Return on Equity (ROE) is a critical financial metric that measures a company’s profitability in relation to its shareholders’ equity. It essentially tells investors how effectively a company is using the money invested by its shareholders to generate profits. In the realm of finance, understanding ROE is paramount for evaluating a company’s performance, assessing its value, and making informed investment decisions. This metric serves as a vital indicator of management’s efficiency in deploying capital and generating returns for its owners.

Understanding the Core Components of ROE

At its heart, ROE is a ratio derived from the income statement and the balance sheet. It requires a clear understanding of its constituent parts: net income and shareholders’ equity. Without a firm grasp of these elements, the true meaning and implications of ROE can be lost.

Net Income: The Bottom Line of Profitability

Net income, often referred to as the “bottom line,” represents a company’s total earnings after all expenses, including taxes and interest, have been deducted. It is the profit that is available to be distributed to shareholders or reinvested back into the business. For ROE calculation, the most recent period’s net income is typically used, providing a snapshot of the company’s earning power over a specific timeframe.

Factors Influencing Net Income

Several factors contribute to a company’s net income. These include:

- Revenue: The total amount of money generated from the sale of goods or services. Higher revenue, all else being equal, generally leads to higher net income.

- Cost of Goods Sold (COGS): The direct costs attributable to the production or purchase of the goods sold by a company. Reducing COGS can improve profitability.

- Operating Expenses: Costs incurred in the normal course of business, such as salaries, rent, marketing, and research and development. Efficient management of these expenses is crucial.

- Interest Expenses: The cost of borrowing money. Companies with significant debt will have higher interest expenses, which reduce net income.

- Taxes: Corporate income taxes levied by governments. Tax rates can significantly impact the final net income.

- Depreciation and Amortization: Non-cash expenses that reflect the wear and tear of assets over time. While not cash outflows, they reduce taxable income.

The quality and sustainability of net income are vital considerations when analyzing ROE. A company with consistently growing and high-quality net income will generally present a more attractive ROE than one with volatile or artificially inflated earnings.

Shareholders’ Equity: The Stakeholders’ Investment

Shareholders’ equity, also known as book value, represents the owners’ stake in a company. It is calculated as total assets minus total liabilities. This figure reflects the amount of capital that has been contributed by shareholders (through stock purchases) and retained earnings that have been reinvested into the business over time.

Components of Shareholders’ Equity

Shareholders’ equity is comprised of several key components:

- Common Stock: The par value of the shares issued to common stockholders.

- Preferred Stock: The par value of preferred shares issued, which typically have different dividend rights and liquidation preferences than common stock.

- Additional Paid-in Capital: The amount of capital shareholders paid for stock above its par value.

- Retained Earnings: The accumulated profits of a company that have not been distributed as dividends to shareholders. This is a significant driver of equity growth and is directly linked to profitability.

- Treasury Stock: Shares of the company’s own stock that it has repurchased from the open market. This reduces total shareholders’ equity.

The choice of whether to use average shareholders’ equity or year-end shareholders’ equity in the ROE calculation can also influence the result. Using average equity, calculated as (Beginning Equity + Ending Equity) / 2, is often preferred as it smooths out potential distortions caused by significant changes in equity during the period, such as stock buybacks or new equity issuances.

