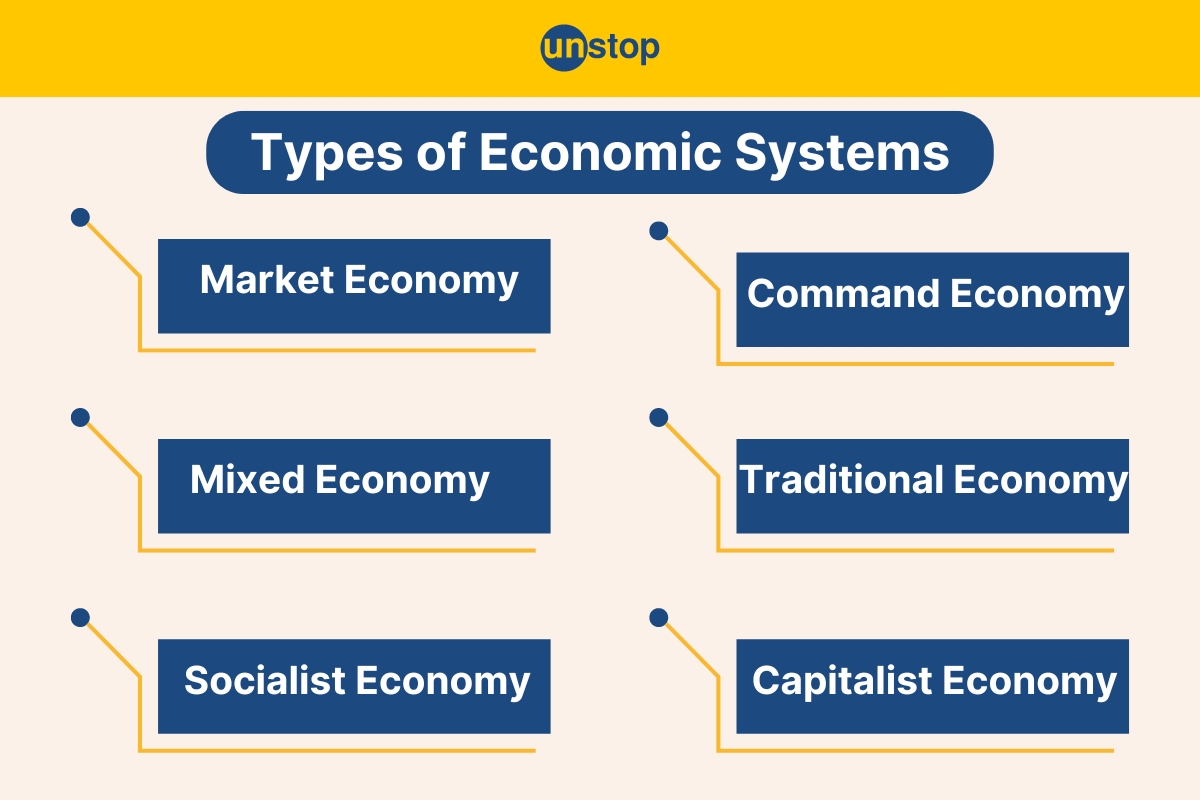

The way a society organizes the production, distribution, and consumption of goods and services is fundamental to its structure and well-being. This organization is dictated by its economic system, which answers three core questions: what to produce, how to produce it, and for whom to produce it. While myriad variations and hybrid models exist, economic systems can be broadly categorized into three primary archetypes: traditional, command, and market economies. Understanding these foundational systems provides a crucial lens through which to analyze the economic realities of nations, the evolution of industries, and the impact of technological advancements on how we live and work.

The Enduring Influence of Traditional Economic Systems

Traditional economic systems are the oldest and, historically, the most prevalent form of economic organization. They are characterized by their deep roots in custom, tradition, and habit. Decisions regarding production, distribution, and consumption are largely determined by long-standing practices, beliefs, and social norms passed down through generations. In such economies, economic roles are often inherited, and the methods of production are typically rudimentary, relying on skills and technologies that have been used for centuries.

Sustaining Livelihoods Through Established Practices

In a traditional economy, the “what to produce” question is answered by looking at what has always been produced – usually basic necessities like food, clothing, and shelter. Agriculture, hunting, gathering, and rudimentary crafts form the backbone of production. The “how to produce” is dictated by the inherited knowledge and tools, with little room for innovation or deviation from established methods. For example, farming techniques might involve manual labor and simple tools passed down from ancestors, with little adoption of modern machinery.

