The journey through higher education is a significant milestone for many, often accompanied by the daunting prospect of financing it. For students and families navigating this complex landscape, understanding financial aid is paramount. Two terms that frequently surface are “EFC” and “FAFSA.” While seemingly interconnected, they represent distinct but crucial elements in the financial aid application process. This article will delve into the nature of the Expected Family Contribution (EFC) and its integral role within the Free Application for Federal Student Aid (FAFSA). We will explore what the EFC signifies, how it’s calculated, and its profound impact on the financial aid package a student may receive.

Understanding the Expected Family Contribution (EFC)

The Expected Family Contribution (EFC) is a metric used by federal student aid programs to determine a student’s eligibility for financial assistance. It represents the amount of money a student’s family is expected to contribute towards their education for the academic year. It’s crucial to understand that the EFC is not a bill or the exact amount a family will pay. Instead, it’s a standardized calculation that aims to assess a family’s financial strength and their capacity to contribute to educational expenses.

The Calculation Methodology: A Look Behind the Numbers

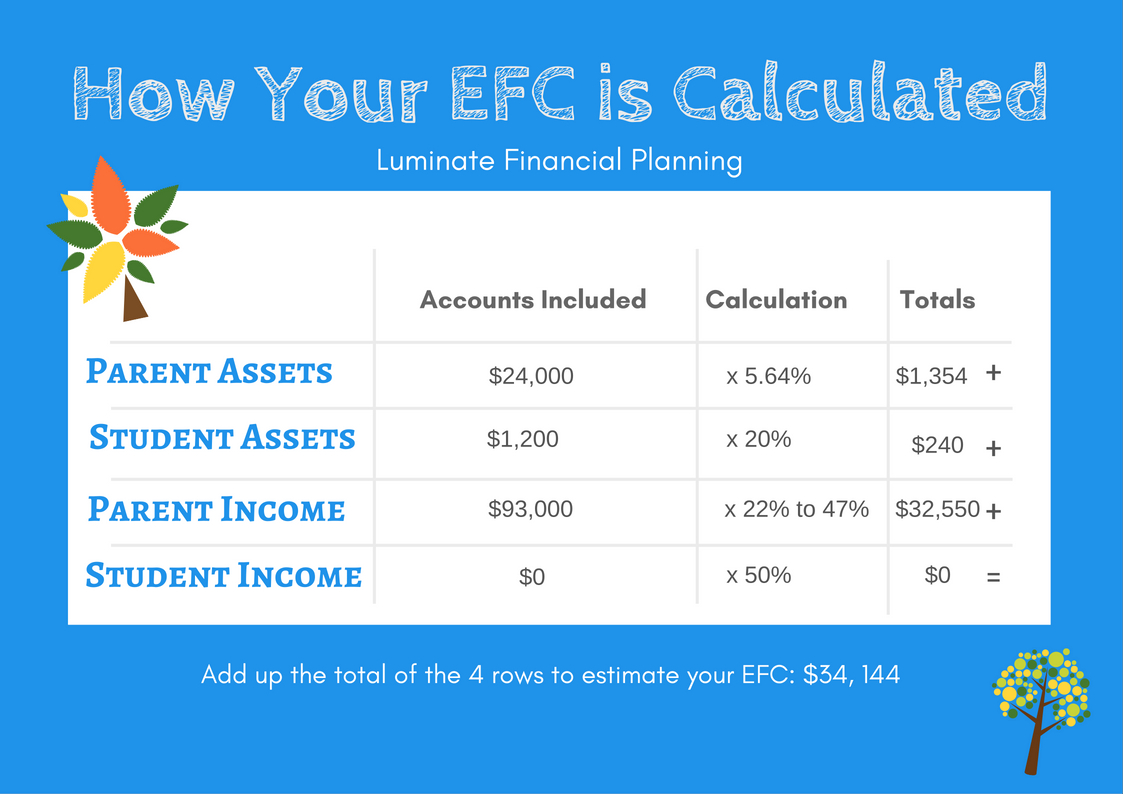

The EFC is not determined by a simple formula. It’s the result of a complex calculation that takes into account a myriad of financial factors reported by the student and their parents on the FAFSA. The Department of Education uses a standardized formula, known as the federal methodology, to arrive at the EFC. This methodology considers a wide range of income and asset information.

Income Considerations: Wages, Investments, and More

The most significant components of the EFC calculation are typically derived from income. This includes:

- Parent and Student Income: This encompasses wages, salaries, tips, and any other taxable income earned by the parents and the student. For dependent students, the parents’ income is the primary driver.

- Untaxed Income: Certain types of income are not subject to federal income tax but are still considered in the EFC calculation. Examples include child support received, veterans’ non-education benefits, and housing, food, and other living allowances paid to members of the military, clergy, and others.

- Adjusted Gross Income (AGI): This is a crucial figure derived from the tax return, representing gross income minus certain deductions.