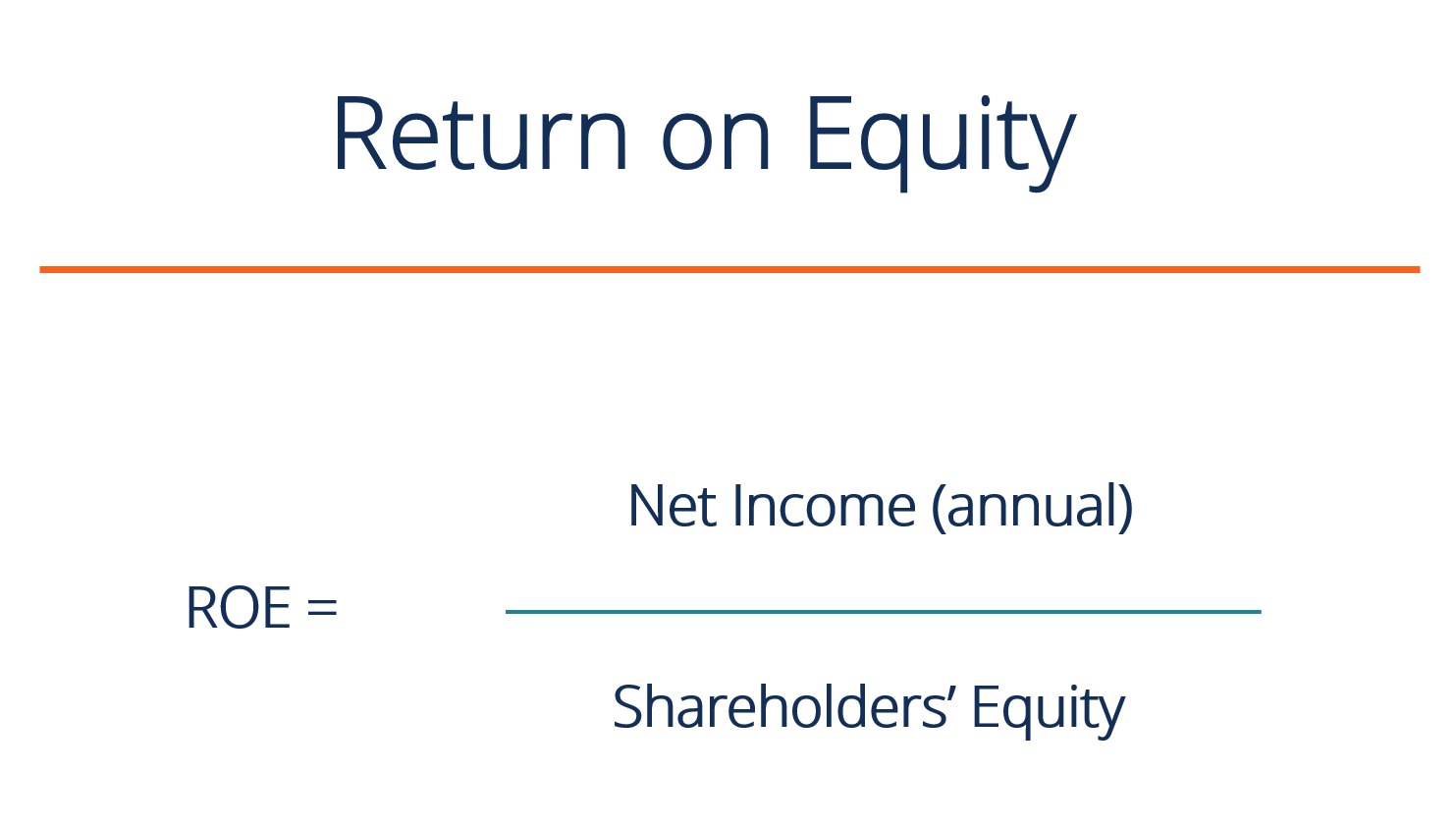

The ROE Formula and its Interpretation

The fundamental formula for Return on Equity is straightforward:

ROE = Net Income / Shareholders’ Equity

While the formula is simple, its interpretation requires a nuanced understanding of what the resulting percentage signifies and how it should be contextualized.

Calculating ROE: A Practical Example

Let’s consider a hypothetical company, “Tech Innovators Inc.,” to illustrate the ROE calculation.

- Net Income for the year: $10 million

- Shareholders’ Equity at the beginning of the year: $80 million

- Shareholders’ Equity at the end of the year: $120 million

To calculate ROE using average shareholders’ equity:

- Average Shareholders’ Equity: ($80 million + $120 million) / 2 = $100 million

- ROE: $10 million / $100 million = 0.10 or 10%

This 10% ROE indicates that for every dollar of shareholder equity invested in Tech Innovators Inc., the company generated $0.10 in profit during the year.

Interpreting the ROE Ratio: What Does the Number Mean?

A higher ROE generally suggests that a company is more efficient at generating profits from its shareholders’ investments. Conversely, a lower ROE might indicate inefficiencies, poor management, or a less profitable business model. However, interpreting ROE in isolation can be misleading. Several factors need to be considered for a comprehensive analysis:

- Industry Benchmarks: ROE varies significantly across different industries. A 15% ROE might be excellent in a mature, low-growth industry but mediocre in a fast-growing, technology-driven sector. Therefore, comparing a company’s ROE to its peers within the same industry is crucial.

- Company Growth Stage: Early-stage, rapidly growing companies may have lower ROE as they reinvest heavily in expansion, which can temporarily suppress profits relative to equity. Mature, stable companies might exhibit higher ROE due to established market positions and efficient operations.

- Financial Leverage: A company can increase its ROE by taking on more debt (increasing financial leverage). While this can amplify returns when things go well, it also increases risk. Analyzing ROE alongside leverage ratios (like the debt-to-equity ratio) provides a more complete picture.

- Sustainability of Earnings: It’s important to ascertain whether the net income used in the ROE calculation is sustainable. One-time gains or accounting adjustments can artificially inflate ROE for a single period, making it an unreliable indicator of future performance.

- Dividend Policy: Companies that pay out a large portion of their earnings as dividends will have slower growth in retained earnings, potentially impacting their ROE. Conversely, companies that retain more earnings for reinvestment may see their ROE improve over time if those investments are profitable.

