The term “perfect credit score” is a subject of much discussion and, at times, a source of confusion for consumers. While the concept of achieving an ideal credit standing is aspirational, understanding what constitutes “perfect” is crucial for navigating the financial landscape effectively. This article delves into the nuances of credit scoring, exploring what a perfect score signifies, the factors that contribute to it, and the practical implications of achieving such a benchmark.

Understanding Credit Scores: The Foundation of Financial Health

At its core, a credit score is a three-digit number that represents an individual’s creditworthiness. Lenders, from mortgage providers to credit card companies, use these scores to assess the risk associated with lending money. A higher score indicates a lower risk, making it more likely for an individual to be approved for loans and to secure favorable interest rates. The most widely used credit scoring models are developed by Fair Isaac Corporation (FICO) and VantageScore. While both have their proprietary algorithms, they generally rely on similar core principles.

The Mechanics of Credit Scoring: How Your Score is Calculated

The journey to a high credit score, and indeed a “perfect” one, is paved with responsible financial habits. Understanding the factors that influence this score is the first step towards mastering it. These factors, weighted differently in scoring models, paint a comprehensive picture of your financial behavior.

Payment History: The Cornerstone of Your Credit Reputation

By far the most significant factor in determining your credit score is your payment history. This encompasses whether you pay your bills on time, every time. Late payments, even by a few days, can have a detrimental impact, and missed payments or defaults can significantly damage your score. Consistent on-time payments demonstrate reliability and a commitment to meeting your financial obligations, forming the bedrock of a strong credit profile. This includes not just credit card payments but also loan installments, mortgage payments, and even utility bills if they are reported to credit bureaus.

Credit Utilization: The Balancing Act of Borrowing

The amount of credit you use relative to your total available credit is known as credit utilization. Experts generally recommend keeping this ratio below 30%, and ideally below 10%, for optimal score impact. High credit utilization signals to lenders that you may be overextended financially, even if you make your payments on time. This is because it suggests a reliance on borrowed funds, which can increase the perceived risk. Strategically managing your credit balances is therefore essential. This involves not maxing out credit cards and, where possible, increasing your credit limits rather than simply spending more.

Length of Credit History: The Value of Time

The longer you have managed credit responsibly, the more information lenders have to assess your behavior. A longer credit history, when marked by positive activity, generally contributes to a higher credit score. This factor emphasizes the importance of starting early and maintaining good habits over an extended period. It’s not about having a lot of credit accounts, but about having a consistent history of responsible management over time. New credit, while sometimes necessary, can temporarily lower your score due to the average age of your accounts decreasing.

Credit Mix: Diversification of Your Financial Portfolio

Lenders like to see that you can manage different types of credit responsibly. This includes a mix of revolving credit (like credit cards) and installment loans (like mortgages or car loans). Having a diverse credit mix can positively impact your score, as it demonstrates an ability to handle various credit obligations. However, it’s important to note that opening new accounts solely for the sake of credit mix is generally not advisable. This factor is more about how your existing credit portfolio is managed.

New Credit: A Cautious Approach

Opening multiple new credit accounts in a short period can negatively affect your credit score. Each time you apply for credit, a “hard inquiry” is placed on your credit report, which can slightly lower your score. While necessary at times, it’s advisable to be judicious about applying for new credit and to space out applications. The impact of new credit is usually temporary, but it’s a factor to be mindful of when aiming for a perfect score.

What Constitutes a “Perfect” Credit Score?

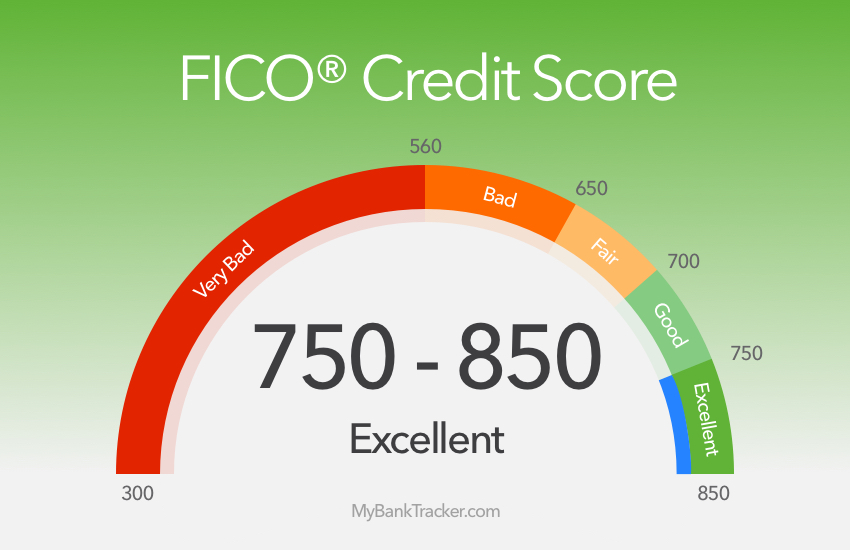

The concept of a “perfect” credit score can be somewhat elusive, as different scoring models and lenders may have slightly different benchmarks. However, generally speaking, a credit score in the range of 740 and above is considered excellent. Scores of 800 and above are often seen as approaching perfection, offering the most advantageous terms and approvals.

