The accounts receivable turnover ratio is a critical financial metric that measures how effectively a company collects its outstanding debts from customers. It essentially tells you how many times a company collects its average accounts receivable balance during a specific period, typically a year. This ratio is a key indicator of a business’s liquidity and its ability to manage credit sales and cash flow efficiently. A higher turnover ratio generally signifies that a company is collecting its debts quickly, which is a positive sign for its financial health. Conversely, a lower ratio might suggest issues with credit policies, collection efforts, or the overall economic environment affecting customer payments. Understanding and monitoring this ratio is crucial for businesses of all sizes, from small startups to large corporations, as it directly impacts their working capital and ability to meet short-term obligations.

Understanding the Components of Accounts Receivable Turnover

To fully grasp the significance of the accounts receivable turnover ratio, it’s essential to understand its constituent parts: net credit sales and average accounts receivable. These two figures, when properly calculated, provide the foundation for assessing a company’s credit management prowess.

Net Credit Sales

Net credit sales represent the total revenue generated from sales made on credit during a specific accounting period, minus any sales returns, allowances, and discounts. It’s important to use credit sales specifically because the turnover ratio is concerned with how quickly the company converts credit extended to customers into cash. Cash sales, by their nature, do not involve a period of waiting for payment and therefore do not contribute to accounts receivable.

The calculation of net credit sales typically involves starting with gross credit sales and then deducting:

- Sales Returns and Allowances: This includes the value of goods returned by customers or price reductions granted due to damaged or unsatisfactory merchandise.

- Sales Discounts: These are reductions offered to customers for prompt payment, such as a “2/10, n/30” discount (2% discount if paid within 10 days, otherwise the full amount is due in 30 days). While these discounts reduce the amount of cash received, they are a strategic tool to encourage faster payments and are therefore factored into net credit sales.

Accuracy in calculating net credit sales is paramount. Overstating or understating this figure can lead to a distorted accounts receivable turnover ratio, providing a misleading picture of the company’s performance. Businesses often rely on their accounting software and internal financial reporting systems to track and accurately report net credit sales.

Average Accounts Receivable

Average accounts receivable is the average balance of money owed to the company by its customers over a specific period. This figure is calculated to smooth out fluctuations that can occur in accounts receivable throughout the period. A single accounts receivable balance at the end of a period might not be representative of the typical amount owed.

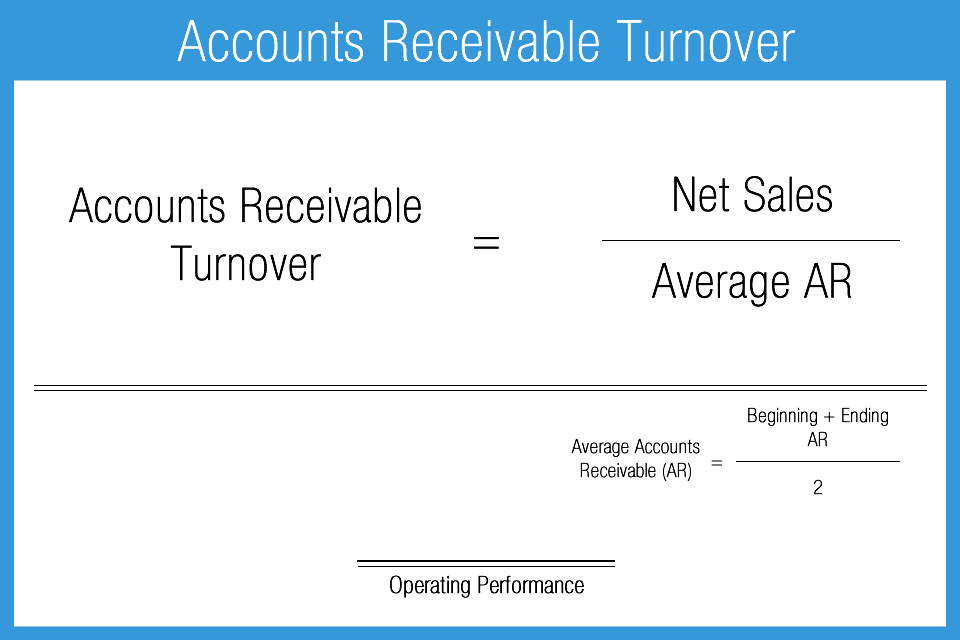

The most common method for calculating average accounts receivable is to take the sum of the accounts receivable balance at the beginning of the period and the accounts receivable balance at the end of the period, and then divide by two:

$$ text{Average Accounts Receivable} = frac{text{Beginning Accounts Receivable} + text{Ending Accounts Receivable}}{2} $$

For more granular analysis or if there are significant seasonal variations in sales and collections, a business might opt to calculate a monthly or quarterly average by summing the accounts receivable balances at the end of each month or quarter and dividing by the number of months or quarters in the period. This provides a more precise representation of the average amount outstanding.