The Significance of ROE in Financial Analysis

Return on Equity is not just an academic exercise; it is a powerful tool used by investors, analysts, and management alike for various strategic purposes. Its ability to link profitability directly to the owners’ stake makes it a cornerstone of shareholder value analysis.

For Investors: Evaluating Investment Opportunities

For investors, ROE serves as a key metric for:

- Identifying Profitable Companies: Companies with consistently high and growing ROE are often indicators of strong management and a competitive business model.

- Comparing Investment Options: When faced with multiple investment choices, comparing their ROE alongside other financial metrics can help investors identify those with the best potential for generating returns.

- Assessing Management Effectiveness: A high ROE can signal that a company’s management team is effectively deploying shareholder capital to create value. Conversely, a declining ROE might prompt an investor to question management’s strategic decisions.

- Spotting Potential Red Flags: An unusually high or volatile ROE can sometimes signal aggressive accounting practices or excessive leverage, warranting further investigation.

For Management: Driving Performance and Strategy

Company management uses ROE to:

- Monitor Operational Efficiency: ROE provides a clear measure of how well the company is converting its equity base into profits. Management can track ROE trends to identify areas where efficiency can be improved.

- Guide Capital Allocation Decisions: Understanding the drivers of ROE can help management make better decisions about where to invest capital. Projects or divisions that promise to enhance ROE are often prioritized.

- Set Performance Targets: ROE can be used as a key performance indicator (KPI) for the company and its various divisions, aligning strategic goals with financial outcomes.

- Communicate with Stakeholders: ROE is a widely understood metric that can be used to communicate the company’s financial performance and strategic progress to shareholders and the broader financial community.

Limitations and Nuances of ROE Analysis

While ROE is a valuable metric, it’s essential to acknowledge its limitations and use it in conjunction with other financial tools for a complete understanding.

- Impact of Share Buybacks: Share buybacks reduce the amount of outstanding shares and therefore shareholders’ equity. This can artificially inflate ROE without necessarily indicating improved operational performance.

- Negative Equity: In cases of significant losses, a company can have negative shareholders’ equity. In such scenarios, ROE becomes meaningless or even misleading.

- Variations in Accounting Practices: Different accounting methods can affect net income and shareholders’ equity, leading to variations in ROE even for companies in similar industries.

- Short-Term Focus: ROE can sometimes encourage a short-term focus on maximizing immediate profits, potentially at the expense of long-term investments or sustainable growth.

Therefore, a thorough financial analysis will always involve looking at ROE in the context of other financial ratios, industry trends, and the company’s overall strategic objectives.

