Understanding the diverse landscape of auto insurance can feel like navigating a complex maze. For many drivers, the sheer volume of policy options, coverage types, and terminology can be overwhelming. This guide aims to demystify the world of auto insurance, breaking down the essential components that make up a robust policy. Whether you’re a seasoned driver seeking to optimize your coverage or a new driver embarking on your insurance journey, a clear understanding of your options is crucial for both peace of mind and financial protection.

Understanding the Fundamentals of Auto Insurance

At its core, auto insurance is a contract between you and an insurance company. In exchange for regular premium payments, the insurer agrees to cover certain financial losses that may arise from an auto accident or other covered incidents. These losses can include damage to your vehicle, medical expenses for injuries sustained, and liability for damage or injury caused to others. The primary purpose of auto insurance is to mitigate the significant financial burden that can result from unforeseen events on the road.

The Pillars of Coverage: Liability Insurance

Liability insurance is the bedrock of most auto insurance policies and is mandated by law in almost every state. It’s designed to protect you financially if you are at fault in an accident and cause damage to another person’s property or injure them. Liability coverage is typically divided into two main components:

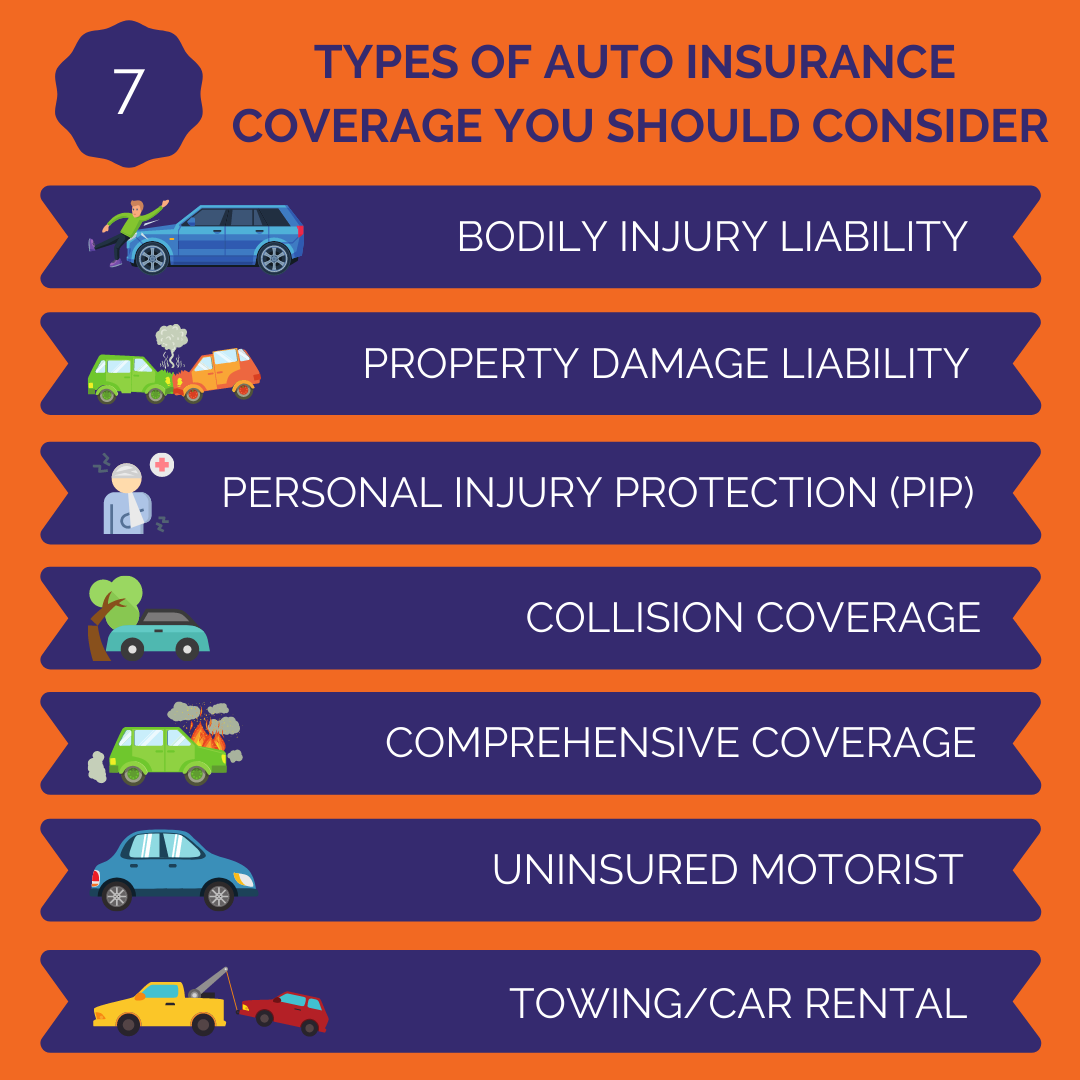

Bodily Injury Liability

This coverage pays for the medical expenses, lost wages, and pain and suffering of individuals who are injured in an accident where you are deemed responsible. If your negligence leads to severe injuries for another driver, their passengers, or pedestrians, this coverage is what shields you from potentially crippling lawsuits and out-of-pocket expenses. Minimum liability limits are set by state law, but these often fall far short of covering the true cost of serious injuries. Therefore, many drivers opt for higher limits to ensure adequate protection.

Property Damage Liability

This component of liability insurance covers the cost of repairing or replacing property that you damage in an accident. This most commonly refers to damage to the other vehicle(s) involved, but it can also extend to other property such as fences, buildings, or mailboxes. Again, state minimums may be insufficient to cover the cost of significant property damage.

Protecting Your Own Vehicle: Physical Damage Coverage

While liability insurance protects others from your actions, physical damage coverage is focused on repairing or replacing your own vehicle. This category is further divided into two distinct types of coverage:

Collision Coverage

