The current ratio is a fundamental financial metric that offers a snapshot of a company’s short-term financial health and its ability to meet its immediate obligations. In essence, it measures a company’s liquidity, which is its capacity to convert assets into cash to pay off its short-term debts and liabilities. For investors, creditors, and management, understanding what the current ratio indicates is crucial for making informed decisions about a company’s operational efficiency, financial stability, and potential for growth. This article delves into the nuances of the current ratio, exploring its calculation, interpretation, and the insights it provides into a company’s financial standing.

Understanding the Components of the Current Ratio

The current ratio is a simple yet powerful liquidity ratio that provides a clear picture of a company’s ability to cover its short-term liabilities with its short-term assets. To truly grasp what the current ratio indicates, it’s essential to first understand its constituent parts: current assets and current liabilities. These components are typically found on a company’s balance sheet, which is a financial statement that reports a company’s assets, liabilities, and shareholders’ equity at a specific point in time.

Defining Current Assets

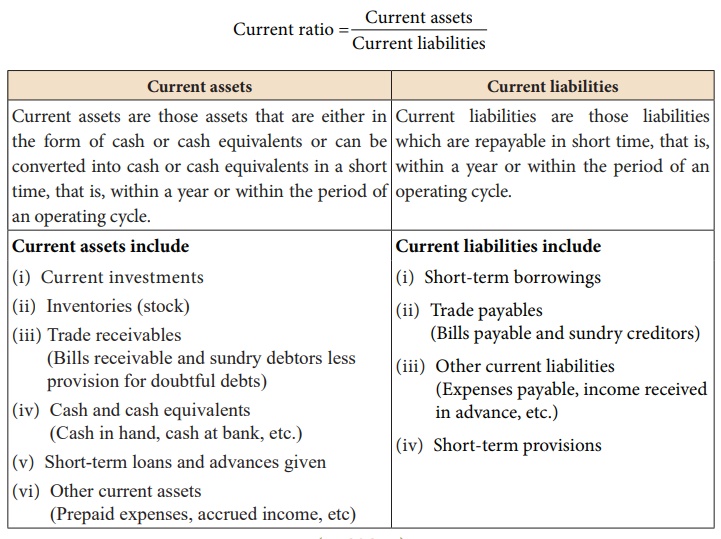

Current assets are resources that a company expects to convert into cash, sell, or consume within one year or its operating cycle, whichever is longer. The operating cycle refers to the period it takes for a company to purchase inventory, sell it, and collect the cash from the sale. These assets are considered the most liquid and readily available forms of a company’s wealth.

- Cash and Cash Equivalents: This is the most liquid form of current asset. It includes physical currency, bank deposits, and highly liquid short-term investments that can be readily converted into cash with minimal risk of value fluctuation. Examples include money market accounts and short-term government bonds.

- Marketable Securities: These are short-term investments in financial instruments, such as stocks and bonds, that are easily bought and sold in the public market. They are expected to be converted into cash within a year.

- Accounts Receivable: This represents the money owed to a company by its customers for goods or services that have been delivered but not yet paid for. A healthy accounts receivable balance indicates strong sales and effective credit policies, but an aging receivable can signal collection issues.

- Inventory: This includes raw materials, work-in-progress goods, and finished goods that a company holds for sale. The value of inventory is typically recorded at the lower of cost or market value. A high level of inventory can tie up significant capital, while too little can lead to lost sales.

- Prepaid Expenses: These are expenses that have been paid in advance but have not yet been consumed or used. Examples include prepaid rent, insurance premiums, and subscriptions. While not directly convertible to cash, they represent resources that will be used in the near future.

Defining Current Liabilities

Current liabilities, conversely, represent obligations that a company is expected to settle within one year or its operating cycle, whichever is longer. These are essentially short-term debts that the company owes to external parties.

- Accounts Payable: This is the money a company owes to its suppliers for goods or services purchased on credit. It represents short-term financing from suppliers.

- Short-Term Loans and Notes Payable: These are borrowings that are due within one year. This can include lines of credit, short-term bank loans, and commercial paper.

- Accrued Expenses: These are expenses that have been incurred but not yet paid. Examples include wages payable, taxes payable, and interest payable.

- Current Portion of Long-Term Debt: This represents the portion of a company’s long-term debt that is due within the next twelve months.