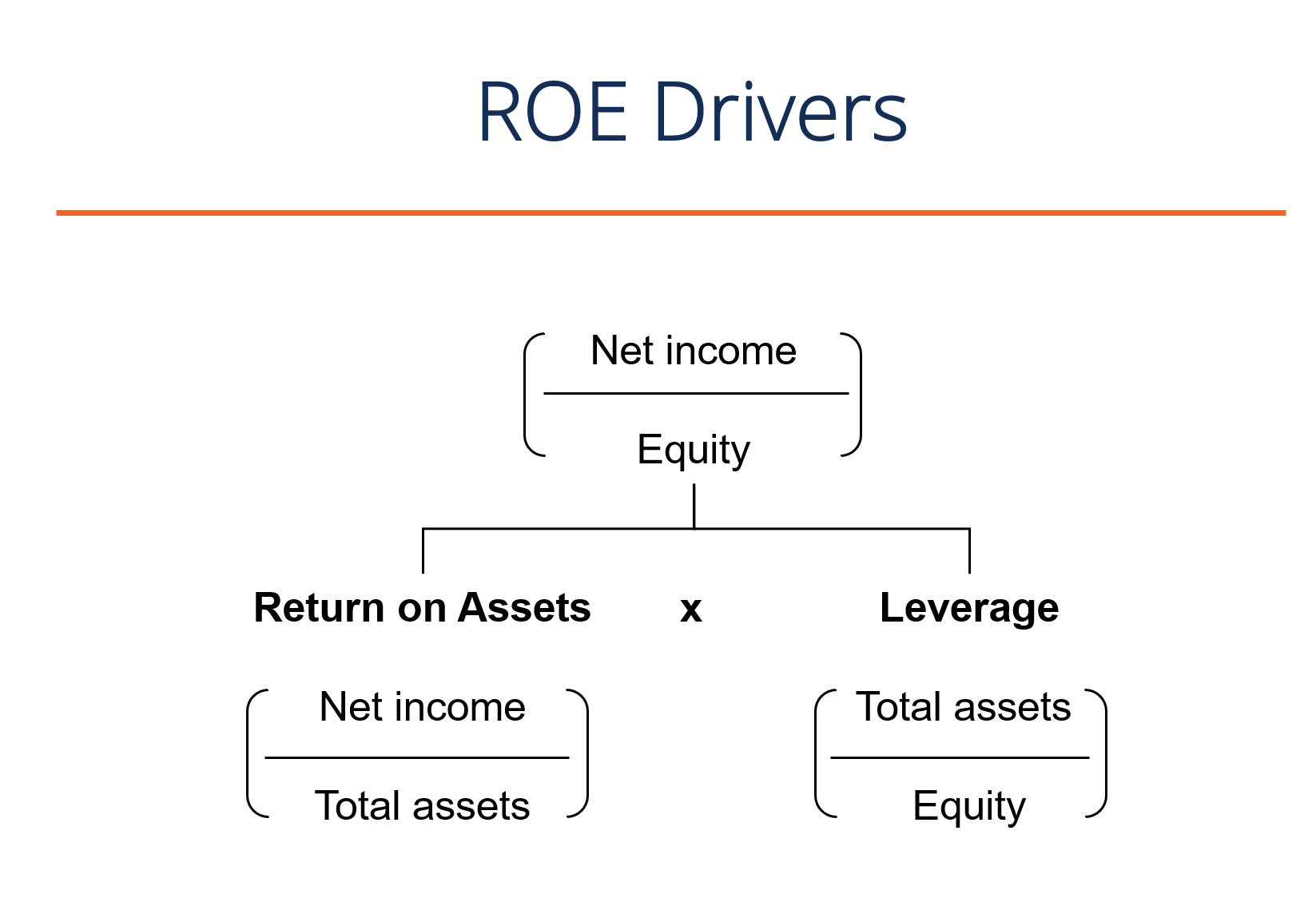

Advanced ROE Analysis: The DuPont Framework

To gain a deeper understanding of what drives a company’s ROE, the DuPont Analysis (also known as the DuPont Identity or DuPont Model) is an invaluable framework. It breaks down ROE into its component parts, allowing for a more granular examination of profitability drivers.

Deconstructing ROE: The DuPont Identity

The DuPont framework decomposes ROE into three key components:

ROE = Net Profit Margin x Asset Turnover x Equity Multiplier

Let’s break down each of these components:

Net Profit Margin: Operational Efficiency in Profit Generation

Net Profit Margin = Net Income / Revenue

This ratio measures how much profit a company generates for every dollar of sales. A higher net profit margin indicates that a company is more efficient at controlling its costs relative to its revenue. It reflects the effectiveness of pricing strategies, cost management, and operational efficiency.

Asset Turnover: Efficiency in Utilizing Assets

Asset Turnover = Revenue / Average Total Assets

This ratio measures how efficiently a company uses its assets to generate sales. A higher asset turnover suggests that a company is generating more revenue with its existing asset base, indicating efficient asset utilization. Industries with high sales volume and low asset intensity, such as retail, typically have higher asset turnover ratios.

Equity Multiplier: The Impact of Financial Leverage

Equity Multiplier = Average Total Assets / Average Shareholders’ Equity

This ratio, also known as the financial leverage ratio, quantifies the extent to which a company uses debt financing. A higher equity multiplier indicates that a company relies more heavily on debt to finance its assets. While leverage can amplify returns (as seen in the ROE formula), it also magnifies risk. An increasing equity multiplier, especially when coupled with a stable or declining net profit margin, can signal growing financial risk.

The Power of Decomposition: Uncovering ROE Drivers

By examining these three components, analysts can identify whether a high or low ROE is primarily driven by strong operational performance (high net profit margin and asset turnover), effective use of financial leverage (high equity multiplier), or a combination of factors.

For instance, a company with a consistently high ROE might be achieving this through:

- Superior Profitability: A high net profit margin due to strong brand recognition, premium pricing, or exceptionally low operating costs.

- Efficient Asset Management: A high asset turnover ratio, suggesting that the company is adept at converting its assets into sales rapidly.

- Strategic Leverage: A judicious use of debt that amplifies returns without exposing the company to excessive risk.

Conversely, a declining ROE could be traced to a shrinking net profit margin due to increased competition, a decrease in asset turnover indicating operational inefficiencies or slowing sales, or an excessive reliance on debt that is becoming burdensome. The DuPont analysis provides a roadmap to diagnose the root causes of changes in ROE, enabling more targeted strategic interventions.

In conclusion, Return on Equity is a fundamental metric in finance that provides a vital link between a company’s profitability and the capital invested by its shareholders. While the basic formula is simple, its true value lies in its comprehensive interpretation, its comparison against industry benchmarks, and its decomposition through frameworks like the DuPont Analysis. By understanding ROE, investors and management alike can gain deeper insights into a company’s financial health, operational efficiency, and its ability to create sustainable shareholder value.