Collision insurance pays for damage to your vehicle that occurs as a result of a collision with another vehicle or an object, such as a tree, guardrail, or pothole. This coverage is typically optional unless you have a car loan or lease, in which case the lender will likely require it. Collision coverage often comes with a deductible, which is the amount you agree to pay out-of-pocket before the insurance company begins to cover the remaining costs. Choosing a higher deductible can lower your premium, but it means you’ll have to pay more upfront if you file a claim.

Comprehensive Coverage

Comprehensive insurance, often referred to as “other than collision” coverage, protects your vehicle from damage caused by events other than a collision. This can include things like theft, vandalism, fire, natural disasters (hail, floods, earthquakes), and striking an animal. Like collision coverage, comprehensive insurance usually includes a deductible. It’s important to understand what specific perils are covered under your comprehensive policy, as there can be variations between insurers.

Understanding Additional Coverage Options

Beyond the core components of liability and physical damage, a comprehensive auto insurance policy can include a range of optional coverages that provide additional layers of protection. These options can be particularly valuable depending on your individual circumstances, such as your driving habits, the value of your vehicle, and your financial situation.

Protecting Yourself and Your Passengers: Medical Payments and Personal Injury Protection

These coverages are designed to address the medical needs of you and your passengers, regardless of who is at fault in an accident.

Medical Payments (MedPay)

Medical payments coverage is typically a no-fault coverage that pays for medical and funeral expenses for you and your passengers injured in an accident. It can cover expenses such as doctor visits, hospital stays, and ambulance services, even if you have health insurance. MedPay limits are usually relatively low, and it can be a valuable supplement to health insurance, especially for minor injuries where deductibles might otherwise apply.

Personal Injury Protection (PIP)

PIP is a more comprehensive no-fault coverage that is available in some states. In addition to medical expenses, PIP can also cover lost wages, essential services (like household help if you’re unable to perform them due to injuries), and funeral expenses. Like MedPay, PIP pays regardless of fault. The availability and specific benefits of PIP vary significantly by state.

When Others Are Uninsured or Underinsured: Uninsured/Underinsured Motorist Coverage

This is a critical coverage that protects you if you are involved in an accident with a driver who has no insurance or not enough insurance to cover the damages.

