In the dynamic landscape of real estate transactions, understanding the financial mechanisms that can influence affordability and purchasing power is paramount. Among these, the concept of an “interest rate buydown” stands out as a strategic tool that can significantly impact the long-term cost of homeownership. While the term itself might sound technical, its implications are straightforward and can offer substantial benefits to prospective homebuyers. At its core, an interest rate buydown is a financial arrangement designed to lower the interest rate on a mortgage for a specified period, thereby reducing the monthly mortgage payments for the borrower. This is typically achieved by an upfront payment made by someone other than the borrower, most commonly the seller of the property or a builder, to the lender.

The motivation behind offering an interest rate buydown is multifaceted. For sellers, it can be a powerful incentive to attract buyers, especially in a competitive market or when looking to close a deal more quickly. For builders, it’s a way to stimulate sales and manage inventory, making their new homes more appealing. For buyers, it represents an opportunity to ease into homeownership with lower initial payments, providing breathing room for other expenses or simply making a property more attainable. Understanding the nuances of how these buydowns work, who benefits, and the different types available is crucial for any informed real estate decision.

Understanding the Mechanics of an Interest Rate Buydown

An interest rate buydown is not a permanent reduction of the interest rate for the entire loan term. Instead, it’s a temporary concession that alters the initial interest rate, creating a lower payment for a set duration. This is achieved through an upfront payment that the borrower doesn’t directly contribute. The lender then applies this payment to effectively “buy down” the interest rate, meaning they reduce the rate at which interest accrues on the loan principal for a defined period. The amount of the buydown, the duration it lasts, and the resulting interest rate are all pre-determined and outlined in the mortgage agreement.

The Role of the Upfront Payment

The cornerstone of any interest rate buydown is the upfront payment. This payment is essentially a lump sum transferred from a third party to the mortgage lender. The size of this payment directly correlates with the extent of the interest rate reduction and the duration it is applied. For instance, a larger payment can secure a more significant reduction or a longer period of reduced interest. This payment is a crucial element for understanding the financial transaction, as it represents the cost of achieving the lower monthly payments. It’s important to note that this payment is non-refundable to the party that made it.

How the Reduced Rate is Applied

Once the buydown payment is made, the lender adjusts the borrower’s initial interest rate. This adjustment typically follows a tiered structure. For example, a “2-1 buydown” is a common structure where the interest rate is reduced by 2% in the first year, then by 1% in the second year, before reverting to the original, agreed-upon market interest rate for the remainder of the loan term. Alternatively, a “1-0 buydown” would reduce the interest rate by 1% for the first year, then revert to the market rate. The specific structure of the buydown dictates how the interest rate is applied over time and, consequently, how the monthly payments fluctuate.

The Impact on Monthly Payments

The most tangible benefit of an interest rate buydown for the borrower is the reduction in their monthly mortgage payments during the buydown period. This lower payment can make a significant difference in a household’s budget, freeing up funds for other essential expenses, savings, or investments. For example, with a 2-1 buydown, a borrower might experience a payment that is hundreds of dollars less in the first year compared to what they would pay on a loan with the full interest rate. This can be particularly beneficial for first-time homebuyers who may be stretching their finances to afford a down payment and closing costs.

Types of Interest Rate Buydowns

Interest rate buydowns are not a one-size-fits-all solution. They come in various structures, each offering a different timeline and degree of interest rate reduction. The most common types are distinguished by the number of percentage points by which the interest rate is reduced and the number of years this reduction is effective. Understanding these different types allows buyers and sellers to choose the structure that best aligns with their financial goals and market conditions.