Asset Evaluation: Savings, Investments, and Real Estate

Beyond income, the federal methodology also scrutinizes a family’s assets. The treatment of assets can differ based on whether the parents or the student own them.

- Parental Assets: These are generally assessed more heavily. They include savings accounts, checking accounts, money market accounts, stocks, bonds, mutual funds, and real estate (excluding the primary home).

- Student Assets: Assets owned directly by the student are also considered, though typically at a higher rate of contribution than parental assets. This includes savings, investments, and other assets in the student’s name.

- Exempt Assets: Certain assets are generally excluded from the EFC calculation. The most significant of these is the family’s primary residence. Other exemptions can include retirement accounts (like 401(k)s and IRAs) and the value of a small business owned and controlled by the family, if it has fewer than 100 full-time employees.

The Role of Household Size and Number in College

The EFC calculation also takes into account household size and the number of family members attending college.

- Household Size: A larger household generally implies more dependents to support, which can lead to a lower EFC.

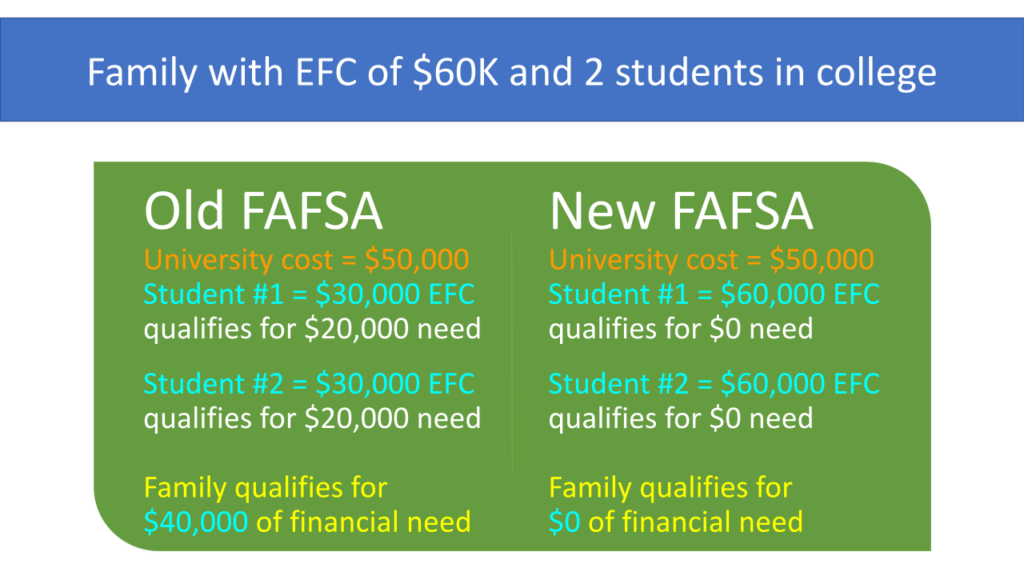

- Number in College: If multiple siblings are attending college simultaneously, the expected contribution from each child’s education expenses is distributed among them, potentially lowering the individual EFC for each student.

Contributions from the Student and Parents

The federal methodology separates the expected contribution into two main parts: the parents’ contribution and the student’s contribution. These are calculated based on their respective incomes and assets, with specific allowances and income protection allowances applied. The sum of these calculated contributions, after certain adjustments, forms the final EFC.

The FAFSA: The Gateway to Financial Aid and EFC Calculation

The FAFSA, or Free Application for Federal Student Aid, is the cornerstone of the financial aid application process for students seeking federal aid in the United States. It is the primary form used by nearly all post-secondary institutions and state aid programs to determine financial need. The FAFSA serves as the data source from which the EFC is calculated.

What Information Does the FAFSA Collect?

To accurately calculate the EFC, the FAFSA requires detailed financial and personal information from both the student and, if the student is a dependent, their parents. The information collected is comprehensive and includes:

- Student and Parent Demographics: This includes names, dates of birth, Social Security numbers, and marital status.

- Household Information: Details about the number of people in the household, the number of dependents, and the number of family members enrolled in college during the academic year.

- Income Information: This is a critical section, requiring details about parents’ and the student’s earnings, wages, tips, and other taxable income from the prior-prior year (e.g., for the 2023-2024 academic year, income from 2021 is used). It also includes untaxed income.

- Asset Information: This section asks about the value of various assets owned by parents and the student, including savings, checking accounts, investments, and real estate.

- Dependency Status: The FAFSA determines whether a student is considered dependent or independent for financial aid purposes. This status significantly impacts whose financial information must be provided.

The Submission and Processing of the FAFSA

Submitting the FAFSA is a critical step. It can be completed online through the official Federal Student Aid website. Once submitted, the application is processed by the Department of Education. During this processing, the federal methodology is applied to the financial data provided.