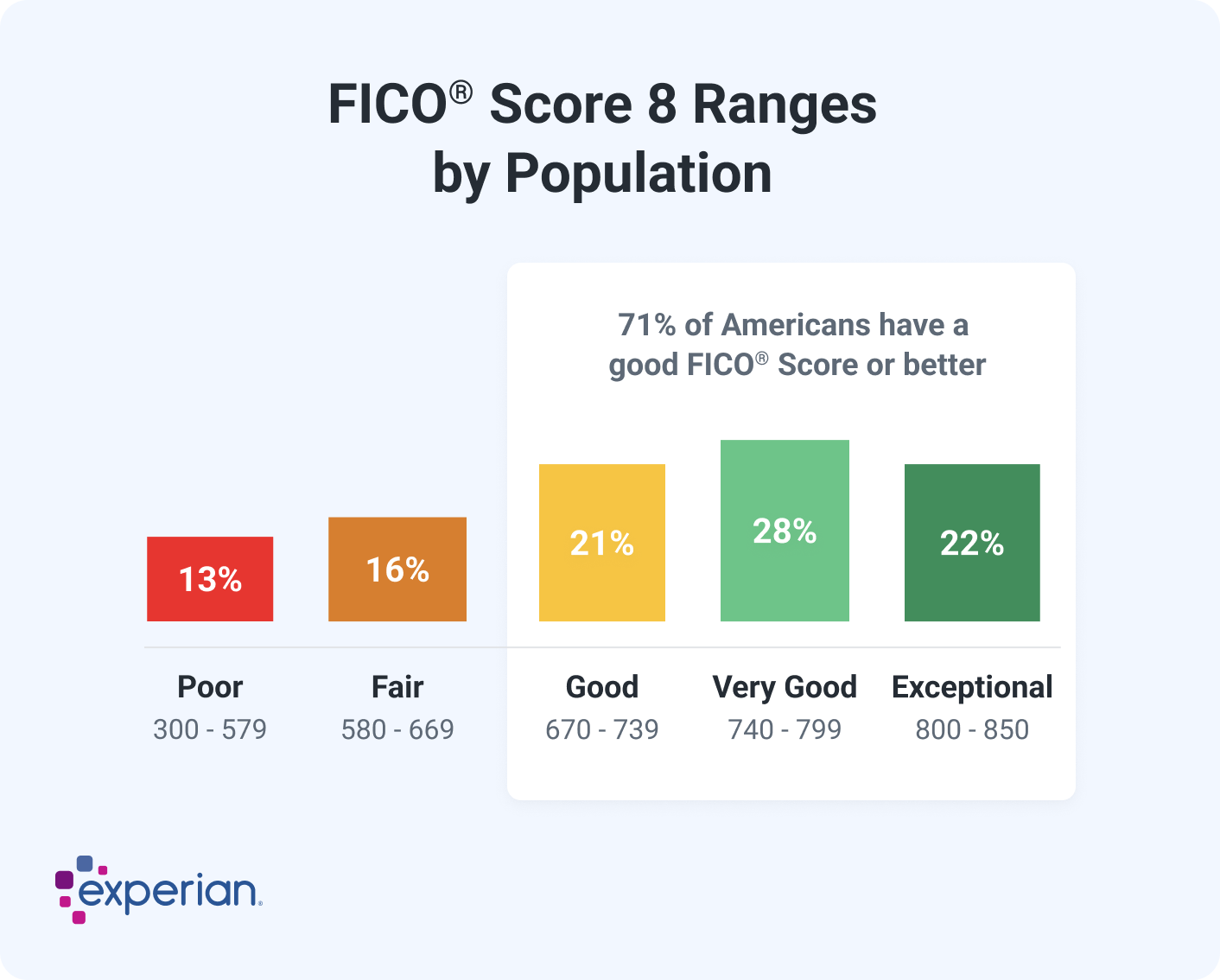

The Spectrum of Scores: From Poor to Exceptional

Credit scores are typically categorized to provide a general understanding of creditworthiness:

- Poor (300-579): Indicates a high risk for lenders.

- Fair (580-669): Suggests some credit issues, but manageable for some lenders.

- Good (670-739): A solid score that will likely qualify for most loans, though perhaps not the best rates.

- Very Good (740-799): Excellent credit, leading to favorable loan terms and higher approval odds.

- Exceptional (800-850): The pinnacle of creditworthiness, often referred to as “perfect” credit.