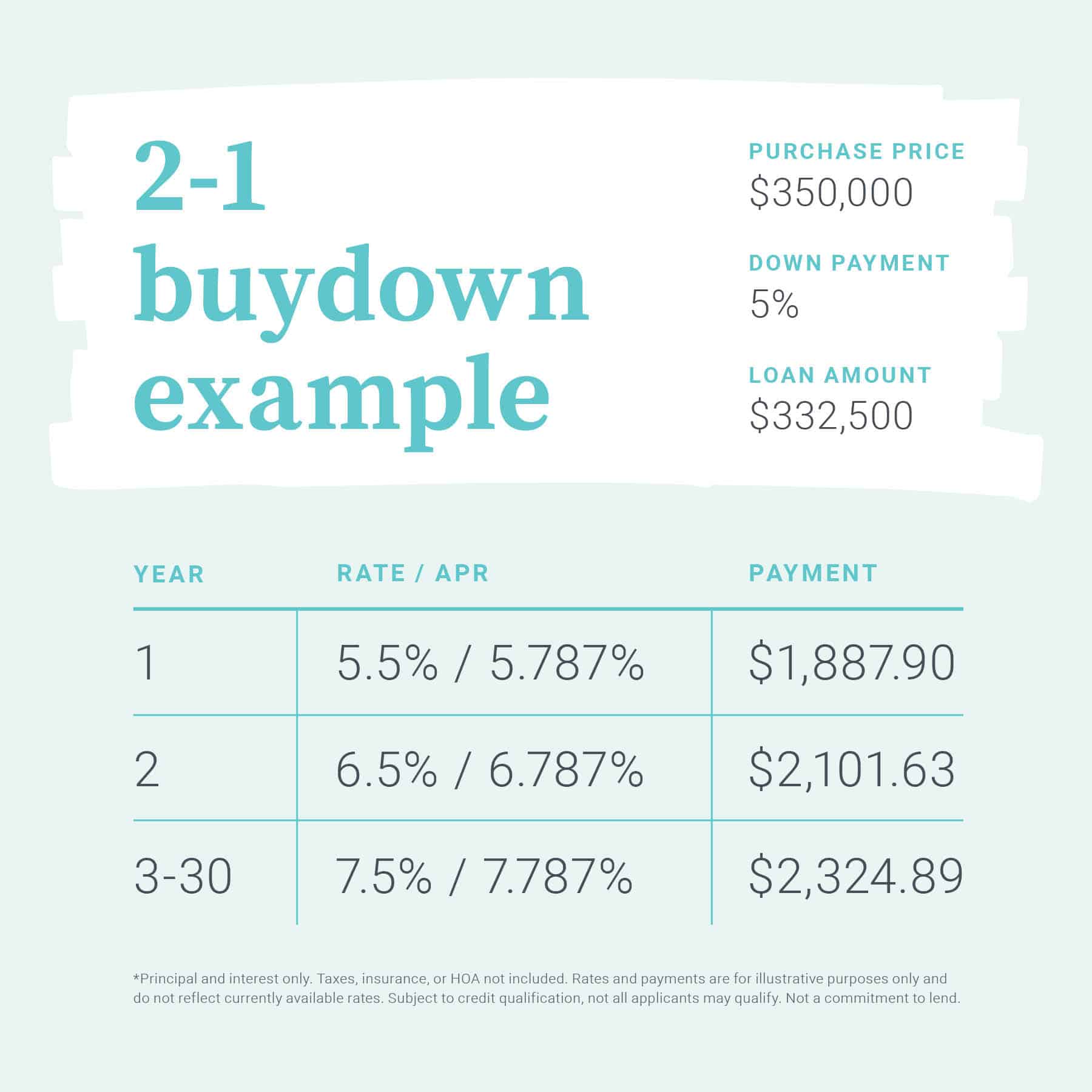

The 2-1 Buydown

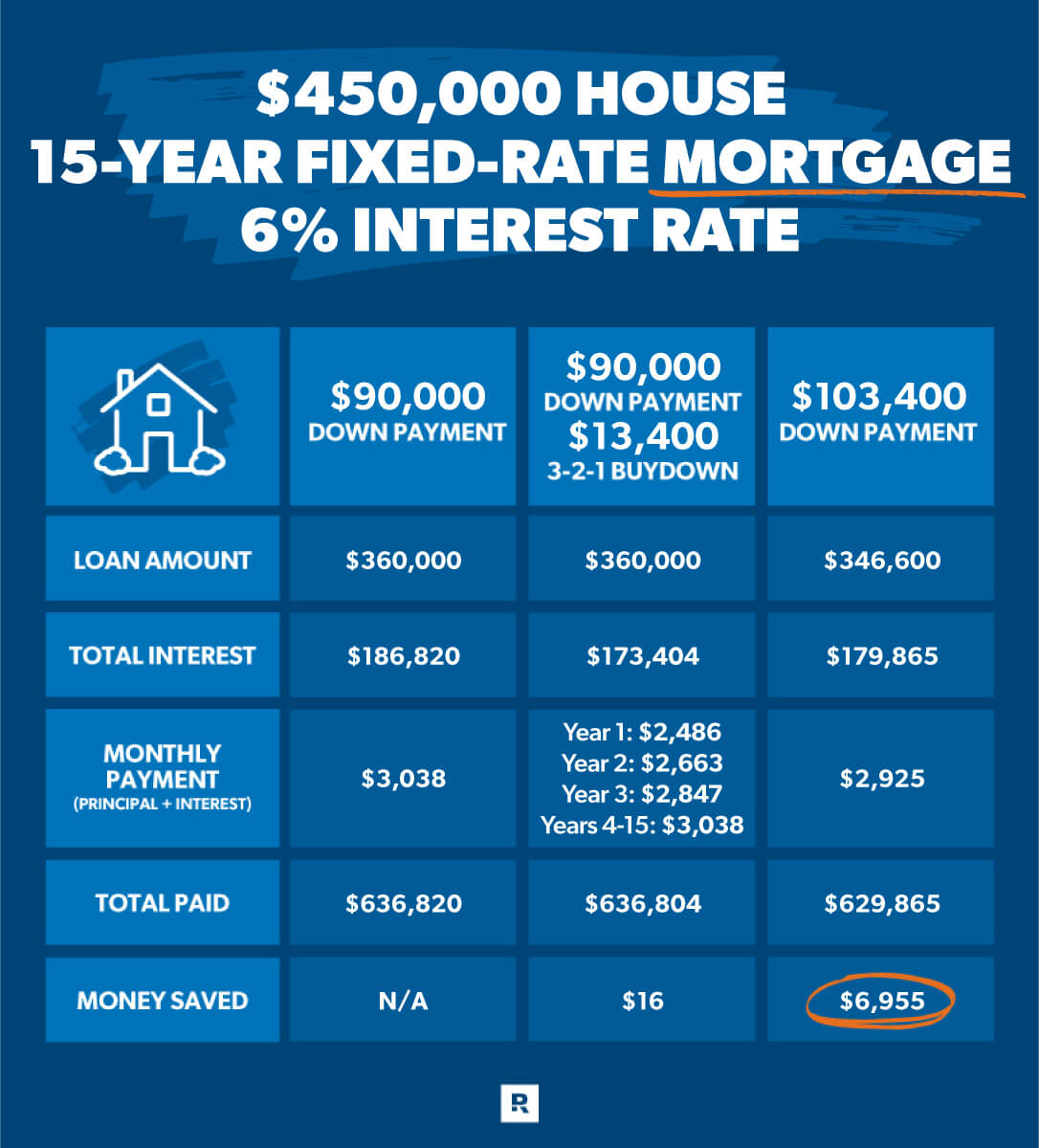

The 2-1 buydown is perhaps the most frequently encountered type of interest rate buydown. In this arrangement, the initial interest rate is reduced by 2 percentage points for the first year of the loan. In the second year, the rate is reduced by 1 percentage point from the note rate. From the third year onwards, the loan reverts to the original note rate, which is the interest rate agreed upon by the borrower and lender at the outset of the loan, before any buydown. This structure provides a substantial initial payment relief, making the first two years of homeownership more manageable financially.

The 1-0 Buydown

A variation on the 2-1 buydown, the 1-0 buydown offers a less aggressive but still beneficial reduction. In this scenario, the interest rate is reduced by 1 percentage point for the first year of the loan. After the first year, the loan reverts to the original note rate. This type of buydown is often utilized when a smaller reduction is sufficient to make the property more attractive or affordable, or when market conditions dictate a less substantial incentive. It still provides a period of lower payments, albeit for a shorter duration and to a lesser degree than a 2-1 buydown.

Permanent vs. Temporary Buydowns

It’s critical to differentiate between temporary and permanent interest rate buydowns. The types discussed above (2-1 and 1-0) are temporary buydowns. They offer a reduced rate for a limited time, after which the loan reverts to the standard interest rate. There is also the concept of a permanent buydown, which is essentially paying discount points at closing to permanently lower the interest rate for the entire life of the loan. While both achieve a lower interest rate, the payment structure and the mechanism of achieving that lower rate are distinct. A permanent buydown involves a higher upfront cost at closing but provides continuous savings.

Benefits and Considerations of Interest Rate Buydowns

While an interest rate buydown can be a compelling financial tool, it’s essential to weigh its advantages against potential drawbacks and to consider the long-term implications. Understanding who benefits most and under what circumstances can help individuals make informed decisions about whether to utilize or offer this incentive.

