The question “what is net income on a balance sheet” immediately presents a slight conceptual challenge. To address this accurately and informatively, it’s crucial to understand the fundamental differences between the financial statements on which net income does appear and the balance sheet itself. This article will delve into this distinction, explaining where net income originates, how it’s reported, and its vital relationship to the balance sheet without directly appearing on it.

The Income Statement: The True Home of Net Income

Net income, often referred to as the “bottom line,” is the ultimate measure of a company’s profitability over a specific period. It represents the profit remaining after all expenses, including taxes and interest, have been deducted from total revenues. Crucially, net income is not a permanent fixture on the balance sheet. Instead, it is a key figure generated by the income statement (also known as the profit and loss statement or P&L).

Understanding Revenue and Expenses

The income statement begins by detailing a company’s revenues, which are the earnings generated from its primary business activities. This can include sales of goods, provision of services, or investment income. Following the revenue section, a comprehensive list of expenses is presented. These expenses can be broadly categorized into:

Cost of Goods Sold (COGS)

This directly relates to the production or acquisition of the goods or services sold. For a manufacturing company, COGS includes raw materials, direct labor, and manufacturing overhead. For a retailer, it’s the cost of purchasing inventory.

Operating Expenses

These are the costs incurred in the day-to-day running of the business, excluding those directly tied to the production of goods or services. Common operating expenses include:

- Selling, General, and Administrative (SG&A) Expenses: This encompasses marketing, advertising, sales salaries, rent, utilities, and administrative staff salaries.

- Research and Development (R&D) Expenses: Costs associated with developing new products or improving existing ones.

- Depreciation and Amortization: The systematic allocation of the cost of tangible assets (depreciation) and intangible assets (amortization) over their useful lives.

Other Expenses

This category can include items not directly related to core operations, such as:

- Interest Expense: The cost of borrowing money.

- Taxes: Income taxes levied by governments.

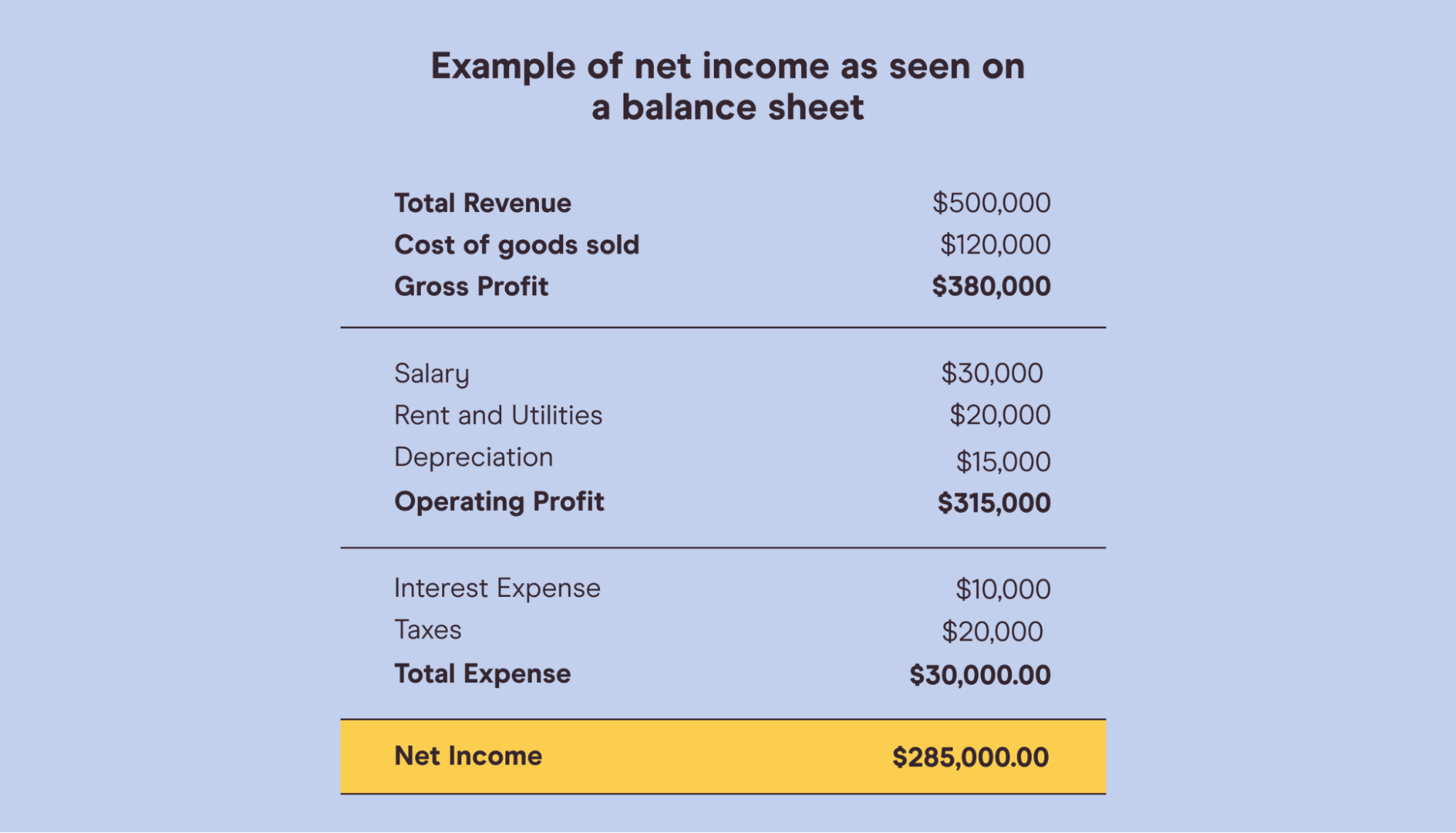

The Calculation of Net Income

The process of calculating net income on the income statement is a sequential subtraction:

