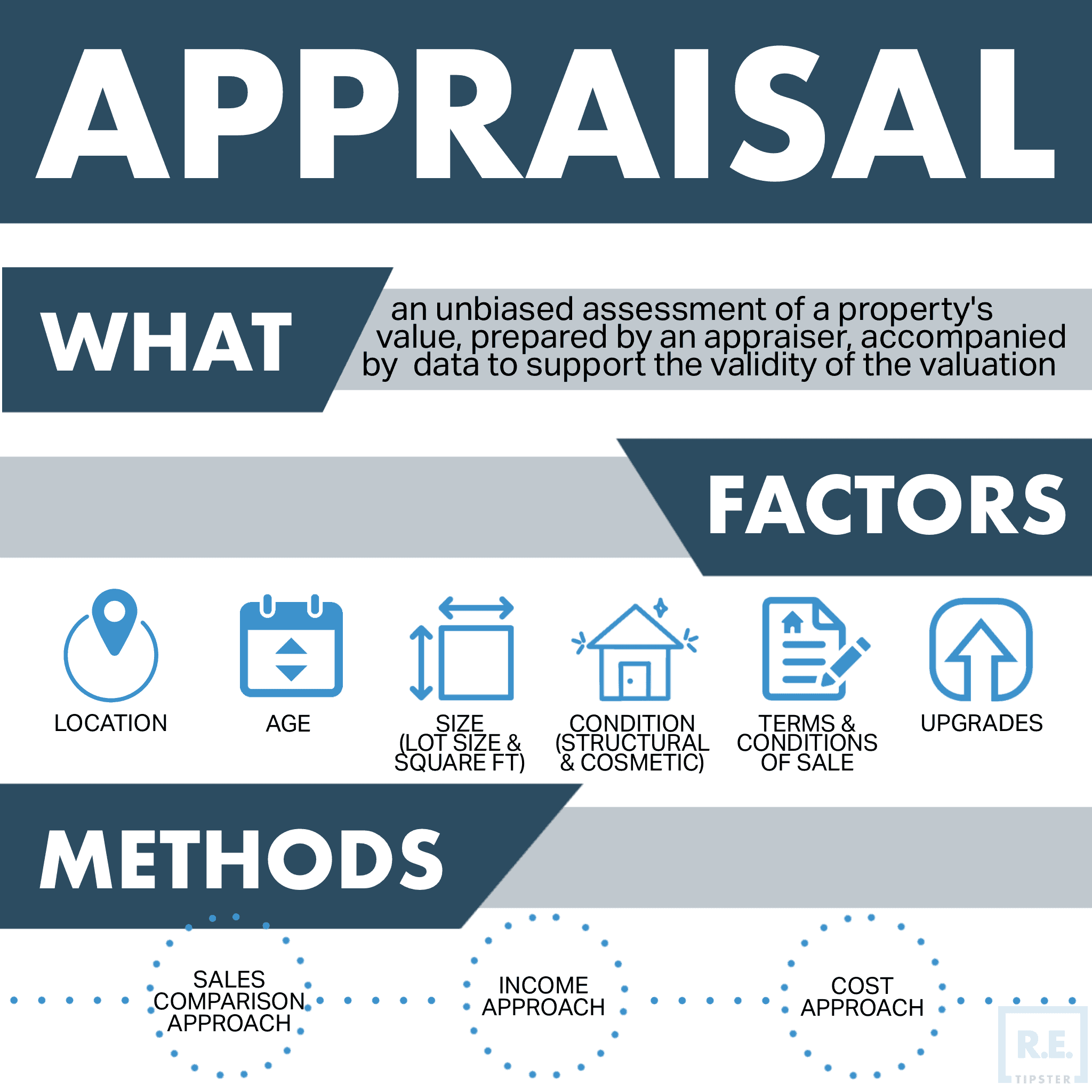

An appraisal in real estate is a critical component of many property transactions and decisions. It’s an unbiased, professional opinion of a property’s value, performed by a licensed appraiser. This process is more than just a quick guess; it’s a detailed and methodical examination that considers numerous factors to arrive at a credible valuation. Understanding what an appraisal entails is crucial for buyers, sellers, lenders, and investors alike, as it directly impacts financial decisions and the overall health of the real estate market.