- Deferred Revenue (Unearned Revenue): This is cash received by a company for goods or services that have not yet been delivered or rendered. It represents an obligation to provide those goods or services in the future.

Calculating and Interpreting the Current Ratio

The calculation of the current ratio is straightforward, but its interpretation requires careful consideration of various factors. A simple formula provides the initial insight, but the true meaning emerges when this ratio is analyzed within its specific industry context and over time.

The Formula for the Current Ratio

The current ratio is calculated using the following formula:

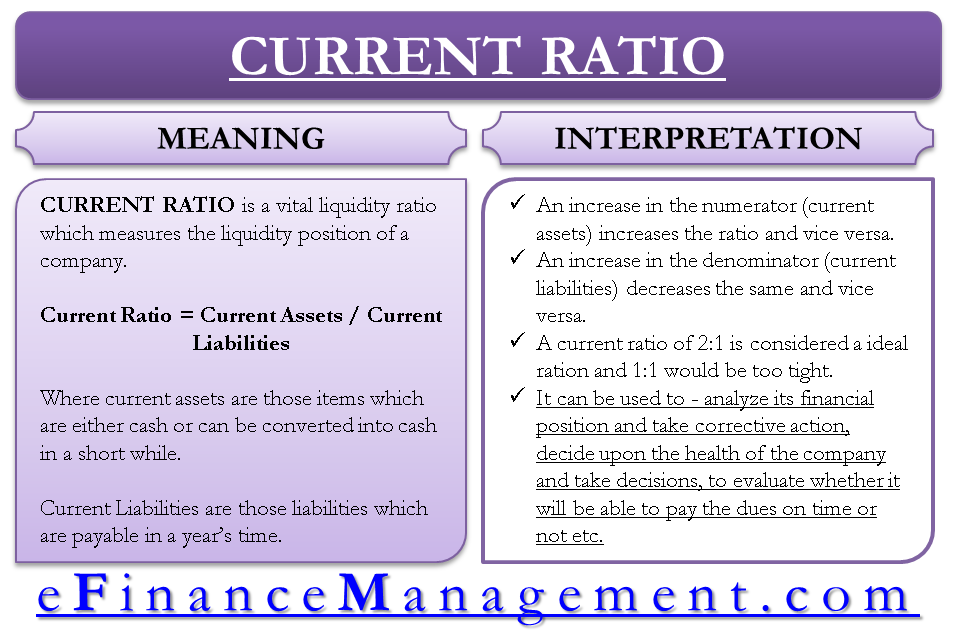

Current Ratio = Current Assets / Current Liabilities

For instance, if a company has $500,000 in current assets and $250,000 in current liabilities, its current ratio would be $500,000 / $250,000 = 2. This means the company has $2 in current assets for every $1 of current liabilities.

What a High Current Ratio Indicates

A higher current ratio generally suggests that a company has sufficient liquid assets to cover its short-term obligations. This can be viewed positively, as it implies a lower risk of defaulting on its immediate debts.

- Strong Liquidity and Solvency: A robust current ratio signals a company’s ability to meet its financial commitments as they come due. This financial stability can enhance its creditworthiness and make it more attractive to lenders and investors.

- Financial Flexibility: Companies with a high current ratio often possess greater flexibility to manage unexpected expenses, take advantage of growth opportunities, or navigate economic downturns without facing immediate cash flow crises.

- Potential for Inefficient Asset Utilization: However, an excessively high current ratio might also indicate that the company is not efficiently utilizing its assets. For example, it could be holding too much cash that could be invested to generate higher returns, or it might have excessive inventory that is tying up capital and increasing storage costs.

What a Low Current Ratio Indicates

Conversely, a low current ratio can signal potential financial distress and a higher risk of liquidity problems.

- Liquidity Risk: A ratio below 1 means that a company has more current liabilities than current assets, indicating it may struggle to meet its short-term obligations. This could lead to difficulties in paying suppliers, employees, or creditors, potentially damaging its reputation and operational capacity.

- Increased Reliance on External Financing: Companies with low current ratios might need to rely heavily on short-term borrowing or equity financing to meet their obligations, which can be expensive and dilutive.

- Operational Inefficiencies: A consistently low current ratio could point to underlying issues with inventory management, accounts receivable collection, or overall cash flow management.