The quality of accounts receivable also plays a role. While the formula uses the gross balance, a more sophisticated analysis might consider the aging of receivables to identify any significant amounts that are past due and potentially uncollectible. However, for the standard turnover ratio calculation, the gross average balance is generally used.

Calculating and Interpreting the Accounts Receivable Turnover Ratio

The core of understanding accounts receivable turnover lies in its calculation and subsequent interpretation. This involves a straightforward formula, but the insights derived from the resulting number are multifaceted and require careful consideration of industry benchmarks and company-specific goals.

The Formula Explained

The accounts receivable turnover ratio is calculated by dividing net credit sales by the average accounts receivable. The formula is as follows:

$$ text{Accounts Receivable Turnover Ratio} = frac{text{Net Credit Sales}}{text{Average Accounts Receivable}} $$

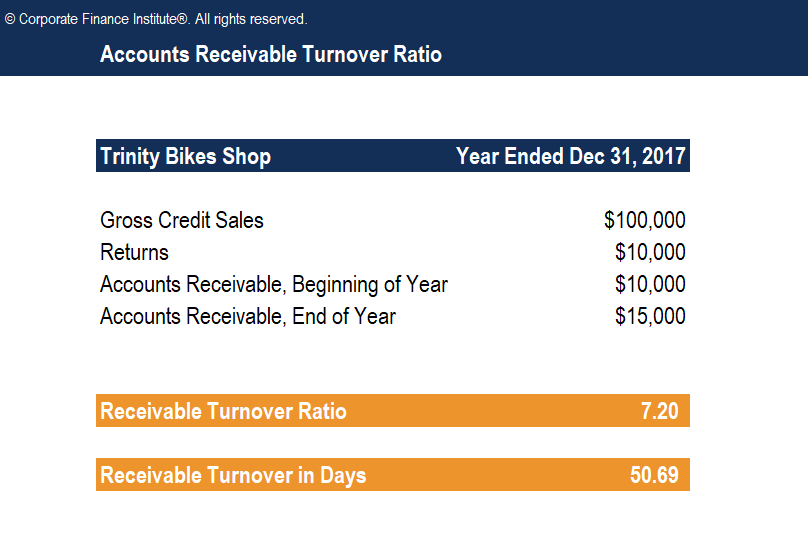

For example, if a company has net credit sales of $1,000,000 for the year and its average accounts receivable balance was $200,000, the accounts receivable turnover ratio would be:

$$ frac{$1,000,000}{$200,000} = 5 $$

This means the company collected its average accounts receivable balance five times during the year.

What the Ratio Indicates

A higher accounts receivable turnover ratio is generally desirable. It suggests that a company is efficiently managing its credit operations and collecting payments from customers promptly. This leads to:

- Improved Cash Flow: Faster collections mean more cash is available to the business, which can be used for operating expenses, investments, debt repayment, or distribution to shareholders.

- Reduced Risk of Bad Debts: When receivables are collected quickly, there’s less time for customers to default on their payments, thus minimizing the risk of uncollectible accounts.

- Lower Financing Costs: With more cash on hand, a company may need to borrow less money, thereby reducing interest expenses.

Conversely, a low accounts receivable turnover ratio can signal several potential problems:

- Ineffective Credit Policies: The company may be extending credit too liberally to customers with poor creditworthiness.

- Weak Collection Efforts: The collection department might not be proactive enough in following up on overdue accounts.

- Poor Sales Management: Customers might be taking advantage of lenient payment terms.

- Economic Downturn: Customers may be experiencing financial difficulties, leading to slower payments.

The Days Sales Outstanding (DSO) Connection

The accounts receivable turnover ratio is closely related to another important metric: Days Sales Outstanding (DSO). DSO measures the average number of days it takes for a company to collect payment after a sale has been made. It’s often considered the inverse of the turnover ratio and provides a more intuitive understanding of the collection period.

The formula for DSO is:

$$ text{Days Sales Outstanding (DSO)} = frac{text{Average Accounts Receivable}}{text{Net Credit Sales / Number of Days in Period}} $$

Or, more simply, using the turnover ratio:

$$ text{Days Sales Outstanding (DSO)} = frac{text{Number of Days in Period}}{text{Accounts Receivable Turnover Ratio}} $$

If the number of days in the period is 365, and the accounts receivable turnover ratio is 5, then the DSO would be:

$$ frac{365}{5} = 73 text{ days} $$

This indicates that, on average, it takes the company 73 days to collect payment from its customers. A lower DSO is generally preferred, as it signifies quicker cash conversion.

Factors Influencing Accounts Receivable Turnover

Several internal and external factors can influence a company’s accounts receivable turnover ratio, making it essential to analyze this metric within its broader operational and economic context. Understanding these drivers allows businesses to identify areas for improvement and make informed strategic decisions.

Internal Factors

Internal factors are those that a company can directly control or influence through its policies and operational efficiency.

- Credit Policies: The generosity and strictness of a company’s credit policies play a significant role. Offering very lenient credit terms (e.g., long payment periods, minimal credit checks) can lead to a higher volume of sales but also a lower turnover ratio as it takes longer to collect. Conversely, stringent credit policies might reduce sales but improve the turnover ratio.

