Understanding the intricacies of higher education financing is paramount for students and families navigating the complex landscape of college costs. Among the various financial aid options available, federal student loans play a significant role. Within this category, Federal Direct Subsidized Loans stand out as a particularly beneficial resource, offering students a way to finance their education with favorable terms. This article delves into the core aspects of Federal Direct Subsidized Loans, demystifying their purpose, eligibility, application process, and repayment, providing a comprehensive guide for prospective borrowers.

Understanding the Fundamentals of Federal Direct Subsidized Loans

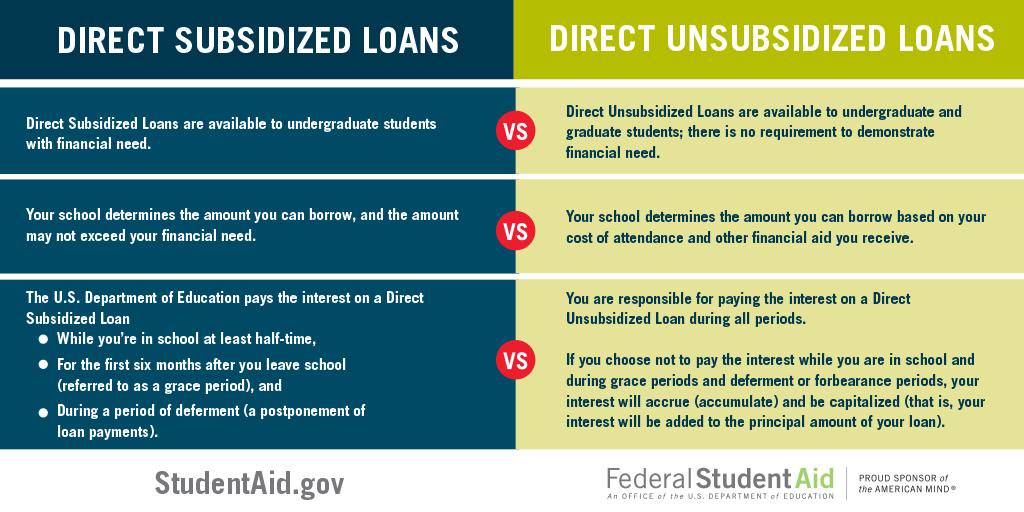

Federal Direct Subsidized Loans, often simply referred to as “subsidized loans,” are a cornerstone of the U.S. Department of Education’s federal student loan program. Their primary distinction lies in the fact that the federal government pays the interest on these loans while the student is enrolled in school at least half-time, during the grace period, and during periods of authorized deferment. This “subsidy” of interest is a critical feature that significantly reduces the overall cost of borrowing for eligible students.

Who is Eligible for a Subsidized Loan?

Eligibility for a Federal Direct Subsidized Loan is primarily determined by financial need. This means that students must demonstrate a significant need for financial assistance to cover their educational expenses as calculated by the Free Application for Federal Student Aid (FAFSA).

Financial Need Assessment

The FAFSA is the gateway to all federal student aid, including subsidized loans. When students complete the FAFSA, they provide information about their family’s financial circumstances, including income, assets, and household size. The Department of Education uses this information to calculate the Expected Family Contribution (EFC), which represents the amount a family is expected to contribute towards a student’s education. The difference between the total cost of attendance at an institution (including tuition, fees, room, board, books, and personal expenses) and the EFC is the student’s calculated financial need. Students who demonstrate financial need are generally eligible for subsidized loans.

Enrollment Status and Academic Progress

Beyond financial need, borrowers must also meet general federal student aid eligibility requirements. This includes being a U.S. citizen or eligible non-citizen, having a high school diploma or GED, and making satisfactory academic progress (SAP) as defined by the institution. Furthermore, to receive disbursements of subsidized loans, students must be enrolled at least half-time in an eligible degree or certificate program at a participating school.

Loan Limits and Disbursement

The amount a student can borrow through a Federal Direct Subsidized Loan is subject to annual and aggregate limits set by the federal government. These limits vary based on the student’s academic level (undergraduate or graduate) and whether they are claimed as a dependent on their parents’ tax returns.