The “for whom to produce” is also heavily influenced by social hierarchies and kinship structures. Goods are often distributed within families, tribes, or communities based on social status, age, and established obligations. Barter and direct exchange are common forms of trade, rather than the use of standardized currency. This system fosters a strong sense of community and interdependence, as survival often depends on collective effort and adherence to shared customs.

Challenges and Adaptations in a Changing World

While traditional economies offer stability and a strong sense of cultural identity, they are inherently resistant to change and often struggle to adapt to external pressures. Low levels of productivity, limited technological advancement, and susceptibility to natural disasters can lead to subsistence living and a lack of economic surplus. As the world becomes increasingly interconnected, even the most remote traditional economies face exposure to new ideas, technologies, and global markets. This exposure often forces adaptation, leading to a gradual shift towards more modern economic practices, sometimes blurring the lines between purely traditional and other economic models. The resilience of these systems lies in their ability to preserve cultural heritage while slowly integrating elements that enhance survival and prosperity.

The Centralized Power of Command Economic Systems

In stark contrast to the decentralized nature of traditional systems, command economies place the power of economic decision-making squarely in the hands of a central authority, typically the government. In this model, the state owns and controls the major means of production – land, factories, and natural resources – and dictates what goods and services will be produced, how they will be produced, and who will receive them. The overarching goal is often to achieve specific societal objectives, such as rapid industrialization, social equality, or national defense.

Government as the Sole Economic Planner

Under a command economy, the “what to produce” is determined by the central planning agency, which sets production targets for various industries based on the perceived needs of the nation. This can involve prioritizing heavy industry, agriculture, or defense over consumer goods. The “how to produce” is also centrally managed, with the government allocating resources, labor, and technology to state-owned enterprises. Managers of these enterprises are expected to meet the quotas set by the planners, often with little autonomy to make independent decisions.

The “for whom to produce” is typically determined through government-issued rationing systems, price controls, and the allocation of jobs. Wages are set by the state, and the availability of goods and services is managed to ensure equitable distribution, at least in theory. This approach aims to eliminate the inequalities and perceived inefficiencies of market competition, striving for a society where everyone’s basic needs are met. Examples of countries that have historically operated or continue to operate under command economic principles include the former Soviet Union and North Korea.

Strengths, Weaknesses, and the Quest for Efficiency

Command economies can, in theory, mobilize resources quickly to achieve large-scale projects and can ensure a basic standard of living for all citizens. They can also prevent the extreme economic disparities that can arise in market economies. However, these systems often suffer from significant drawbacks. Central planners can struggle to accurately gauge consumer demand, leading to chronic shortages of some goods and surpluses of others. The lack of competition and profit motive can stifle innovation and reduce efficiency, as enterprises have little incentive to improve their products or processes. Bureaucracy and corruption can also be prevalent. Over time, many command economies have faced challenges in keeping pace with technological advancements and the evolving needs of their populations, leading to periods of economic stagnation or reform.

The Dynamic Engine of Market Economic Systems

Market economic systems, also known as capitalism, are characterized by decentralized decision-making driven by the interactions of buyers and sellers in markets. Private ownership of the means of production is paramount, and individuals and firms are free to pursue their own economic interests. The forces of supply and demand, competition, and the pursuit of profit are the primary drivers of economic activity.

Consumer Sovereignty and Producer Competition

In a market economy, the “what to produce” is largely determined by consumer demand. Consumers signal their preferences through their purchasing decisions, and producers respond by creating the goods and services that are most in demand. This concept is often referred to as “consumer sovereignty.” The “how to produce” is driven by efficiency and innovation. Firms compete with each other to produce goods and services at the lowest possible cost and of the highest possible quality to attract customers. This competition incentivizes the adoption of new technologies and improved production methods.

The “for whom to produce” is determined by the ability and willingness of individuals to pay for goods and services. Those who possess valuable skills, own productive assets, or have accumulated wealth are generally able to acquire a greater share of the available goods and services. Wages are determined by the market forces of supply and demand for labor, and profits are earned by firms that successfully meet consumer needs and manage their operations efficiently.

The Benefits of Freedom and the Perils of Instability

Market economies are renowned for their ability to foster innovation, generate wealth, and offer a wide variety of goods and services to consumers. The freedom to innovate and the reward for success can lead to rapid economic growth and improvements in living standards. Competition also tends to keep prices in check and encourages efficiency. However, market systems are not without their challenges. They can lead to significant income inequality, as not everyone possesses the same skills or opportunities. Market failures, such as monopolies, externalities (like pollution), and information asymmetry, can necessitate government intervention. Furthermore, market economies are prone to cycles of boom and bust, with periods of recession and unemployment.

