The healthcare landscape is complex, and understanding its financial underpinnings is crucial for individuals navigating their financial futures. Among the various taxes that contribute to public services, the Additional Medicare Tax (AMT) often raises questions. This specific tax, introduced to bolster funding for the Medicare program, plays a significant role in the nation’s healthcare system. While its name suggests a direct link to Medicare, its implications extend to a broader understanding of payroll taxes and their impact on high-income earners.

Understanding the Foundation: Medicare and Its Funding

Medicare is a federal health insurance program primarily for individuals aged 65 and older, younger people with disabilities, and people with End-Stage Renal Disease (ESRD). It’s a vital safety net, providing access to essential medical services and treatments for millions of Americans. The program is funded through a combination of payroll taxes, premiums, and general federal revenue. Understanding how Medicare is financed is the first step in comprehending the purpose and impact of the Additional Medicare Tax.

The Medicare Payroll Tax: A Core Component

The bedrock of Medicare funding from earned income is the Medicare payroll tax. This tax is collected from both employees and employers through the Federal Insurance Contributions Act (FICA) and the Self-Employment Contributions Act (SECA). For most wage earners, the Medicare tax rate is 1.45% of their gross wages, with an equal 1.45% contribution from their employer, totaling 2.9%. This means that for every dollar earned, 2.9 cents are directed towards Medicare. Self-employed individuals pay both the employee and employer portions, which amounts to 2.9% of their net earnings from self-employment. There is no income limit on the amount of earnings subject to this standard Medicare tax.

Beyond the Standard: The Need for Additional Funding

As the population ages and healthcare costs continue to rise, the demand on the Medicare program has steadily increased. To ensure the long-term solvency and adequacy of Medicare funding, legislative measures have been implemented to generate additional revenue. The Additional Medicare Tax is one such measure, designed to contribute further to the program’s financial stability by targeting higher earners. It’s a mechanism that acknowledges the differing capacities of individuals to contribute to shared societal resources, particularly those related to essential services like healthcare.

The Mechanics of the Additional Medicare Tax

The Additional Medicare Tax is not a separate tax in the sense of a new tax form or a distinct filing requirement. Instead, it’s an increase in the existing Medicare tax rate for certain high-income individuals. Its application is specific and has clear thresholds that determine who is subject to it. Understanding these thresholds and how they are calculated is paramount for accurate tax planning and compliance.

Defining High-Income Earners: Thresholds and Applicability

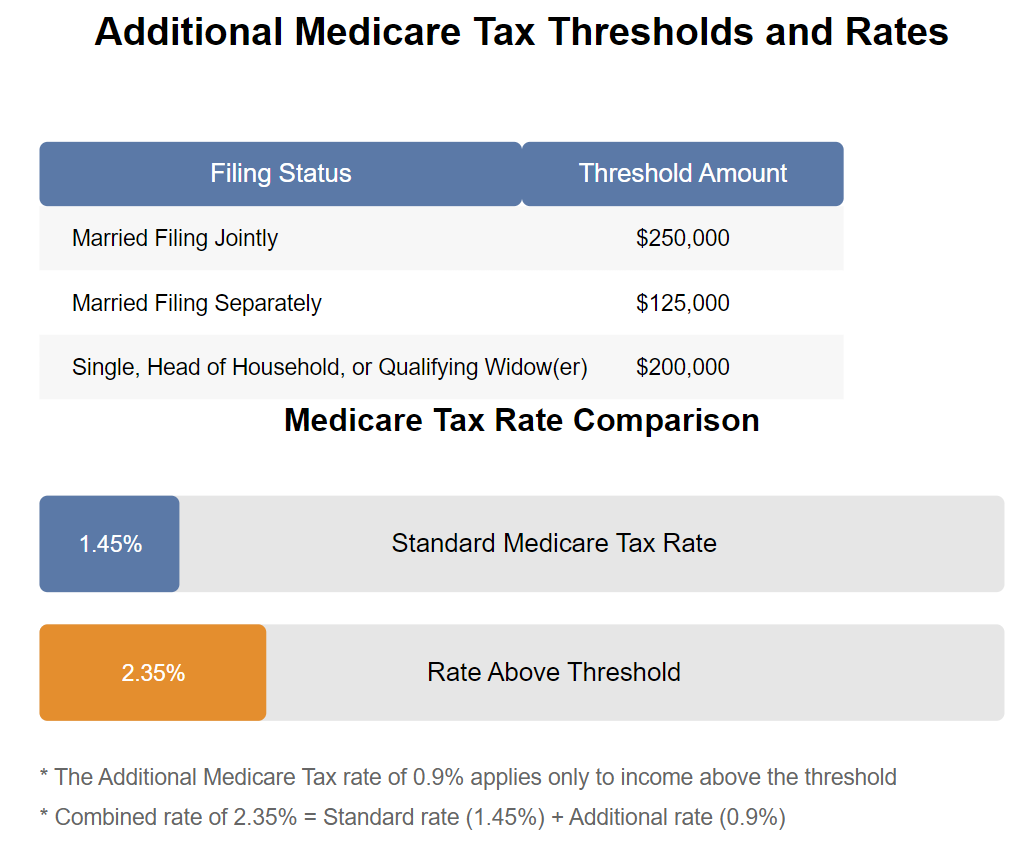

The Additional Medicare Tax applies to individuals whose annual earned income exceeds certain thresholds. These thresholds are set by the IRS and are adjusted periodically. For the tax year 2023, the thresholds for individuals are:

