The pursuit of higher education in the United States has long been facilitated by a complex ecosystem of financial aid programs. Among these, the Stafford Loan, particularly its subsidized form, stands out as a cornerstone for many students seeking to finance their academic endeavors. Understanding the nuances of subsidized Stafford loans is crucial for navigating the landscape of educational financing and making informed decisions about one’s financial future. This financial instrument, while seemingly straightforward in its purpose, represents a sophisticated innovation within the broader framework of educational technology and economic accessibility.

The Genesis and Purpose of Stafford Loans

The Stafford Loan program, initially introduced as the “Guaranteed Student Loan Program” in 1965 and later renamed, was a direct response to the growing need for accessible and affordable higher education. Its evolution reflects a persistent societal commitment to empowering individuals through knowledge, recognizing that education is a powerful engine for personal growth and economic prosperity. The program’s design is an example of technological innovation applied to social good, creating a system that bridges the gap between academic aspirations and financial realities for millions.

Historical Context and Evolution

Before the advent of federal student loan programs, financing a college education was a significant hurdle for many families. The high cost of tuition, coupled with limited access to private credit, often meant that pursuing higher education was a privilege rather than an opportunity available to all. The Stafford Loan program emerged as a pivotal intervention, aiming to democratize access to education by providing federal backing and favorable terms. The initial iterations focused on guaranteeing loans made by private lenders, mitigating risk for these institutions and thus encouraging them to lend to students. Over time, the program has undergone numerous reforms, including the transition to direct lending by the federal government, streamlining the process and increasing government control over loan terms and conditions. This evolution showcases a continuous effort to adapt and improve the financial infrastructure supporting education, demonstrating a proactive approach to addressing societal needs through policy and programmatic innovation.

Core Objectives and Target Audience

The fundamental objective of the Stafford Loan program is to ensure that financial constraints do not prevent deserving students from obtaining a college education. This is particularly true for subsidized Stafford loans, which are specifically designed to assist students demonstrating financial need. The program targets undergraduate, graduate, and professional students enrolled in eligible post-secondary institutions. By offering loans with more favorable terms than those typically available in the private market, the federal government aims to:

- Increase Access: Lowering financial barriers to entry for higher education.

- Promote Equity: Providing opportunities to students from diverse socioeconomic backgrounds.

- Support Economic Mobility: Enabling individuals to acquire skills and knowledge that lead to better employment prospects and higher earning potential.

The success of the Stafford Loan program is, in essence, a testament to the power of well-designed financial systems and their capacity to foster societal progress. It is a prime example of how innovation in financial technology can have a profound and lasting impact on individual lives and the broader economy.

Understanding Subsidized Stafford Loans

The key differentiator of a subsidized Stafford loan lies in its treatment of interest during the period when a student is enrolled in school at least half-time, during the grace period after leaving school, and during authorized deferment periods. This “subsidy” provided by the federal government significantly reduces the overall cost of borrowing for students, making it a more attractive and accessible option for those who qualify.

