A Health Savings Account (HSA) deduction represents a powerful financial tool for individuals with high-deductible health plans (HDHPs) to manage their healthcare costs. At its core, an HSA deduction is the amount of money you contribute to your HSA that can be subtracted from your taxable income, thereby reducing your overall tax liability. This makes HSAs incredibly attractive for those seeking to proactively save for medical expenses while simultaneously benefiting from tax advantages. Understanding the nuances of these deductions is crucial for maximizing their benefit and ensuring financial well-being in the face of rising healthcare costs.

The Fundamentals of Health Savings Accounts

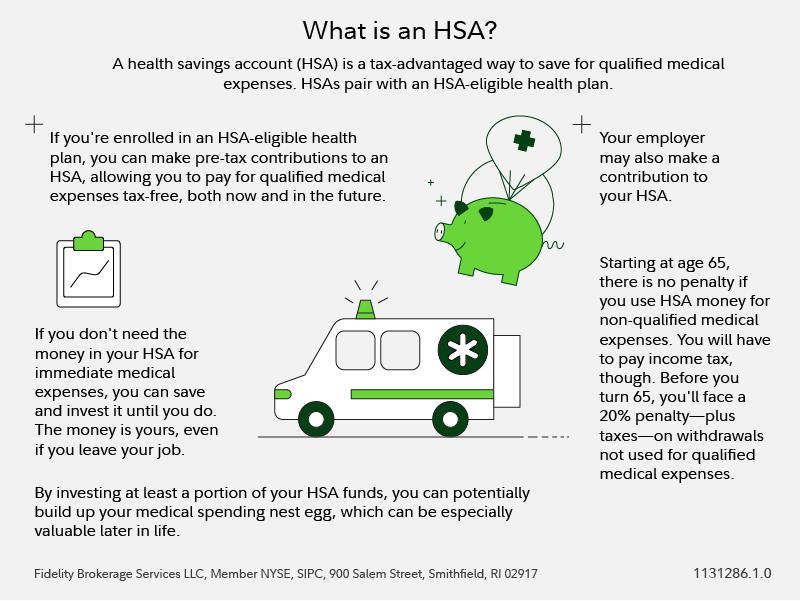

Health Savings Accounts were established by the U.S. Congress in 2003 as part of the Medicare Prescription Drug, Improvement, and Modernization Act. Their primary purpose is to provide individuals enrolled in HDHPs with a tax-advantaged way to save for qualified medical expenses. Unlike traditional savings accounts, HSAs offer a unique triple tax advantage: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are also tax-free. This makes them a compelling option for long-term healthcare financial planning.