- Unmarried individuals: $200,000

- Married individuals filing jointly: $250,000

- Married individuals filing separately: $125,000

It’s crucial to note that these thresholds apply to earned income, which typically includes wages, salaries, tips, and net earnings from self-employment. Investment income, such as dividends and capital gains, is generally not subject to the Additional Medicare Tax. However, for self-employed individuals, their net earnings from self-employment are considered earned income.

The Rate Increase: A Deeper Dive

Once an individual’s earned income surpasses the applicable threshold, an additional 0.9% tax is levied on the income exceeding that threshold. This 0.9% is in addition to the standard 1.45% Medicare tax. Therefore, for individuals earning above the thresholds, the total Medicare tax rate on that excess income becomes 2.35% (1.45% + 0.9%).

For example, if an unmarried individual earns $250,000 in a year, the first $200,000 is subject to the standard 1.45% Medicare tax. The remaining $50,000 ($250,000 – $200,000) is subject to the Additional Medicare Tax, bringing the total Medicare tax rate on that $50,000 to 2.35%. The calculation for the additional tax would be $50,000 * 0.009 = $450.

Self-Employment Considerations: Navigating SECA

For self-employed individuals, the calculation of the Additional Medicare Tax is slightly more nuanced due to the self-employment tax. The self-employment tax rate is 15.3% on net earnings from self-employment, which includes Social Security tax (12.4% up to an annual limit) and Medicare tax (2.9% with no limit). A deduction for one-half of the self-employment tax is allowed when calculating adjusted gross income.

When a self-employed individual’s net earnings from self-employment exceed the applicable thresholds, the additional 0.9% Medicare tax applies to the portion of their net earnings from self-employment that exceeds those thresholds. It’s important to remember that the 0.9% is on top of the 2.9% Medicare portion of the self-employment tax. So, for income above the threshold, the total Medicare tax rate for a self-employed individual becomes 3.8% (2.9% + 0.9%).

Broader Implications and Tax Planning

The Additional Medicare Tax, while specific in its application, has broader implications for financial planning, particularly for individuals approaching or exceeding the income thresholds. Understanding its existence and mechanics allows for more informed decision-making regarding income streams, tax strategies, and long-term financial goals.

Impact on High-Income Earners and Their Financial Strategies

The Additional Medicare Tax directly impacts the take-home pay of high-income earners. This can influence their decisions about income deferral, investment strategies, and even business structures. For instance, an individual anticipating exceeding the threshold might consider deferring bonuses or other forms of compensation to a future year when their income might be lower. They might also explore tax-advantaged investment vehicles that can reduce their overall taxable income. The additional tax can also be a factor in considering if the benefits of certain business structures outweigh the increased tax burden.

Interaction with Other Tax Provisions

It’s important to understand that the Additional Medicare Tax operates independently of other tax provisions, such as the Alternative Minimum Tax (AMT) for individuals. While both involve complex calculations, they address different tax bases and have different purposes. The Additional Medicare Tax is solely focused on increasing Medicare funding based on earned income thresholds. It’s crucial for taxpayers to consult with tax professionals to ensure they are accurately calculating and reporting all applicable taxes and to leverage any available tax planning opportunities.

The Role in Medicare’s Financial Sustainability

The Additional Medicare Tax plays a crucial role in the ongoing financial sustainability of the Medicare program. As healthcare demands evolve and the population ages, ensuring adequate funding is paramount. This tax, by targeting those with a greater capacity to contribute, helps to bridge potential funding gaps and supports the program’s ability to provide essential healthcare services to millions. It’s a component of a broader system designed to balance individual financial responsibility with collective societal well-being.

Conclusion: Navigating the Medicare Tax Landscape

The Additional Medicare Tax is a specific, yet significant, aspect of the U.S. tax system, directly contributing to the vital Medicare program. It functions as an increase on the standard Medicare payroll tax for individuals whose earned income surpasses defined thresholds. Understanding these thresholds, the additional rate, and its implications for earned income and self-employment is essential for accurate tax compliance and effective financial planning. By staying informed about such tax provisions, individuals can better manage their financial obligations and contribute to the continued strength of essential public services like Medicare.