The transition to college is a significant milestone, marking not just academic growth but also the burgeoning financial independence of young adults. For many, a credit card becomes a vital tool in navigating this new phase, offering convenience, building credit history, and providing a safety net. However, with a plethora of options available, discerning the “best” credit card for college students requires a nuanced understanding of their unique needs and financial situations. This isn’t about finding a one-size-fits-all solution, but rather identifying cards that offer accessible entry points, reward responsible usage, and minimize potential pitfalls. The ideal college student credit card is a gateway to financial literacy, a tool for managing everyday expenses, and a stepping stone towards a healthy credit future.

Understanding the College Student’s Financial Landscape

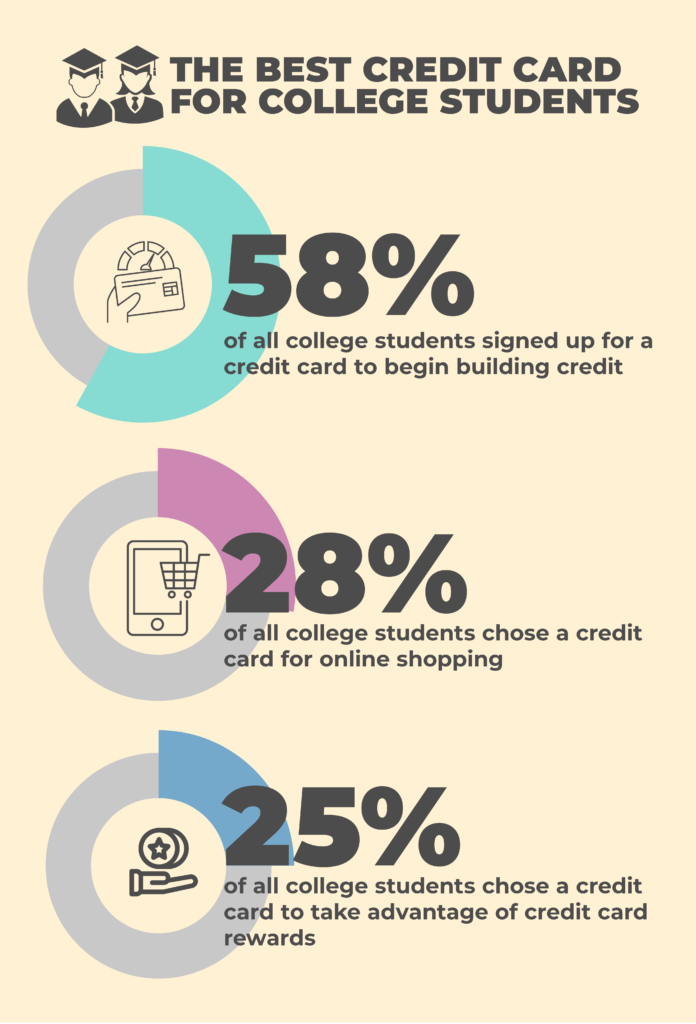

College students often operate with a limited or inconsistent income stream, typically derived from part-time jobs, parental support, or scholarships. This financial reality significantly shapes their credit card needs. The primary goals for this demographic are often to establish a credit history, manage essential expenses like textbooks, groceries, and transportation, and avoid accumulating overwhelming debt. Understanding these constraints is paramount to selecting a credit card that serves as a beneficial tool rather than a financial burden.

The Importance of Building Credit Early

Credit history is a cornerstone of future financial success. Lenders, landlords, and even potential employers often review credit reports to assess an individual’s financial responsibility. For college students, who are just beginning their independent financial journey, establishing a positive credit history early on is incredibly advantageous. Responsible credit card usage – making on-time payments and keeping balances low – can lead to better interest rates on future loans, easier approval for apartments, and a more secure financial footing as they enter the professional world.