- Collection Procedures: The effectiveness of a company’s collection department is paramount. Proactive follow-ups on overdue invoices, offering payment plans, and implementing efficient billing processes can significantly speed up collections. Delays in sending invoices or a lack of consistent follow-up on late payments will depress the turnover ratio.

- Sales Volume and Terms: The volume of credit sales and the specific payment terms offered to customers directly impact the ratio. A sudden surge in sales, especially with extended payment terms, can temporarily lower the turnover ratio. Similarly, offering attractive discounts for early payment can boost the turnover ratio.

- Invoicing Accuracy and Timeliness: Errors or delays in invoicing can lead to disputes or confusion, slowing down the payment process. Accurate and prompt invoicing is crucial for maintaining a healthy turnover.

- Customer Relationships: Strong customer relationships built on trust and clear communication can encourage prompt payment. Conversely, strained relationships may lead to payment delays.

External Factors

External factors are elements outside of a company’s direct control, often stemming from the broader economic environment or industry-specific conditions.

- Economic Conditions: During economic downturns, customers may experience financial hardship, leading to widespread payment delays. This can cause the accounts receivable turnover ratio to decline across many businesses in affected industries.

- Industry Norms: Different industries have varying norms regarding payment terms and collection periods. For instance, industries with long production cycles or high-value transactions might naturally have longer collection periods than those with quick, repetitive sales. Comparing a company’s turnover ratio to industry averages is therefore essential for accurate benchmarking.

- Competitive Landscape: In highly competitive markets, businesses might feel pressure to offer more lenient credit terms to attract and retain customers, even if it negatively impacts their turnover ratio.

- Seasonal Fluctuations: Some businesses experience seasonal peaks and troughs in sales and collections. This can lead to variations in the accounts receivable balance throughout the year, which is why using an average balance in the calculation is important.

- Regulatory Changes: Changes in regulations related to credit and collections can also influence how quickly businesses can recover outstanding debts.

Strategic Implications and Improving Accounts Receivable Turnover

A well-managed accounts receivable turnover ratio is not just a passive indicator; it’s a lever that can be actively manipulated to enhance a company’s financial performance. By implementing strategic initiatives, businesses can improve their collection efficiency and, consequently, their overall financial health.

Benchmarking and Goal Setting

The first step in strategic improvement is understanding where a company stands relative to its peers and setting realistic targets.

- Industry Analysis: As mentioned earlier, comparing the accounts receivable turnover ratio to industry benchmarks is crucial. A ratio that seems low in isolation might be perfectly acceptable within its specific industry. Conversely, a seemingly high ratio might still have room for improvement if competitors are significantly outperforming.

- Setting Realistic Targets: Based on industry analysis and internal capabilities, businesses should set specific, measurable, achievable, relevant, and time-bound (SMART) goals for improving their turnover ratio. These targets should be communicated to relevant departments, particularly sales and finance.

Enhancing Collection Strategies

Improving the speed and efficiency of collecting outstanding debts is a primary focus for boosting the turnover ratio.

- Optimizing Invoicing Processes: Ensure invoices are accurate, clear, and sent out promptly. Consider implementing electronic invoicing systems for faster delivery and easier customer payment.

- Strengthening Collection Follow-up: Develop a systematic approach to following up on overdue accounts. This might involve tiered communication strategies, starting with polite reminders and escalating to more assertive collection actions as the debt ages.

- Offering Incentives for Early Payment: Reintroduce or refine early payment discount programs. The cost of the discount should be weighed against the benefits of faster cash inflow and reduced collection costs.

- Leveraging Technology: Utilize accounts receivable management software that can automate reminders, track payment statuses, and provide insights into customer payment behavior.

- Credit Risk Assessment: Implement robust credit assessment procedures for new customers to minimize the risk of extending credit to those unlikely to pay. Regularly review the creditworthiness of existing customers.

Impact on Working Capital and Financial Health

An improved accounts receivable turnover ratio has a direct and positive impact on a company’s working capital and overall financial health.

- Increased Liquidity: Faster collection means more cash is available in the business, improving its ability to meet short-term obligations like payroll, supplier payments, and operating expenses without relying heavily on external financing.

- Reduced Need for Financing: With more internal cash flow, the need for short-term loans or lines of credit decreases, leading to lower interest expenses and a stronger balance sheet.

- Enhanced Profitability: While not directly impacting revenue, improved cash flow and reduced financing costs contribute to higher net profits. Furthermore, a more efficient collection process can free up resources that can be deployed in more revenue-generating activities.

- Investor Confidence: A strong and improving accounts receivable turnover ratio can signal to investors and creditors that the company is financially sound and well-managed, potentially leading to better access to capital and more favorable financing terms.

In conclusion, the accounts receivable turnover ratio is a dynamic and vital metric that offers profound insights into a company’s operational efficiency and financial well-being. By understanding its components, accurately calculating and interpreting it, and proactively implementing strategies for improvement, businesses can transform their credit management from a passive administrative function into a powerful driver of profitability and financial stability.