Uninsured Motorist (UM) Coverage

UM coverage can help pay for your medical expenses and, in some states, property damage if you’re hit by an uninsured driver. It essentially steps in to cover the damages that the uninsured driver would have been responsible for.

Underinsured Motorist (UIM) Coverage

UIM coverage works similarly to UM coverage but applies when the at-fault driver has insurance, but their liability limits are insufficient to cover the full extent of your damages. For example, if the at-fault driver has $25,000 in bodily injury liability coverage, but your medical bills total $50,000, UIM coverage could help pay for the remaining $25,000.

Additional Protections for Peace of Mind

Beyond the standard and more common optional coverages, several other endorsements can enhance your auto insurance policy.

Roadside Assistance

This coverage typically provides assistance for common roadside emergencies such as towing, flat tire changes, battery jump-starts, fuel delivery, and lockout services. It’s a convenient addition for drivers who frequently travel or want added assurance on the road.

Rental Car Reimbursement

If your vehicle is being repaired due to a covered claim, rental car reimbursement coverage helps pay for a rental car while yours is out of commission. This can be invaluable for maintaining your daily commute or handling essential errands.

Gap Insurance

Gap insurance is particularly relevant for drivers who have financed or leased a new vehicle. If your car is totaled in an accident, insurance typically pays out the actual cash value of the vehicle at the time of the loss. If you owe more on your loan or lease than the car’s depreciated value, gap insurance will cover the difference, preventing you from being saddled with a significant debt for a vehicle you no longer possess.

Choosing the Right Policy for Your Needs

Selecting the appropriate auto insurance policy involves a careful assessment of your individual circumstances and risk tolerance. It’s not a one-size-fits-all solution, and what’s ideal for one driver might not be for another.

Factors Influencing Your Insurance Needs

Several key factors will influence the type and amount of coverage you require:

- State Requirements: As mentioned, every state has minimum liability coverage requirements. You must meet these legal minimums to drive legally.

- Vehicle Value and Age: Newer, more expensive vehicles generally warrant more comprehensive and collision coverage due to their higher replacement cost. Older, less valuable cars might be better served with less extensive physical damage coverage, especially if the cost of premiums outweighs the potential payout.

- Driving Habits and History: A clean driving record with no accidents or violations typically leads to lower premiums. Conversely, a history of accidents, tickets, or DUIs will significantly increase your insurance costs and may limit your coverage options. Frequent drivers or those who commute long distances may also face higher premiums.

- Financial Situation and Risk Tolerance: Consider your ability to absorb financial losses. If you have significant savings and can comfortably afford to pay for minor repairs out-of-pocket, you might choose higher deductibles to lower your premiums. However, if a major accident would pose a significant financial hardship, investing in higher coverage limits and lower deductibles is advisable.

- Loan or Lease Agreements: If you have a car loan or lease, the lender will almost certainly require you to carry collision and comprehensive coverage to protect their investment.

![]()

The Importance of Shopping Around and Comparing Quotes

Once you have a good understanding of the types of coverage available and your specific needs, the next crucial step is to shop around and compare quotes from multiple insurance providers. Premiums can vary significantly between companies for the exact same coverage. Don’t settle for the first quote you receive.

- Get Multiple Quotes: Aim to get quotes from at least three to five different insurance companies, including both national carriers and smaller, regional insurers.

- Be Precise with Information: Ensure you are providing identical information to each insurer when requesting quotes to facilitate an accurate comparison. This includes details about your vehicle, driving history, and desired coverage levels.

- Understand the Policy Details: Beyond the premium price, carefully examine the policy details. Pay attention to deductibles, coverage limits, exclusions, and any additional endorsements. The cheapest policy might not be the best if it lacks crucial coverage.

- Ask About Discounts: Many insurance companies offer a variety of discounts, such as multi-car discounts, safe driver discounts, good student discounts, and discounts for bundling auto and homeowners insurance. Inquire about all available discounts to potentially lower your overall premium.

By taking a systematic approach to understanding your auto insurance options and diligently comparing quotes, you can secure a policy that provides the right balance of protection and affordability, ensuring you’re covered for whatever the road may bring.