The Student Aid Report (SAR)

After the FAFSA is processed, students receive a Student Aid Report (SAR). The SAR summarizes the information provided on the FAFSA and, most importantly, displays the calculated EFC. This document is vital as it provides a clear indication of the family’s expected contribution and serves as a basis for financial aid offers from colleges.

The Transition to the SAI (Student Aid Index)

It’s important to note that for the 2024-2025 academic year and beyond, the term “Expected Family Contribution” (EFC) is being replaced by the “Student Aid Index” (SAI). While the underlying principles of assessing a family’s ability to pay remain, the calculation methodology for the SAI is undergoing revisions. The goal is to create a more equitable and streamlined system. While the EFC is the established term for the period prior to this transition, understanding its current role is essential for those applying for aid in the immediate past and present. The SAI will continue the tradition of using a standardized formula to determine a student’s financial aid eligibility, but with updated factors and a new name.

The Impact of EFC on Financial Aid Packages

The EFC, or its successor the SAI, is a pivotal factor in determining the types and amounts of financial aid a student receives. It’s not the sole determinant, but it plays a significant role in the overall financial aid equation.

Calculating Financial Need

The core principle of financial aid is to bridge the gap between the cost of attendance (COA) at an institution and the student’s and family’s expected contribution. The formula for calculating financial need is generally:

Financial Need = Cost of Attendance (COA) – Expected Family Contribution (EFC)

A higher EFC generally means a lower calculated financial need, which could result in a reduced amount of need-based financial aid. Conversely, a lower EFC indicates a higher financial need and potentially a larger financial aid package.

Different Types of Financial Aid

The EFC influences eligibility for various types of financial aid:

- Federal Pell Grants: These are need-based grants awarded to undergraduate students who display exceptional financial need and have an EFC below a certain threshold.

- Federal Supplemental Educational Opportunity Grants (FSEOG): Similar to Pell Grants, these are also need-based and are awarded to students with exceptional financial need.

- Federal Work-Study: This program provides part-time jobs for students with financial need, allowing them to earn money to help pay for educational expenses. Eligibility is often determined by financial need.

- Federal Student Loans: While some federal loans (like PLUS loans) are not strictly need-based, others, such as the Direct Subsidized Loan, are awarded based on financial need. The amount of subsidized loan a student can receive is influenced by their EFC.

- State and Institutional Aid: Most state grant programs and institutional aid offered by colleges and universities are also need-based and utilize the FAFSA and the resulting EFC to determine eligibility.

The EFC as a Starting Point, Not the Final Word

It is crucial to reiterate that the EFC is an expected contribution, not a definitive amount a family must pay. Colleges and universities use the EFC as a benchmark. They then consider their own institutional policies, available funding, and the student’s specific circumstances when constructing a financial aid package. Sometimes, students or families facing extenuating circumstances not fully captured by the FAFSA may be able to appeal their EFC or financial aid package with the financial aid office of the institution.

Implications for College Choice and Planning

The EFC can significantly influence a student’s college choices. Families with a high EFC might find it more challenging to afford institutions with higher costs of attendance, even with financial aid. Conversely, a low EFC can open doors to a wider range of institutions by demonstrating a greater need for financial assistance. Understanding the EFC early in the college planning process allows families to better estimate their potential out-of-pocket costs and explore various financial aid strategies, including scholarships, grants, and financing options.

Navigating the Financial Aid Landscape: Key Takeaways

The EFC and FAFSA are integral components of the financial aid system, designed to assess a family’s ability to contribute to educational costs and to distribute federal aid accordingly. While the terminology is shifting to the Student Aid Index (SAI) for upcoming academic years, the fundamental purpose remains: to ensure that financial barriers do not prevent deserving students from pursuing higher education.

Proactive Engagement and Accurate Information

The accuracy and completeness of the information provided on the FAFSA are paramount. Errors or omissions can lead to an inaccurate EFC calculation, potentially impacting the amount of aid a student receives. Families should approach the FAFSA process with care, gathering all necessary financial documents and honestly reporting their financial situation. Proactive engagement with financial aid offices at prospective institutions can also provide valuable guidance and clarify any uncertainties.

The Importance of the FAFSA Submission Window

Timing is critical. The FAFSA typically opens on October 1st each year for the following academic year. Many states and institutions have their own deadlines for processing financial aid applications, and some aid programs are awarded on a first-come, first-served basis. Therefore, submitting the FAFSA as early as possible is highly recommended to maximize opportunities for various types of aid.

Beyond the EFC: A Holistic View of Financial Aid

While the EFC is a critical number, it’s essential to remember that it’s part of a larger financial aid picture. Students and families should explore all available avenues for financial assistance, including institutional scholarships, private scholarships, and grants from various organizations. A comprehensive approach to financial aid planning, coupled with a thorough understanding of the FAFSA and the EFC/SAI calculation, empowers students to make informed decisions and navigate the path to higher education with greater financial confidence.