While the article title “What year was the IRS established?” might initially seem out of place within a tech-focused publication, it actually offers a fascinating entry point into understanding the historical evolution of governmental data management and its parallels with modern technological advancements. To truly appreciate the present-day capabilities of entities like the IRS, understanding their origins and the technological constraints they operated under is crucial. This exploration delves into the historical context of the IRS’s establishment, tracing the roots of its administrative functions and setting the stage for how technology, from its nascent stages to the sophisticated systems of today, has shaped and continues to shape tax collection and management.

![]()

The establishment of any large governmental organization is a reflection of societal needs and the administrative capacity available at a given time. For the IRS, its origins are deeply intertwined with the financial demands of a nation, particularly during times of conflict. Understanding the “why” and “how” of its inception provides a valuable lens through which to view the subsequent technological revolutions that have transformed its operations.

The Genesis of a Federal Tax Authority

The foundation of the Internal Revenue Service (IRS) as a federal entity is a story that unfolds through legislative action and the evolving needs of the United States government. Its establishment was not a single, sudden event, but rather a process that culminated in the creation of a permanent and robust infrastructure for federal income tax collection.

Early Forays into Federal Taxation

Before the establishment of a permanent federal income tax, the U.S. government relied on a variety of revenue streams, primarily tariffs and excise taxes. However, the necessity of funding significant national endeavors, particularly wartime efforts, repeatedly brought the concept of direct federal taxation to the forefront. The Civil War, in particular, necessitated a substantial increase in government revenue, leading to the introduction of the nation’s first income tax in 1861. This was a temporary measure, intended to finance the Union’s war effort.

The Revenue Act of 1861 introduced a tax on incomes exceeding $800 annually. However, its implementation was delayed due to the outbreak of hostilities. A revised income tax was enacted in 1862, and this legislation saw active collection for the duration of the war and for several years afterward. This period marked a significant, albeit temporary, shift in federal revenue generation, demonstrating the government’s capacity to levy and collect direct taxes on its citizens.

The Rise of a Permanent Income Tax System

Following the Civil War, the income tax was repealed in 1872. For several decades, the federal government returned to its reliance on tariffs and excise taxes. However, the late 19th century saw growing calls for a more equitable tax system. Concerns over the concentration of wealth and the perceived regressiveness of existing taxes fueled a movement for a federal income tax.

This push culminated in the passage of the Revenue Act of 1894, which attempted to reintroduce a federal income tax. However, this act was quickly challenged and declared unconstitutional by the Supreme Court in the case of Pollock v. Farmers’ Loan & Trust Co. in 1895, which held that direct taxes on income from property were unconstitutional without apportionment among the states. This legal setback underscored the need for a constitutional amendment to grant Congress the explicit power to levy an income tax.