Eligibility for Health Savings Accounts

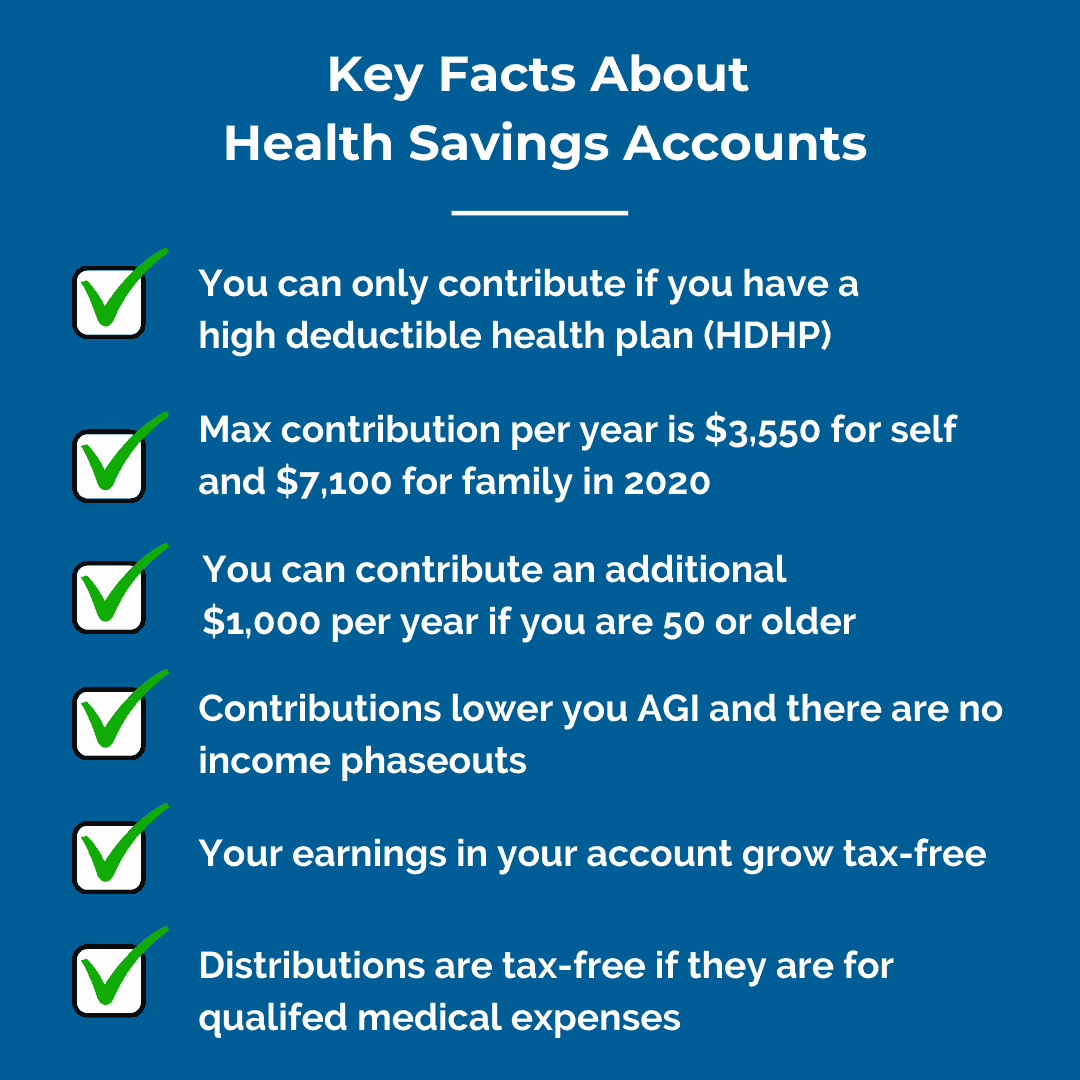

To be eligible to open and contribute to an HSA, individuals must be enrolled in a High-Deductible Health Plan (HDHP). The IRS sets specific criteria for what constitutes an HDHP annually. For 2023, an HDHP is defined as a health plan with a minimum annual deductible of $1,400 for self-only coverage or $2,800 for family coverage. Additionally, the out-of-pocket maximum for an HDHP cannot exceed $7,000 for self-only coverage or $14,000 for family coverage. It’s important to note that individuals cannot be enrolled in Medicare, be claimed as a dependent on someone else’s tax return, or have other health coverage that is not an HDHP to be eligible.

Understanding High-Deductible Health Plans (HDHPs)

HDHPs are characterized by lower monthly premiums compared to traditional health insurance plans, but they come with significantly higher deductibles. This means that individuals are responsible for paying a larger portion of their healthcare costs out-of-pocket before the insurance plan begins to cover expenses. While the initial out-of-pocket burden can seem daunting, HDHPs are designed to incentivize individuals to be more mindful of their healthcare spending and to encourage preventative care. The savings from lower premiums can be directed towards an HSA, creating a financial cushion for the higher deductible.

Contribution Limits for HSAs

The IRS sets annual limits on the amount individuals can contribute to their HSAs. These limits are adjusted periodically for inflation. For 2023, the maximum contribution for self-only coverage is $3,850, and for family coverage, it is $7,750. Individuals aged 55 and older can make an additional “catch-up” contribution of $1,000 per year. These limits apply to the total contributions made by both the individual and their employer if they offer an HSA-compatible plan. It’s essential to track your contributions to ensure you do not exceed these limits, as excess contributions may be subject to taxes and penalties.

The Mechanics of the HSA Deduction

The “HSA deduction” primarily refers to the tax deduction taken on your federal income tax return for the contributions you make to your Health Savings Account. This deduction directly reduces your adjusted gross income (AGI), which can lead to a lower overall tax bill. The IRS allows this deduction for contributions made directly by the account holder, as well as for contributions made by an employer through payroll deductions, although the latter are typically not considered taxable income in the first place.

How to Claim Your HSA Deduction

When you contribute to an HSA, the process for claiming the deduction depends on how the contributions were made. If your employer contributes to your HSA through payroll deductions, these contributions are usually made pre-tax, meaning they are already excluded from your taxable income reported on your W-2 form. You will typically not need to take an additional deduction on your tax return for these employer contributions.

However, if you make contributions to your HSA directly from your bank account, you will claim the deduction on your federal income tax return. This is done by filing IRS Form 8889, “Health Savings Accounts (HSAs),” which is then attached to your Form 1040. Form 8889 requires you to report your HSA contributions, distributions, and any employer contributions. The net result of these calculations will be the amount you can deduct from your taxable income.

Taxable vs. Non-Taxable Contributions

It’s important to distinguish between taxable and non-taxable contributions when considering your HSA deduction. Employer contributions are generally considered non-taxable by definition and reduce your overall taxable income before it’s even calculated. Contributions you make yourself, on the other hand, are tax-deductible. This means that while the money is yours to use, you get to subtract it from your income for tax purposes. The combined effect of pre-tax employer contributions and tax-deductible personal contributions works to significantly lower your tax burden.