Revenue – Cost of Goods Sold = Gross Profit

Gross Profit – Operating Expenses = Operating Income (or EBIT – Earnings Before Interest and Taxes)

Operating Income – Interest Expense = Earnings Before Tax (EBT)

EBT – Taxes = Net Income

This step-by-step calculation clearly illustrates how net income is derived. It’s a measure of performance over a period of time (e.g., a quarter or a fiscal year).

The Balance Sheet: A Snapshot of Financial Position

The balance sheet, in contrast to the income statement, provides a snapshot of a company’s financial position at a specific point in time (e.g., as of December 31, 2023). It adheres to the fundamental accounting equation:

Assets = Liabilities + Equity

This equation must always balance.

Understanding the Components of the Balance Sheet

Assets

These are the resources owned by the company that have economic value and are expected to provide future benefits. Assets are typically categorized into:

- Current Assets: Assets expected to be converted into cash, sold, or consumed within one year or the operating cycle, whichever is longer. Examples include cash, accounts receivable, inventory, and short-term investments.

- Non-Current Assets (or Long-Term Assets): Assets expected to provide benefits for more than one year. Examples include property, plant, and equipment (PP&E), long-term investments, and intangible assets like patents and goodwill.

Liabilities

These represent the obligations of the company to external parties. Liabilities are also categorized by their maturity:

- Current Liabilities: Obligations due within one year or the operating cycle. Examples include accounts payable, salaries payable, short-term loans, and the current portion of long-term debt.

- Non-Current Liabilities (or Long-Term Liabilities): Obligations due in more than one year. Examples include long-term loans, bonds payable, and deferred tax liabilities.

Equity

This represents the owners’ stake in the company. It’s what remains after deducting liabilities from assets. Equity is comprised of:

- Paid-in Capital: The amount of money shareholders have invested in exchange for stock.

- Retained Earnings: This is where the connection between net income and the balance sheet becomes apparent, albeit indirectly. Retained earnings represent the cumulative profits of the company that have not been distributed to shareholders as dividends.

The Indirect Link: Retained Earnings and Net Income

While net income itself doesn’t have a line item labeled “Net Income” on the balance sheet, its impact is reflected through the retained earnings account. The income statement’s net income for a period is added to the previous period’s retained earnings. If a company pays dividends, these are subtracted from retained earnings. The retained earnings figure reported on the balance sheet at the end of a period is a result of the cumulative net income earned over the company’s life, less all dividends paid out.

The Statement of Retained Earnings

To explicitly show this flow, many companies present a Statement of Retained Earnings (or a Statement of Changes in Equity). This statement bridges the income statement and the balance sheet. It typically starts with the beginning balance of retained earnings, adds net income for the period (from the income statement), and subtracts any dividends paid. The ending balance of retained earnings from this statement is then reported on the balance sheet.

The formula for calculating the ending retained earnings is:

Beginning Retained Earnings + Net Income – Dividends = Ending Retained Earnings

This statement highlights that net income, a profit measure from the income statement, directly influences the equity section of the balance sheet through the retained earnings account.

Why the Distinction Matters

Understanding the difference between the income statement and the balance sheet, and how net income fits into this framework, is fundamental for anyone analyzing a company’s financial health.

For Investors

Investors use net income from the income statement to gauge a company’s profitability and its ability to generate returns. They then look at the balance sheet to understand the company’s financial structure, its assets and liabilities, and how equity has been built over time. A growing net income, reflected in increasing retained earnings, can signal a healthy and expanding business.

For Creditors

Creditors, such as banks, are primarily interested in a company’s ability to repay its debts. While net income indicates a company’s earning power, the balance sheet reveals its liquidity (ability to meet short-term obligations) and solvency (ability to meet long-term obligations). A strong balance sheet, with sufficient assets to cover liabilities, is crucial for obtaining credit, even if the net income is temporarily lower.

For Management

Company management relies on both statements for decision-making. The income statement helps them assess the effectiveness of their strategies in generating revenue and controlling costs. The balance sheet provides insights into asset utilization, debt levels, and the overall financial capacity of the company to invest in future growth.

In essence, the income statement tells the story of a company’s performance over time, while the balance sheet paints a picture of its financial standing at a given moment. Net income is the engine of profitability that, when reinvested, contributes to the growth and strengthening of the company’s financial position as depicted on the balance sheet through retained earnings. Therefore, while you won’t find “net income” as a direct line item on the balance sheet, its presence is undeniably felt through the vital account of retained earnings, making both statements indispensable for a complete financial understanding.