Annual and Aggregate Borrowing Limits

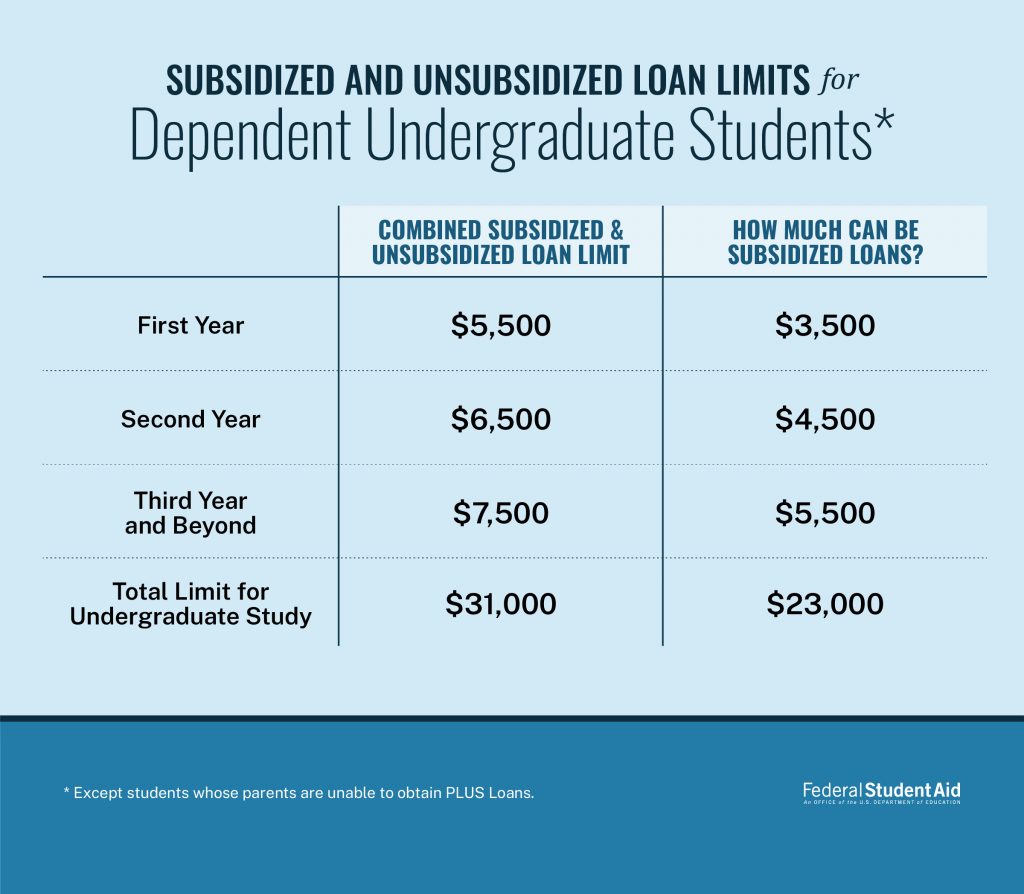

For undergraduate students, annual limits typically range from $3,500 for first-year students to $5,500 for third-year and beyond. Graduate and professional students are generally not eligible for subsidized loans, though there are exceptions for certain health professions. The aggregate limit for undergraduate subsidized loans is $23,000. These limits are designed to ensure that students borrow only what they truly need for their education, minimizing excessive debt.

The Disbursement Process

Once a student’s eligibility is confirmed and they have accepted the loan amount, the funds are disbursed directly to the school. The school first applies the loan funds to the student’s tuition, fees, and other institutional charges. Any remaining funds are then provided to the student for living expenses, books, and other educational costs. Disbursement typically occurs in installments, often at the beginning of each academic term or semester.

The Key Advantages of Federal Direct Subsidized Loans

The primary appeal of Federal Direct Subsidized Loans lies in their borrower-friendly features, particularly the interest subsidy and predictable repayment terms. These advantages distinguish them from other forms of borrowing and can lead to substantial savings over the life of the loan.