Deadlines for HSA Contributions

The deadline for making HSA contributions for a given tax year is typically the tax filing deadline of the following year, excluding extensions. For example, contributions for the 2023 tax year can be made up until April 15, 2024 (or the next business day if April 15 falls on a weekend or holiday). This extended deadline provides flexibility for individuals to make their full allowable contributions after the end of the tax year. It’s crucial to be aware of this deadline to ensure you maximize your tax benefits.

Qualified Medical Expenses and HSA Distributions

The tax-free nature of HSA withdrawals is contingent upon using the funds for “qualified medical expenses.” This is a broad category that encompasses a wide range of healthcare services and products. Understanding what qualifies is essential to avoid unexpected tax liabilities and penalties on non-qualified distributions.

Defining Qualified Medical Expenses

Qualified medical expenses, as defined by the IRS, generally include costs for diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body. This includes a vast array of expenses such as:

- Medical Services: Doctor’s visits, hospital stays, surgical procedures, diagnostic tests, prescription medications, dental care (including orthodontia), vision care (including eyeglasses and contact lenses), and mental health services.

- Medical Supplies: Bandages, crutches, diagnostic devices, therapeutic devices, and other similar items.

- Medical Equipment: Wheelchairs, walkers, and other medically necessary equipment.

- Health Insurance Premiums: In certain limited circumstances, you can use HSA funds to pay for health insurance premiums. This is generally allowed for COBRA continuation coverage, for health insurance purchased after losing unemployment compensation, and for Medicare Part A and Part B premiums (and Medicare Advantage plan premiums). It does not generally include premiums for a non-HDHP or for the portion of premiums paid by your employer.

- Long-Term Care: Premiums paid for qualified long-term care insurance contracts, up to certain limits.

It is crucial to consult IRS Publication 502, “Medical and Dental Expenses,” for a comprehensive and up-to-date list of qualified medical expenses.

Tax Implications of Non-Qualified Distributions

If you withdraw funds from your HSA for expenses that are not considered qualified medical expenses, those distributions will be subject to both ordinary income tax and a 20% penalty tax. This penalty is in addition to the income tax you would have paid if the money had been withdrawn from a regular savings account. The only exception to the 20% penalty is for individuals who have reached age 65, are disabled, or have died. In these cases, the distributions are still taxed as ordinary income but are not subject to the additional 20% penalty. This highlights the importance of carefully tracking your HSA withdrawals and ensuring they are used for legitimate medical needs.

The Rollover and Carryover Feature

One of the most significant advantages of an HSA is its rollover and carryover feature. Unlike Flexible Spending Accounts (FSAs) or Health Reimbursement Arrangements (HRAs), which often have a “use-it-or-lose-it” policy, HSA funds do not expire. Any unspent funds in your HSA automatically roll over to the next year, and your account continues to grow tax-free. This feature allows HSAs to function as a long-term savings vehicle, enabling individuals to accumulate funds for future healthcare needs, including retirement healthcare expenses. This portability and longevity make the HSA a powerful tool for lifelong health financial management.

Maximizing the Benefits of Your HSA Deduction

Understanding the mechanics of the HSA deduction is the first step; maximizing its benefits requires strategic planning and consistent engagement with your account. By taking advantage of all available features and staying informed, individuals can significantly enhance their financial preparedness for healthcare.

Strategic Contribution Strategies

To maximize your HSA deduction, consider contributing the maximum allowable amount each year. If your budget allows, aim to contribute the full annual limit. If you receive an annual bonus or tax refund, consider allocating a portion of it to your HSA before the tax filing deadline. For those with fluctuating income, consider making larger contributions during months with higher income to take full advantage of the deduction. It’s also a good practice to have a portion of your HSA contributions automatically deducted from your paycheck if your employer offers this option, ensuring consistent savings and immediate tax reduction.

Investment Options Within Your HSA

Many HSA providers offer investment options, allowing your savings to grow beyond simple interest. Once your account balance reaches a certain threshold, you can typically invest funds in mutual funds, exchange-traded funds (ETFs), or other securities. This investment feature transforms your HSA from a mere savings account into a powerful investment vehicle for long-term healthcare needs, including retirement. By investing wisely, you can leverage the power of compounding to build a substantial nest egg for future medical expenses, potentially even for long-term care in retirement. It’s important to research investment options carefully and align them with your risk tolerance and financial goals.

The HSA as a Retirement Tool

Beyond immediate healthcare needs, HSAs are increasingly recognized as a valuable retirement savings tool. Because withdrawals for non-medical expenses after age 65 are taxed as ordinary income but are not subject to the 20% penalty, an HSA can function as a supplemental retirement account. Individuals can use their HSA funds for any purpose in retirement, effectively using them as a flexible source of income. This dual purpose – providing for current healthcare needs and supplementing retirement income – makes the HSA an exceptionally versatile financial asset. Planning for how you might use your HSA in retirement, in addition to your other retirement accounts like 401(k)s and IRAs, can lead to a more secure financial future.