for attracting and retaining engineers, researchers, and other professionals who require consistent support and resources to focus on groundbreaking work.

1099 Model in Tech: Agility, Specialized Expertise, and Project-Based Solutions

The 1099 model has become indispensable for the tech industry’s inherent need for agility, rapid prototyping, and access to highly specialized skills that may not be required on a permanent basis.

Sourcing Niche Skills and Rapid Project Deployment

The tech world is characterized by rapid advancements and evolving needs. Companies often require highly specialized expertise for short-to-medium term projects, such as implementing a new AI algorithm, developing a blockchain solution, or performing a critical cybersecurity audit. Engaging 1099 contractors allows companies to quickly access these niche skills without the long-term commitment and overhead associated with hiring a full-time employee. This agility is crucial for staying competitive and delivering innovative solutions quickly.

Cost-Effectiveness and Flexibility in Resource Allocation

From a financial perspective, the 1099 model can be more cost-effective for project-specific needs. Companies avoid paying for benefits, employer-side taxes, and other employment-related expenses associated with W2 employees. This allows for more flexible resource allocation, enabling companies to scale their workforce up or down based on project demands. This is particularly advantageous for startups and smaller tech firms that need to manage their budgets carefully while still accessing world-class talent.

The Nuances of Classification: Avoiding Misclassification and Its Consequences

The distinction between W2 and 1099 is not always clear-cut, and misclassification can lead to significant legal and financial repercussions for both the hiring entity and the individual.

Determining the True Nature of the Relationship: Key Factors

Regulatory bodies, such as the IRS and state labor departments, utilize specific tests to determine whether a worker is an employee or an independent contractor. These tests generally focus on the degree of control the hiring entity has over the worker.

The Control Test: Behavioral, Financial, and Type of Relationship

The behavioral control aspect examines whether the company dictates when, where, and how the work is done. For a W2 employee, this control is typically high. For a 1099 contractor, it’s usually low, with the contractor having significant discretion.

Financial control considers aspects like whether the worker has unreimbursed business expenses, whether they invest in their own equipment, whether they offer their services to the general public, and how they are paid (e.g., by the hour or by the project). Independent contractors often bear more financial risk and invest in their own resources.

The type of relationship looks at whether the parties have a written contract defining their relationship, whether benefits are provided, the permanency of the relationship, and whether the services performed are a key aspect of the hiring entity’s business.

Consequences of Misclassification: Legal and Financial Penalties

If a company misclassifies a worker as an independent contractor when they should have been classified as an employee, they can face substantial penalties. These can include back taxes (including Social Security and Medicare taxes), interest on those taxes, fines, and liability for unpaid overtime, unemployment insurance, and workers’ compensation.

For the misclassified worker, the consequences can include a loss of benefits they would have received as an employee, such as health insurance, retirement contributions, and paid time off. They may also be responsible for paying additional taxes if they haven’t been properly accounting for their self-employment income.

Conclusion: Strategic Choices in the Dynamic Tech Ecosystem

The choice between engaging a W2 employee or a 1099 independent contractor is a strategic decision with far-reaching implications for any technology company. It’s a decision that balances the need for core team stability and cultural alignment with the demand for agility, specialized expertise, and cost-effectiveness.

Embracing a Hybrid Model for Optimal Talent Utilization

In the dynamic tech landscape, many companies thrive by adopting a hybrid model. This involves building a strong core of W2 employees who embody the company’s culture, drive long-term innovation, and retain critical knowledge, while strategically leveraging 1099 contractors for specialized projects, burst capacity, and to access cutting-edge skills. This balanced approach allows organizations to remain nimble, innovative, and competitive, ensuring they can effectively harness the diverse talents required to navigate the ever-evolving technological frontier. Understanding the fundamental differences between the W2 and 1099 classifications is not just an administrative necessity; it’s a critical component of effective talent management and a key driver of success in the modern technology ecosystem.