The Purpose and Importance of a Real Estate Appraisal

At its core, a real estate appraisal serves to establish a property’s fair market value. This value is defined as the most probable price a property should bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeably, and assuming the price is not affected by undue stimulus. The importance of this valuation cannot be overstated, as it underpins numerous aspects of property ownership and exchange.

Protecting Financial Interests

For lenders, an appraisal is a risk mitigation tool. When a buyer seeks a mortgage, the lender needs to ensure that the loan amount is not greater than the property’s actual worth. If the borrower defaults, the lender can recoup their investment by selling the property. An inaccurate appraisal, either too high or too low, can lead to significant financial losses for the lender. Conversely, an accurate appraisal safeguards the borrower by ensuring they are not overpaying for the property or borrowing more than the asset is worth.

Facilitating Transactions

Appraisals are a cornerstone of most real estate transactions, particularly those involving financing. A sale contract often includes a contingency clause that makes the purchase conditional on an acceptable appraisal. If the appraised value comes in lower than the agreed-upon sale price, the buyer may have the option to renegotiate the price, walk away from the deal, or cover the difference with additional funds. This contingency protects buyers from overpaying based on emotion or seller expectations. For sellers, a realistic appraisal helps set an appropriate listing price, attracting serious buyers and avoiding prolonged periods on the market due to an inflated asking price.

Legal and Tax Considerations

Beyond sales, appraisals play a vital role in legal and tax matters. They are frequently used in estate settlements, divorce proceedings, property tax assessments, and eminent domain cases. In these situations, an objective valuation is essential for fair distribution of assets, accurate tax liabilities, and just compensation for property acquisition.

The Appraisal Process: A Comprehensive Examination

The process of conducting a real estate appraisal is rigorous and requires a systematic approach. Appraisers follow established methodologies and adhere to strict ethical guidelines to ensure their valuations are objective and reliable.

Data Collection and Property Inspection

The appraisal begins with the collection of a vast amount of data, both specific to the subject property and the surrounding market. The appraiser will thoroughly inspect the property, examining its physical characteristics in detail. This includes:

- Exterior: The condition of the roof, siding, foundation, landscaping, and any outdoor structures such as garages or sheds.

- Interior: The layout, number of bedrooms and bathrooms, overall condition of finishes (flooring, walls, cabinetry), functionality of plumbing and electrical systems, and evidence of wear and tear or recent upgrades.

- Size and Layout: Measuring the property’s square footage, room dimensions, and overall flow.

- Unique Features: Identifying any special amenities like a swimming pool, a finished basement, or energy-efficient upgrades that might add to the property’s value.

In addition to the physical inspection, the appraiser gathers public records, such as property tax assessments, previous sales history, zoning regulations, and any relevant building permits or liens.

Market Analysis and Comparable Sales (Comps)

A critical element of any appraisal is the analysis of the local real estate market. The appraiser researches recent sales of comparable properties – often referred to as “comps” – within the same or a similar neighborhood. These comps are properties that share key characteristics with the subject property, such as:

- Location: Proximity to the subject property.

- Size: Similar square footage and lot size.

- Age and Condition: Comparable age and level of maintenance or renovation.

- Features: Similar number of bedrooms and bathrooms, garage capacity, and amenities.

The appraiser meticulously adjusts the sale prices of these comparable properties to account for any differences between them and the subject property. For example, if a comparable property has an extra bathroom, its sale price will be adjusted downward to reflect what it would likely sell for without that amenity, making it more comparable to the subject property. This adjustment process allows the appraiser to derive a value indication for the subject property based on what similar homes have recently sold for.

Valuation Methodologies

Appraisers typically employ one or more of three primary valuation approaches, depending on the property type and the available data.

1. The Sales Comparison Approach

This is the most common and often the most reliable approach for appraising residential properties. It directly uses the principle of substitution, which states that a buyer will not pay more for a property than it would cost to acquire a similar property. As discussed, this involves comparing the subject property to similar recently sold properties (comps) and making adjustments for differences. The resulting adjusted sale prices of the comps provide a range of values, from which the appraiser can derive a final opinion of value for the subject property.