The Significance of an Exceptional Score: Beyond Just Approval

Achieving an exceptional credit score (typically 800+) unlocks a wealth of financial benefits. It signifies an impeccable track record of responsible credit management, making you an extremely low-risk borrower in the eyes of lenders. This translates into tangible advantages:

- Lowest Interest Rates: You’ll qualify for the most competitive interest rates on mortgages, auto loans, personal loans, and credit cards. This can save you thousands of dollars over the life of a loan.

- Higher Approval Odds: Applications for loans and credit cards are almost guaranteed to be approved, even for premium or exclusive financial products.

- Larger Credit Limits: You’ll be offered higher credit limits, providing greater financial flexibility and potentially improving your credit utilization ratio.

- Easier Rental Applications: Landlords often view applicants with exceptional credit as more reliable tenants.

- Better Insurance Premiums: In some states, credit scores can influence auto and homeowner’s insurance premiums. A higher score may lead to lower rates.

- Waived Security Deposits: For utilities and mobile phone plans, you might be able to waive security deposits.

The Path to Perfection: Strategies for Maximizing Your Score

Attaining and maintaining an exceptional credit score is not a matter of luck; it’s the result of consistent, disciplined financial behavior. While the exact formula remains proprietary, the principles for building a stellar credit profile are well-established.

Cultivating Impeccable Payment Habits: The Foundation

The absolute most critical habit is making all payments on time, without exception. This means setting up automatic payments for all bills, utilizing calendar reminders, or even arranging for direct debits from your bank account. For credit cards, paying the full statement balance by the due date is ideal to avoid interest charges and demonstrate responsible management. If you can’t pay the full balance, at least ensure you pay more than the minimum payment to reduce your outstanding debt and prevent late fees.

Strategic Credit Utilization: Keeping Balances Low

As mentioned earlier, keeping your credit utilization ratio low is paramount. This involves a two-pronged approach: managing your spending and strategically increasing your credit limits. Avoid using more than 30% of your available credit on any single card, and aim to keep your overall utilization even lower. If you find yourself approaching higher utilization, consider making multiple payments throughout the billing cycle to keep the reported balance low, or request a credit limit increase from your current card issuers.

The Long Game: Patience and Consistency

Building a strong credit history takes time. For those starting out, it’s essential to be patient and focus on consistent positive behavior. Avoid closing old, unused credit accounts, as this can shorten your average credit history length and potentially increase your credit utilization. Instead, ensure these accounts are in good standing, perhaps by making a small purchase occasionally and paying it off immediately to keep them active.

Monitoring Your Credit: Vigilance is Key

Regularly checking your credit reports from the three major credit bureaus (Equifax, Experian, and TransUnion) is crucial. You are entitled to a free report from each bureau annually through AnnualCreditReport.com. This allows you to identify any errors or fraudulent activity that could be negatively impacting your score. It’s also an excellent way to stay informed about the information being reported and to track your progress.

When Perfection Isn’t the Only Goal: The Value of a Good Score

While striving for a “perfect” credit score is commendable, it’s important to recognize that a score in the “very good” range (740-799) often provides most of the significant benefits. For many individuals, achieving and maintaining an excellent score is more than sufficient to secure favorable financial terms and opportunities. The marginal benefits of moving from an 800 to an 830, for example, might be less impactful than the effort required to get there.

The Practicality of “Excellent” vs. “Perfect”

The difference in interest rates or loan terms between someone with an 800 score and someone with an 830 score might be negligible. Lenders often have tiers of approval, and once you reach a certain threshold of creditworthiness, the advantages plateau. Therefore, focusing on building a consistently strong credit history with on-time payments and manageable debt levels should be the primary objective. The “perfect” score is a desirable outcome, but the journey to an “excellent” score is where the most significant financial gains are realized.

Avoiding the Pitfalls of Obsession

It’s possible to become overly focused on chasing a perfect score, leading to unnecessary stress or even detrimental financial decisions. For instance, opening multiple credit accounts solely to boost a score can sometimes have the opposite effect due to hard inquiries and a shortened average account age. It’s essential to approach credit management with a balanced perspective, prioritizing long-term financial well-being over the pursuit of a single, arbitrary number.

Conclusion: A Journey of Financial Responsibility

The quest for a “perfect credit score” is ultimately a journey toward impeccable financial responsibility. It is built on a foundation of consistent, on-time payments, judicious use of credit, and a long-term commitment to sound financial habits. While the exact definition of “perfect” can vary, achieving an exceptional score (800+) unlocks significant advantages in the financial world, from lower interest rates to higher approval odds. However, it’s equally important to recognize the immense value of an “excellent” credit score, which often provides the most tangible benefits with less extreme effort. By understanding the factors that influence credit scores and adopting disciplined financial practices, individuals can confidently navigate their financial lives, secure their goals, and build a strong foundation for future prosperity.