Common Financial Needs and Spending Habits

The spending habits of college students are diverse but often center around a few key areas. Textbooks and educational supplies represent a significant, albeit often seasonal, expense. Daily living costs, including groceries, dining out, and personal care items, are ongoing. Transportation, whether public transit passes or gas for a car, also features prominently. Furthermore, students may use credit cards for online purchases, entertainment, and emergency situations. A credit card that aligns with these spending patterns, perhaps by offering rewards on relevant categories, can enhance its utility.

Key Features to Consider for Student Credit Cards

When evaluating credit cards specifically designed for or accessible to college students, certain features stand out as particularly important. These range from the initial accessibility of the card to the ongoing benefits and protections it offers. Prioritizing these features can help students avoid common pitfalls and maximize the advantages of their first credit card.

Low or No Annual Fees

For students, every dollar saved is a dollar that can be put towards education or other essential needs. Annual fees, even if seemingly small, can add up over time and detract from the overall value of a credit card. Therefore, a credit card with a low or, ideally, no annual fee is a crucial consideration. This ensures that the cost of having the card doesn’t outweigh the benefits it provides, making it a more sustainable financial tool throughout their college years.

Accessible Approval Requirements

Many traditional credit cards have stringent approval requirements that can be challenging for college students to meet, especially those with no prior credit history. Student-specific credit cards or secured credit cards are often designed with more lenient approval criteria, making them more accessible. These cards offer a vital entry point for students to begin building credit, often requiring no credit history or a smaller security deposit (in the case of secured cards).

Building Credit Responsibly: Reporting to Major Credit Bureaus

The primary benefit of responsible credit card usage for students is credit building. It is imperative that any credit card considered actively reports payment activity to the three major credit bureaus: Equifax, Experian, and TransUnion. This ensures that on-time payments and responsible account management are reflected on the student’s credit report, positively impacting their credit score over time. Cards that do not report to credit bureaus offer little to no value in terms of credit building.

Rewards Programs Tailored to Student Spending

While not always the primary focus, rewards programs can add significant value to a college student’s credit card. These rewards can take various forms, such as cash back, points, or travel miles. For students, cash back is often the most straightforward and universally useful reward. Cards that offer higher cash back percentages on common student spending categories like groceries, gas, or dining can help offset everyday expenses. Some cards may also offer bonus rewards on online purchases or for streaming services, further aligning with student lifestyles.

Low Initial Interest Rates (APR) and Grace Periods

Interest rates (APR) are a critical factor, especially for students who may occasionally carry a balance. While the goal is always to pay the balance in full each month, unexpected expenses or financial shortfalls can occur. A credit card with a lower introductory APR or a competitive ongoing APR can significantly reduce the cost of carrying a balance. Furthermore, a generous grace period – the time between the end of a billing cycle and the payment due date – provides flexibility and an opportunity to avoid interest charges if payment is made within that window.

Security Features and Fraud Protection

In an increasingly digital world, robust security features are essential. College students, like all consumers, are vulnerable to credit card fraud. Credit cards offering advanced security measures such as EMV chip technology, zero liability for unauthorized charges, and real-time transaction alerts provide peace of mind and protect against financial loss. These features are standard on most reputable cards but are still worth confirming.

Types of Credit Cards Beneficial for College Students

The diverse financial profiles and goals of college students necessitate exploring different types of credit cards. Each category offers distinct advantages that can cater to specific needs, from building credit from scratch to earning rewards on everyday purchases. Understanding these categories helps students make informed decisions based on their current financial situation and future aspirations.

Secured Credit Cards: The Foundation for Building Credit

For students with no credit history or those who have had difficulty obtaining traditional credit, secured credit cards are an excellent starting point. These cards require a cash security deposit, which typically serves as the credit limit. The deposit mitigates risk for the issuer, making approval more likely. By using a secured card responsibly – making payments on time and keeping balances low – students can build a positive credit history that can eventually qualify them for unsecured cards. Many secured cards also offer features like regular credit limit reviews and the potential to graduate to an unsecured account.

Student Credit Cards: Designed for the Academic Journey

Several credit card issuers offer cards specifically branded as “student credit cards.” These are typically unsecured cards with features tailored to the financial realities of college students. They often boast easier approval processes, potentially lower credit limits to prevent overspending, and sometimes offer rewards on common student purchases. While they may not always offer the most lucrative rewards programs, their accessibility and focus on credit building make them a popular choice for many students embarking on their credit journey.