Factors Influencing the Current Ratio

The interpretation of the current ratio is not a one-size-fits-all approach. Several external and internal factors can influence what a “good” or “bad” current ratio looks like for a particular company.

Industry Benchmarks

Different industries have distinct operating models and capital requirements, which directly impact their typical current ratios. For instance, businesses with long production cycles or those that hold substantial inventory, like manufacturing or retail, may naturally have higher current ratios than service-based industries or technology companies.

- Retail and Manufacturing: These sectors often require significant investment in inventory and may have extended payment terms with suppliers, leading to higher current assets relative to current liabilities.

- Technology and Service Industries: Companies in these sectors often have lower inventory levels and may receive payment more promptly for their services, potentially resulting in lower current ratios.

- Utility Companies: These businesses typically have stable revenues and predictable expenses, often exhibiting moderate current ratios.

Comparing a company’s current ratio to the average or median for its industry provides a more meaningful context for assessment.

Economic Conditions

The broader economic environment plays a significant role in a company’s liquidity and, consequently, its current ratio. During economic downturns, businesses may face slower sales, increased difficulty in collecting receivables, and tighter credit markets.

- Recessionary Periods: In challenging economic times, companies may see their current assets diminish (e.g., declining inventory values, slower collections) while their liabilities may remain stable or increase, leading to a lower current ratio.

- Periods of Economic Growth: Conversely, during periods of expansion, sales may increase, leading to higher accounts receivable, and companies might be more willing to extend credit, potentially impacting the ratio.

Company-Specific Strategies and Policies

A company’s internal management decisions and financial strategies can significantly shape its current ratio. These include policies related to credit extension, inventory management, and dividend payments.

- Aggressive Growth Strategies: Companies pursuing rapid expansion might invest heavily in inventory and accounts receivable, leading to a temporarily lower current ratio.

- Conservative Financial Management: A company focused on maintaining a strong liquidity buffer might opt for higher cash reserves and more stringent credit policies, resulting in a higher current ratio.

- Working Capital Management: Effective working capital management aims to optimize the balance between current assets and current liabilities to ensure operational efficiency and financial health.

Beyond the Current Ratio: Related Liquidity Metrics

While the current ratio provides a valuable overview of short-term liquidity, it’s not the sole determinant of a company’s financial health. Analyzing other liquidity ratios alongside the current ratio offers a more comprehensive understanding.

The Quick Ratio (Acid-Test Ratio)

The quick ratio, also known as the acid-test ratio, is a more stringent measure of liquidity. It excludes less liquid current assets, primarily inventory, from the calculation, as inventory can sometimes be difficult to convert to cash quickly without a loss in value. The formula is:

Quick Ratio = (Current Assets – Inventory) / Current Liabilities

A quick ratio of 1:1 or higher is generally considered healthy, indicating that a company can meet its short-term obligations without relying on the sale of inventory.

The Cash Ratio

The cash ratio is the most conservative liquidity ratio. It measures a company’s ability to pay off its current liabilities with only its cash and cash equivalents. The formula is:

Cash Ratio = (Cash + Cash Equivalents) / Current Liabilities

A high cash ratio signifies a company’s ability to meet its obligations immediately, but like a very high current ratio, it can also suggest that the company is not optimally deploying its cash for potential growth and investment.

Conclusion: The Current Ratio as a Financial Barometer

In conclusion, the current ratio serves as a vital financial barometer, offering crucial insights into a company’s short-term liquidity and its ability to meet its immediate financial obligations. By examining the relationship between current assets and current liabilities, stakeholders can gauge a company’s financial resilience and operational efficiency. A healthy current ratio suggests a company is well-positioned to navigate short-term challenges, while an unfavorable ratio may signal potential liquidity risks that require attention.

However, it is imperative to remember that the current ratio should not be analyzed in isolation. Its interpretation is best achieved when considered within the context of industry benchmarks, prevailing economic conditions, and the company’s unique financial strategies. By employing a holistic approach and analyzing the current ratio alongside other liquidity metrics like the quick ratio and cash ratio, investors, creditors, and management can gain a more robust and nuanced understanding of a company’s financial health, enabling more informed and strategic decision-making. The current ratio, when properly understood and applied, is an indispensable tool in the assessment of financial stability and operational viability.