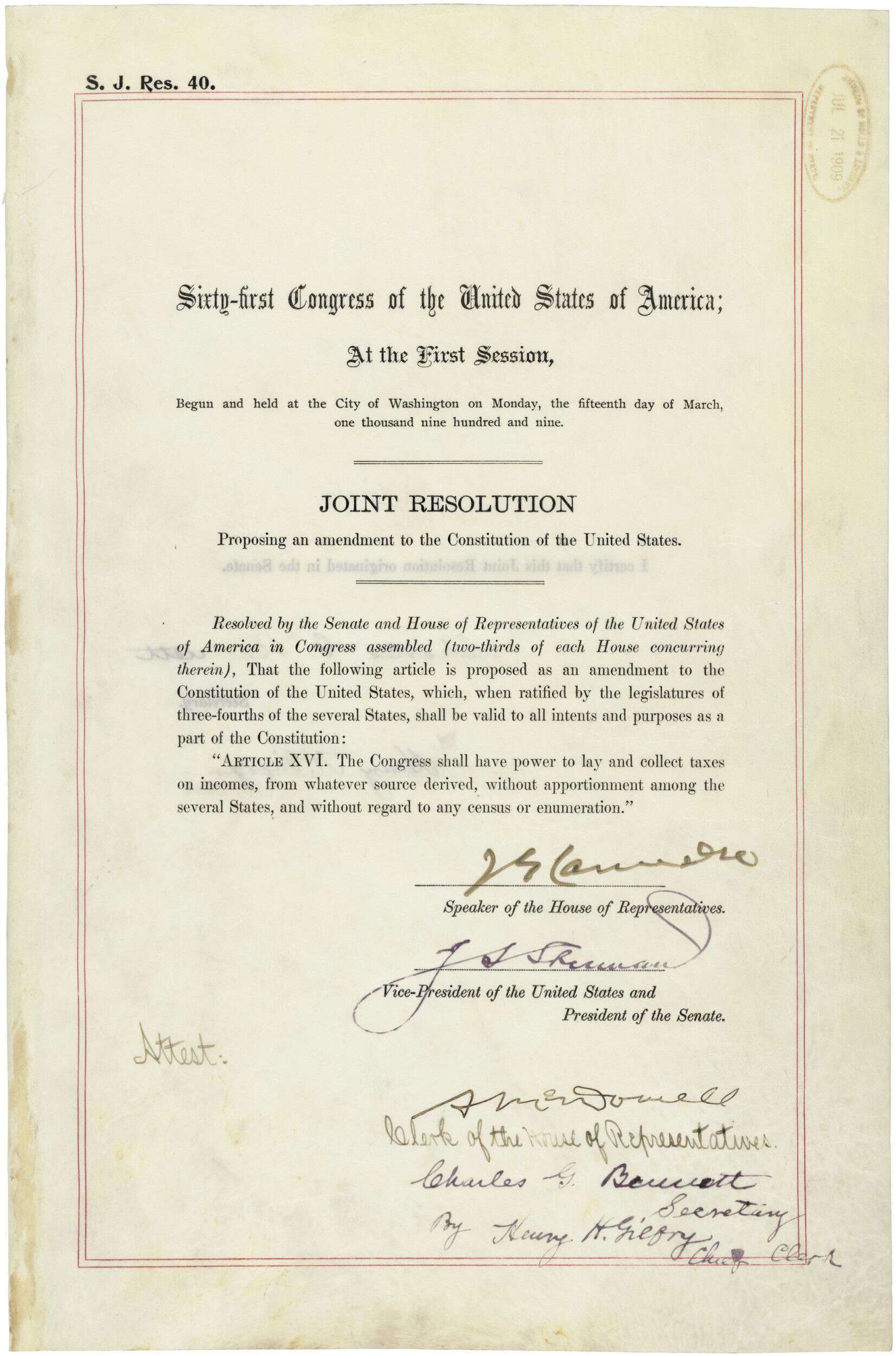

The 16th Amendment: Paving the Way

The crucial turning point for the establishment of a permanent federal income tax system was the ratification of the 16th Amendment to the U.S. Constitution in 1913. This amendment states: “The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.”

The ratification of the 16th Amendment provided the constitutional authority necessary for Congress to enact a lasting income tax. This amendment fundamentally reshaped the financial landscape of the United States, granting the federal government a direct and consistent source of revenue that would prove indispensable in the 20th century and beyond.

The Birth of the Bureau of Internal Revenue

With the constitutional hurdle cleared, Congress moved swiftly to establish a permanent agency responsible for administering the newly empowered federal income tax. This led to the creation of the Bureau of Internal Revenue, the direct precursor to today’s IRS.

Legislative Action and Initial Structure

Following the ratification of the 16th Amendment, Congress passed the Revenue Act of 1913. This landmark legislation not only established a new federal income tax but also solidified the administrative framework for its collection. The Bureau of Internal Revenue was formally established as the entity tasked with this monumental undertaking. Its initial mandate was to collect taxes levied under the new income tax law, as well as existing excise taxes and other internal revenue sources.

The early structure of the Bureau was relatively modest compared to its modern iteration. It comprised a commissioner of internal revenue and a staff of clerks and agents tasked with processing tax returns, assessing liabilities, and enforcing tax laws. The operational procedures were, by today’s standards, extremely rudimentary. Tax forms were often paper-based, and manual record-keeping was the norm. The sheer volume of data to be processed and the complexities of tax law presented significant challenges even in these early days.

Early Challenges and Growth

The Bureau of Internal Revenue faced numerous challenges in its formative years. Educating the public about the new income tax system was a significant undertaking. Ensuring compliance and preventing evasion required the development of enforcement mechanisms and investigative capabilities. Furthermore, the scale of operations grew exponentially with each passing year, especially as the federal government’s role in society expanded.

The outbreak of World War I in 1914 and America’s subsequent entry into the conflict in 1917 dramatically increased the government’s need for revenue. The income tax, empowered by the 16th Amendment, became a crucial source of funding for the war effort. This surge in tax collection necessitated a rapid expansion of the Bureau of Internal Revenue, both in terms of personnel and infrastructure. The organization began to take on a more complex and bureaucratic structure to manage the burgeoning workload.

The Evolution into the Modern IRS

The Bureau of Internal Revenue continued to evolve throughout the 20th century, adapting to changing economic conditions, legislative reforms, and, most significantly, technological advancements. The transition from a manual, paper-based system to a highly digitized and automated operation has been a defining characteristic of its modern history.

Modernization and Technological Integration

The mid-20th century marked a period of significant transformation for the Bureau. As the U.S. economy grew and tax laws became more intricate, the administrative burden on the Bureau increased dramatically. This necessitated a serious investment in mechanization and automation. Early efforts involved the use of punch cards and rudimentary computers to process tax returns and manage taxpayer accounts.

The latter half of the 20th century saw an acceleration of this technological integration. The establishment of sophisticated computer systems, optical character recognition (OCR) technology, and eventually, the internet, revolutionized the Bureau’s operations. Taxpayers gained the ability to file returns electronically, and the Bureau could process vast amounts of data with unprecedented speed and accuracy. This technological leap was not merely about efficiency; it was about enabling the management of a vastly more complex tax system and supporting a growing population of taxpayers.

The Birth of the Internal Revenue Service (IRS)

While the Bureau of Internal Revenue was the operational entity, the formal name change to the Internal Revenue Service (IRS) occurred in 1953. This rebranding signified not just a change in name but a recognition of the agency’s expanded role and its central position in the nation’s fiscal machinery. The IRS inherited the legacy of the Bureau of Internal Revenue and continued to build upon its foundations, particularly in leveraging technology to meet its mission.

The 1970s and 1980s saw significant investments in taxpayer data processing and automation, laying the groundwork for the digital age of tax administration. The development of taxpayer identification numbers (Social Security numbers), electronic filing systems, and sophisticated databases allowed the IRS to manage information more effectively and improve compliance. This ongoing adaptation and modernization underscore the critical role that technological innovation has played in enabling the IRS to fulfill its mandate throughout its history. The journey from a nascent revenue collection agency to a sophisticated, technologically advanced organization is a testament to continuous adaptation and the persistent pursuit of efficient governance.