Advantages for Homebuyers

The primary advantage for homebuyers is the immediate reduction in monthly mortgage payments. This can significantly improve affordability, especially in high-cost housing markets or for individuals with tighter initial budgets. Lower initial payments can also provide a buffer to cover unexpected homeownership expenses, furnishing costs, or other financial commitments that arise shortly after purchasing a home. Furthermore, it can make qualifying for a mortgage easier, as lenders assess affordability based on initial payments. This can be particularly impactful for first-time homebuyers who may be navigating the complexities of the mortgage market for the first time.

Advantages for Sellers and Builders

For sellers, offering an interest rate buydown can be a powerful negotiating tactic and a means to expedite a sale. It can make a property stand out in a crowded market and attract a wider pool of potential buyers by addressing a key concern: affordability. For builders, it’s a strategic sales incentive to move inventory and maintain sales momentum, especially during slower market periods or for properties that have been on the market for an extended time. It allows them to offer a tangible financial benefit without necessarily reducing the list price of the home.

Potential Drawbacks and Considerations

Despite the attractive upfront savings, buyers must be aware of the temporary nature of the reduced rate. The eventual increase in monthly payments can be a shock if not planned for. It’s crucial for borrowers to budget for the higher payments that will commence after the buydown period. Additionally, the cost of the buydown is factored into the overall transaction. While paid by the seller or builder, this cost might indirectly influence the property’s price or other terms of the sale. Buyers should also consider whether the upfront cost of a permanent buydown (discount points) might be more financially beneficial over the long term if they plan to stay in the home for many years. Finally, refinancing the mortgage after the buydown period might be an option, but this incurs additional costs and depends on future interest rate environments.