2. The Cost Approach

The cost approach is primarily used for newer construction or unique properties where comparable sales are scarce, such as specialized commercial buildings or public facilities. It’s based on the principle of substitution, considering what it would cost to replace the subject property with a new one of similar utility. The calculation involves estimating the current cost to construct a new building, subtracting any accrued depreciation (physical deterioration, functional obsolescence, and economic obsolescence), and then adding the value of the land. This approach is less reliable for older properties where depreciation is difficult to estimate accurately.

3. The Income Capitalization Approach

This approach is used for income-producing properties, such as apartment buildings, office complexes, or retail spaces. It focuses on the potential income the property can generate. The appraiser analyzes the property’s current and potential rental income, operating expenses, and vacancy rates to determine its net operating income (NOI). This NOI is then capitalized (divided by a capitalization rate) to arrive at the property’s market value. The capitalization rate reflects the investor’s required rate of return and the perceived risk associated with the property.

The Appraisal Report: A Formal Document

Once the data has been gathered, inspections completed, and valuations performed, the appraiser compiles their findings into a formal appraisal report. This document is a comprehensive narrative that details the entire appraisal process.

Key Components of an Appraisal Report

A typical appraisal report will include:

- Identification of the Property: Full address, legal description, and parcel number.

- Purpose of the Appraisal: The reason for the valuation (e.g., purchase, refinance, estate settlement).

- Appraiser’s Qualifications: Information about the licensed appraiser, including their credentials and experience.

- Description of the Property: A detailed account of the physical characteristics, improvements, and amenities.

- Market Analysis: An overview of the local real estate market conditions, trends, and economic factors influencing value.

- Scope of Work: A clear outline of the research and analyses performed.

- Valuation Approaches Used: Explanation of which methodologies were applied and why.

- Comparable Sales Data: Details and analysis of the selected comparable properties, including photos and sale prices.

- Highest and Best Use Analysis: An assessment of the most profitable use of the property.

- The Appraisal Conclusion: The appraiser’s final opinion of the property’s value, often presented in a specific format (e.g., Uniform Residential Appraisal Report – URAR for residential properties).

- Supporting Documentation: Maps, photographs of the subject and comparable properties, and relevant public records.

The report is a critical document for all parties involved, providing a transparent and well-supported justification for the determined value.

Who Conducts Appraisals and Who Pays for Them?

The professional who conducts real estate appraisals is known as a licensed or certified appraiser. These individuals are regulated by state licensing boards and must meet specific educational, experience, and examination requirements. Their licensing ensures they possess the necessary knowledge and adhere to ethical standards, such as those outlined by the Appraisal Institute or the Uniform Standards of Professional Appraisal Practice (USPAP).

In most real estate transactions where a mortgage is involved, the borrower (buyer) typically pays for the appraisal as part of their closing costs. The lender orders the appraisal from an independent third-party appraisal management company or directly from an appraiser to ensure objectivity. This fee is non-negotiable and is paid upfront to initiate the appraisal process.

For other purposes, such as estate settlements, divorce proceedings, or property tax appeals, the party initiating the appraisal will bear the cost. This could be an executor of an estate, a party in a divorce case, or a property owner challenging their tax assessment.

Understanding and Challenging an Appraisal

While appraisals are designed to be objective, they are still opinions of value based on the data available and the appraiser’s judgment. It’s important for property owners and potential buyers to understand the appraisal report and what it represents.

If a party believes an appraisal is inaccurate, there are avenues for recourse. The most common scenario is when the appraisal comes in lower than the purchase price, triggering a renegotiation. In such cases, the buyer or their agent can present additional data to the appraiser or the lender that may not have been considered, such as recent comparable sales that were overlooked or evidence of recent renovations that significantly increased value. While appraisers are generally not required to revise their reports without new, substantial evidence, providing such information can sometimes lead to a reconsideration or at least offer a clearer understanding of the valuation.

For tax assessments or legal disputes, formal appraisal review processes or the engagement of a second appraiser may be necessary to contest the original valuation.

In conclusion, a real estate appraisal is a fundamental process that provides a professional, unbiased opinion of a property’s value. It is an indispensable tool for lenders, buyers, sellers, and legal professionals, ensuring transparency, fairness, and informed decision-making in the complex world of real estate.