Cash Back and Rewards Credit Cards: Earning on Everyday Spending

Once a student has established some credit history, they may be eligible for cash back or general rewards credit cards. Cash back cards are particularly appealing due to their simplicity and direct financial benefit. Cards offering a flat percentage of cash back on all purchases, or higher percentages on specific categories like groceries, gas, or dining, can help students recoup some of their spending. These rewards can be redeemed as statement credits, direct deposits, or gift cards, effectively reducing their overall expenses. For students who are diligent about paying off their balance each month, these cards can provide tangible savings.

Store or Co-Branded Credit Cards: Niche Benefits

While perhaps less universally applicable than other categories, store or co-branded credit cards can be beneficial if a student is a frequent shopper at a particular retailer or uses a specific service. For example, a student who frequently buys textbooks from a specific bookstore chain might find a co-branded card useful for exclusive discounts or rewards on those purchases. Similarly, a student loyal to a particular airline or hotel chain might consider a co-branded card to earn miles or points towards future travel. The key is to ensure the benefits align with actual spending habits to avoid being locked into potentially less advantageous general terms.

Strategies for Responsible Credit Card Management in College

Acquiring a credit card is only the first step; managing it responsibly is where the true financial education begins. For college students, developing good credit habits early can set a precedent for a lifetime of sound financial decision-making. This involves understanding the terms of the card, diligently tracking spending, and prioritizing on-time payments above all else.

The Golden Rule: Pay Your Balance in Full and On Time

The most crucial advice for any credit card holder, and especially for college students, is to pay the entire balance in full and on time each month. This simple practice ensures that no interest is accrued, making the credit card essentially a free payment tool. It also guarantees positive reporting to credit bureaus, actively building a strong credit score. Setting up automatic payments or calendar reminders can be invaluable in preventing late payments, which can incur hefty fees and negatively impact credit history.

Avoiding the Debt Trap: Understanding Credit Limits and Overspending

Credit cards come with credit limits, which are the maximum amount that can be borrowed. It’s essential for students to understand their credit limit and treat it as a ceiling, not a target. Overspending can quickly lead to accumulating debt, especially if the card has a high APR. Students should aim to keep their credit utilization ratio (the amount of credit used compared to the total available credit) low, ideally below 30%, as this positively impacts their credit score. Regularly reviewing spending through online banking portals or mobile apps can help maintain this discipline.

Monitoring Your Credit Report and Score

As students begin to build credit, it’s important for them to monitor their progress. Free services often allow individuals to check their credit score periodically, and annual credit reports from each of the major bureaus are available for free. Reviewing these reports helps students identify any potential errors, fraudulent activity, or signs of irresponsible usage that need to be addressed. Understanding how their credit score is calculated and what factors influence it empowers them to make informed financial decisions.

Utilizing Card Benefits Wisely: Rewards, Perks, and Protections

Beyond credit building, credit cards often come with a host of benefits that can enhance a student’s life. This includes cash back or points that can be redeemed for savings, travel insurance, purchase protection, extended warranties, or even student-specific discounts. Students should familiarize themselves with their card’s benefits and actively use them to maximize the card’s value. However, it’s crucial that the pursuit of rewards doesn’t lead to overspending. The primary focus should always remain on responsible financial management.

Conclusion: A Stepping Stone to Financial Literacy

Choosing the “best” credit card for a college student is not about finding the most feature-rich or highest-rewarding card on the market. Instead, it’s about selecting a card that serves as a safe, accessible, and educational tool. A card that allows them to establish credit, manage essential expenses, and learn the fundamentals of responsible financial behavior is invaluable. By prioritizing low fees, accessible approval, and features that promote good habits, students can leverage their first credit card not just as a payment method, but as a powerful stepping stone towards financial independence and a secure future. The journey of financial literacy begins with informed choices, and a well-chosen credit card can be a significant catalyst in that journey.