The Mechanism of Interest Subsidy

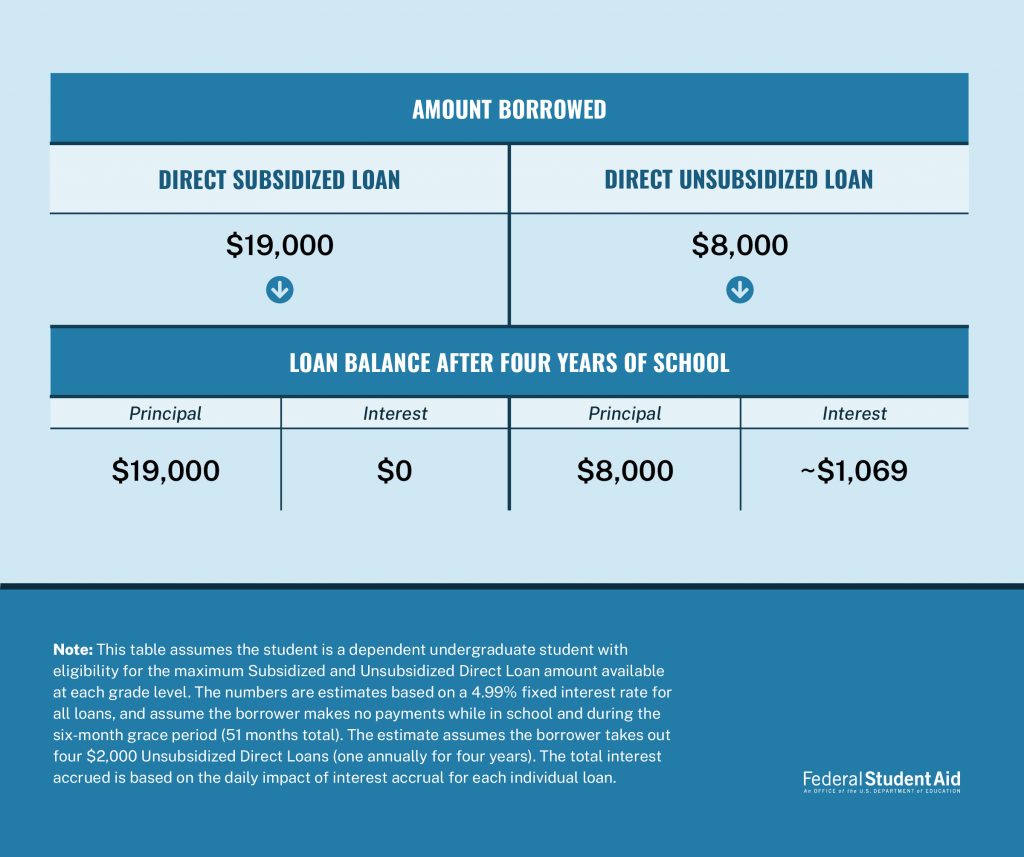

Unlike unsubsidized Stafford loans, where interest accrues from the moment the loan is disbursed, subsidized Stafford loans come with a crucial benefit: the U.S. Department of Education pays the interest on the loan while the student is in school at least half-time, during the grace period (typically six months after a student graduates, leaves school, or drops below half-time enrollment), and during periods of authorized deferment. This means that the principal loan amount does not increase during these times.

This interest subsidy is a significant financial advantage. It prevents the loan balance from ballooning due to accumulated interest before the borrower even begins their repayment period. This feature directly addresses the affordability challenge, ensuring that students graduate with a manageable debt burden that is closer to the original amount they borrowed. This deliberate design is a key innovation in making higher education financing more equitable.

Eligibility Criteria and Financial Need

Eligibility for a subsidized Stafford loan is determined by two primary factors: financial need and enrollment status. Unlike unsubsidized loans, which are available to most students regardless of need, subsidized loans require students to demonstrate financial need as determined by the Free Application for Federal Student Aid (FAFSA). The FAFSA collects detailed information about a student’s and their family’s financial circumstances, including income, assets, and household size. This data is then used to calculate an Expected Family Contribution (EFC) or Student Aid Index (SAI), which helps financial aid offices determine the student’s eligibility for various forms of aid, including subsidized Stafford loans.

Meeting the threshold of financial need is paramount for securing this type of loan. Furthermore, students must be enrolled at least half-time at an eligible institution to qualify and to benefit from the interest subsidy. This ensures that the funds are being used for active academic pursuit, aligning with the program’s core mission. The systematic assessment of financial need through a standardized application process (FAFSA) is itself a form of innovation, creating a transparent and equitable system for distributing federal aid.

Key Distinctions and Repayment Considerations

While both subsidized and unsubsidized Stafford loans are federal education loans, their differences in interest accrual and eligibility lead to distinct repayment profiles. Understanding these distinctions is vital for effective financial planning. The technological infrastructure supporting loan origination, servicing, and repayment is a critical component of this system, enabling seamless management of these diverse loan types.

Comparing Subsidized vs. Unsubsidized Stafford Loans

The primary difference, as highlighted, is the federal government’s payment of interest on subsidized loans during in-school periods, grace periods, and deferments. For unsubsidized Stafford loans, interest accrues from the date of disbursement and is added to the principal balance. This means that an unsubsidized loan will typically have a higher total repayment amount than a subsidized loan of the same principal amount, even if the interest rates are identical.

Both loan types share some common features:

- Federal Backing: Both are federal student loans, offering borrower protections and repayment options not typically found in private loans.

- Fixed Interest Rates: Historically, Stafford loans have featured fixed interest rates, providing predictability for borrowers.