Interest Subsidy: A Significant Cost Saver

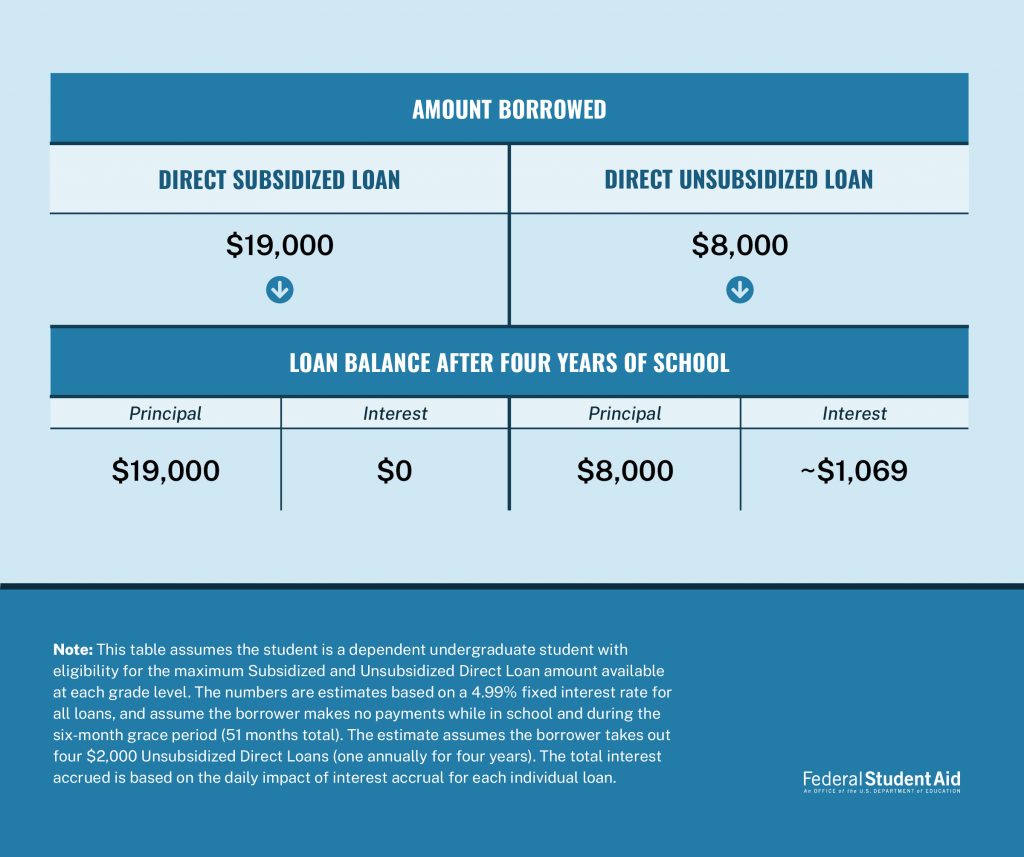

The most defining characteristic of a subsidized loan is the federal government’s commitment to paying the interest that accrues during specific periods. This means that the principal amount of the loan does not increase during these times, which can significantly reduce the total amount repaid.

Interest Accrual During In-School and Grace Periods

Interest does not accrue on subsidized loans while the borrower is enrolled at least half-time in school. Additionally, interest is not charged during the six-month grace period that typically follows a student’s graduation, withdrawal, or dropping below half-time enrollment. This grace period allows borrowers time to secure employment and plan for repayment without the added burden of accumulating interest.

Deferment Periods and Interest Payments

In certain circumstances, borrowers may be eligible for deferment, which allows them to postpone loan payments. During authorized deferment periods, such as for graduate studies, economic hardship, or military service, the federal government continues to pay the interest on subsidized loans. This protection is invaluable for borrowers facing financial challenges or pursuing further education.

Fixed Interest Rates and Predictable Repayment

Federal Direct Subsidized Loans offer fixed interest rates, meaning the rate remains the same for the life of the loan. This provides predictability and protection against rising interest rates that can affect private loans. Once repayment begins, borrowers have access to various repayment plans designed to make managing their debt more manageable.

Fixed Interest Rates for Stability

The fixed interest rate on subsidized loans is a significant advantage, particularly in an environment where interest rates can fluctuate. It allows borrowers to accurately forecast their future monthly payments, making financial planning much simpler. This stability is a stark contrast to the variable rates that can be found with some private student loans, which can lead to unexpected increases in monthly payments.

Flexible Repayment Options

Upon entering repayment, borrowers can choose from several repayment plans, including standard, graduated, and income-driven repayment (IDR) options. Income-driven repayment plans, in particular, are designed to keep monthly payments affordable based on the borrower’s income and family size, with potential for loan forgiveness after 20-25 years of qualifying payments. This flexibility is crucial for borrowers entering careers with potentially lower starting salaries.

The Application and Repayment Process for Subsidized Loans

Securing a Federal Direct Subsidized Loan involves a straightforward application process, primarily centered around the FAFSA. Once the loan is disbursed and the student leaves school, the repayment process begins, offering various strategies for managing the debt.

Applying for a Subsidized Loan

The journey to obtaining a Federal Direct Subsidized Loan begins with the FAFSA. This application serves as the central hub for all federal student aid.

Completing the FAFSA

Students must complete and submit the FAFSA annually, typically starting on October 1st for the following academic year. Accurate and timely submission is crucial, as it determines eligibility for a wide range of federal aid, including Pell Grants, work-study programs, and federal student loans. Schools use the FAFSA information to create a financial aid package tailored to each student’s needs.

Entrance Counseling and the Master Promissory Note (MPN)

Before receiving their first disbursement of federal student loans, undergraduate students are required to complete an Entrance Counseling session. This session provides essential information about loan obligations, repayment responsibilities, and the implications of borrowing. Following Entrance Counseling, borrowers must sign a Master Promissory Note (MPN). The MPN is a legally binding document in which the borrower promises to repay the loan according to its terms and conditions. It can be used for multiple loan disbursements throughout a student’s academic career.

Understanding Loan Repayment

The repayment period for Federal Direct Subsidized Loans typically begins six months after a student graduates, withdraws from school, or drops below half-time enrollment. During this grace period, borrowers can prepare for their repayment obligations without interest accruing.

Grace Period and Repayment Commencement

The six-month grace period is a critical window for borrowers to adjust to life after college. It allows time to find employment, explore repayment options, and begin budgeting for loan payments. Once the grace period ends, borrowers will receive notifications from their loan servicer, and their regular monthly payments will commence.

Exploring Repayment Plans and Strategies

Borrowers have a variety of repayment plans to choose from, each with its own structure and benefits. The standard repayment plan involves fixed monthly payments over a period of up to 10 years. Graduated repayment plans start with lower payments that increase over time. Income-driven repayment (IDR) plans, as previously mentioned, are particularly beneficial for borrowers with lower incomes, as they cap monthly payments at a percentage of discretionary income. Borrowers are encouraged to explore all available options to find a plan that best suits their financial situation. Making timely payments and understanding one’s loan obligations are crucial for maintaining good credit and avoiding default.