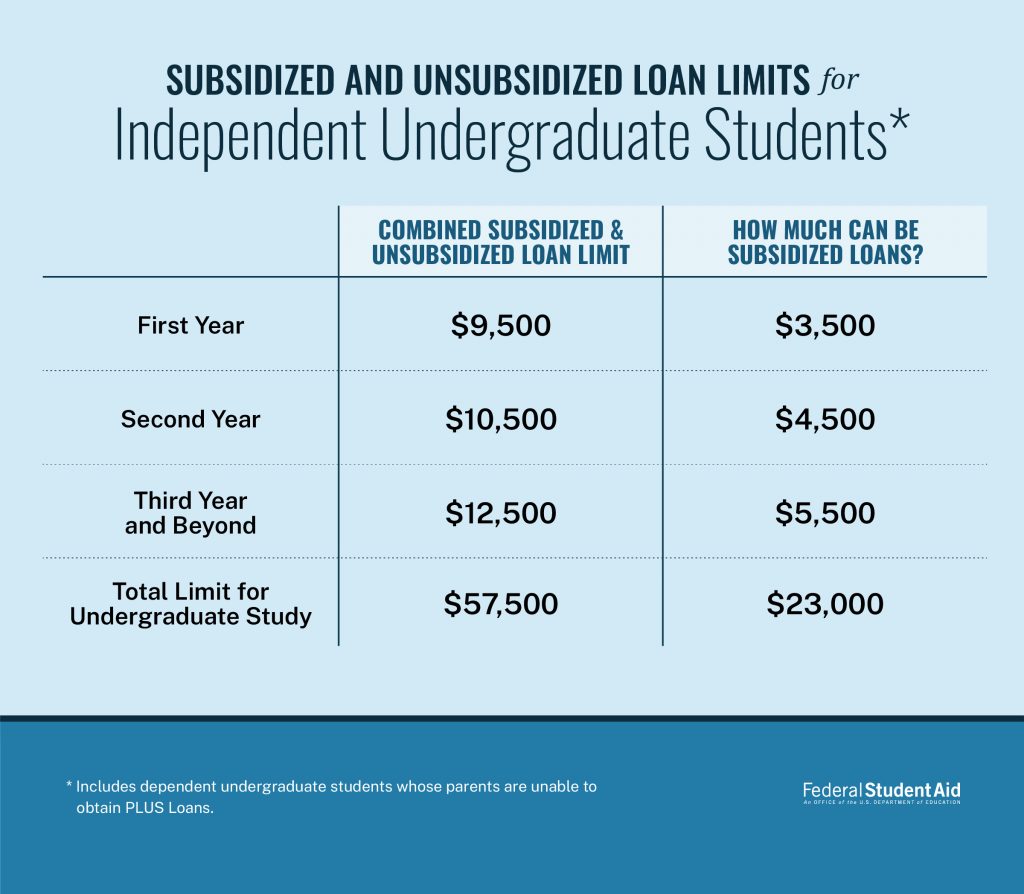

- Loan Limits: There are annual and aggregate limits on the amount students can borrow through Stafford loans, varying based on the student’s academic level and dependency status.

The existence of both subsidized and unsubsidized options within the same program offers flexibility, allowing students to access federal funding based on their individual financial circumstances and needs. This tiered approach is a sophisticated design choice within the financial aid technology framework.

Repayment Plans and Borrower Protections

Once a student leaves school or drops below half-time enrollment, the grace period ends, and repayment of both subsidized and unsubsidized Stafford loans begins. The federal government offers a variety of repayment plans designed to make managing loan debt more manageable. These plans often include:

- Standard Repayment Plan: Fixed monthly payments for up to 10 years.

- Graduated Repayment Plan: Payments start lower and gradually increase over time.

- Income-Driven Repayment (IDR) Plans: Payments are based on a percentage of the borrower’s discretionary income. These plans are particularly innovative in their ability to adapt to a borrower’s financial situation, offering a safety net and making debt repayment more sustainable.

In addition to flexible repayment options, federal Stafford loans come with robust borrower protections. These include:

- Deferment and Forbearance: Options to temporarily postpone or reduce loan payments under certain circumstances (e.g., unemployment, economic hardship).

- Cancellation and Discharge: In specific situations, such as public service employment or total and permanent disability, borrowers may qualify for loan cancellation or discharge.

The technological platforms that manage these loans are critical for administering these complex repayment plans and borrower protections. They allow for real-time tracking of loan statuses, automated calculations for IDR plans, and the efficient processing of deferment and cancellation requests. This sophisticated back-end infrastructure is a key element of the “innovation” aspect of the Stafford Loan program, ensuring its effective and equitable operation.

The Impact and Future of Subsidized Stafford Loans

The subsidized Stafford loan program has profoundly impacted higher education access and student financial well-being. As a cornerstone of federal financial aid, it has enabled millions to pursue their academic goals, contributing to a more educated workforce and a more dynamic economy. However, like many financial systems, it is subject to ongoing evolution and debate concerning its effectiveness and future direction.

Contribution to Educational Access and Economic Mobility

The subsidized Stafford loan has been instrumental in widening the doors of opportunity for countless individuals. By absorbing the cost of interest during crucial periods of a student’s life, it significantly reduces the financial burden, making higher education a more attainable goal for those who might otherwise be excluded. This accessibility is not merely about getting a degree; it is about fostering upward economic mobility. Graduates equipped with higher education are, on average, more likely to secure well-paying jobs, contribute more significantly to the tax base, and experience greater financial stability throughout their lives. The program, therefore, represents a direct investment in human capital and a potent tool for reducing socioeconomic disparities.

Ongoing Debates and Potential Reforms

Despite its successes, the subsidized Stafford loan program, and federal student aid in general, remain subjects of ongoing public and policy discussions. Debates often revolve around:

- Loan Limits: Whether current loan limits are sufficient to cover the rising cost of tuition.

- Interest Rates: The fairness and competitiveness of federal loan interest rates compared to market rates.

- Loan Forgiveness Programs: The efficacy and equity of programs like Public Service Loan Forgiveness (PSLF) and broader proposals for student loan debt cancellation.

- Simplification of Aid Processes: Efforts to streamline the FAFSA and other application processes to make financial aid more accessible and understandable.

Future reforms may focus on further enhancing the “tech” aspect of financial aid, leveraging data analytics and digital platforms to provide more personalized guidance to students, improve loan servicing, and potentially introduce new innovative financing models. The goal is to continuously refine this critical financial technology to better serve students and society. The subsidized Stafford loan, as a foundational element, will likely continue to evolve, adapting to changing economic conditions and societal expectations, ensuring that education remains an attainable dream for future generations.