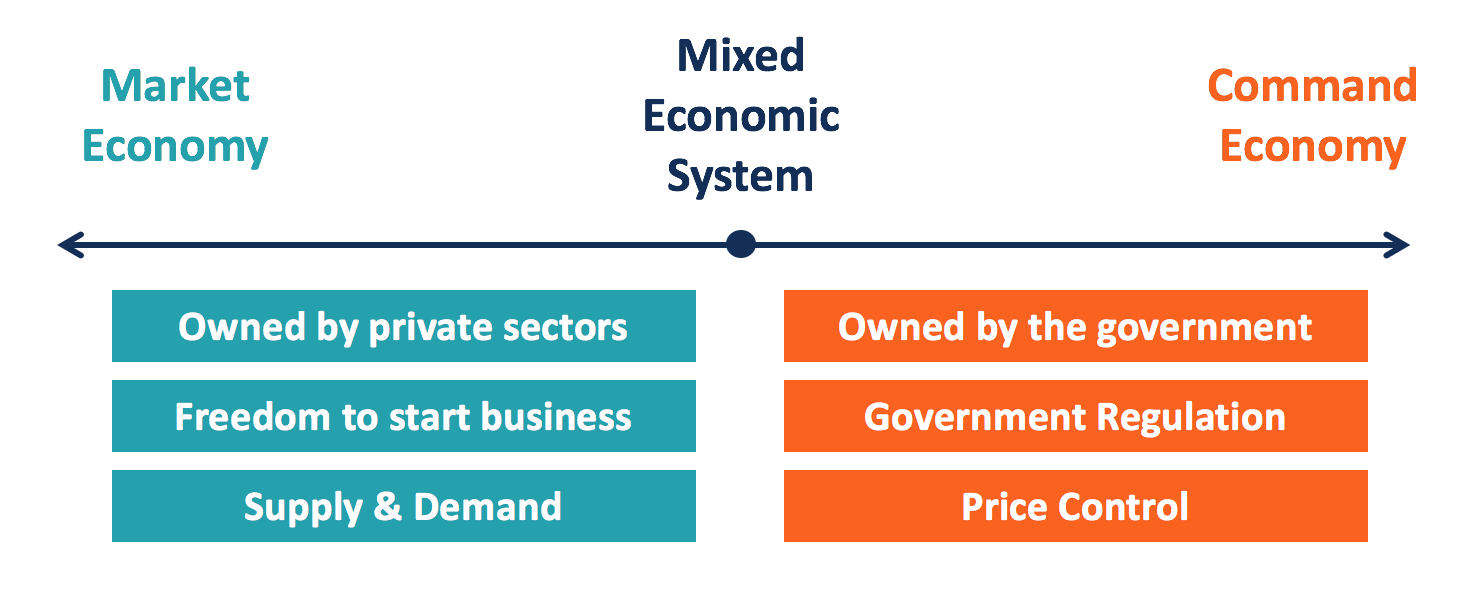

The Interplay of Systems: Mixed Economies

In reality, very few economies operate as pure examples of traditional, command, or market systems. Instead, most modern economies are mixed economies, incorporating elements from more than one of these fundamental archetypes. The degree to which an economy leans towards market or command principles, or retains traditional aspects, varies greatly from country to country and can evolve over time.

Blending Principles for Stability and Growth

Mixed economies seek to leverage the strengths of different systems while mitigating their weaknesses. For instance, a predominantly market economy might introduce government regulations to address environmental concerns (an element that could be seen as a nod to command-style intervention for public good) or provide social safety nets like unemployment benefits and public education to reduce inequality and provide basic opportunities (addressing potential downsides of pure market outcomes). Conversely, a historically command economy might introduce market reforms to stimulate private enterprise and increase efficiency.

The balance in a mixed economy is often a subject of ongoing political and social debate. Different societies will strike different balances based on their values, historical context, and immediate economic challenges. The “what to produce” might be largely market-driven, but certain essential services like healthcare or infrastructure might be heavily subsidized or provided by the state. The “how to produce” is typically driven by private enterprise, but labor laws and environmental standards set by the government influence production methods. The “for whom to produce” is largely determined by market forces, but progressive taxation and social welfare programs aim to redistribute wealth and ensure a baseline standard of living.

Navigating the Continuum of Economic Organization

The concept of mixed economies highlights the dynamic and adaptive nature of economic organization. It acknowledges that no single economic system is perfect and that practical governance often involves a pragmatic blend of approaches. Understanding the core principles of traditional, command, and market economies provides the essential framework for analyzing these mixed systems, appreciating the trade-offs involved in policy decisions, and comprehending the diverse economic landscapes that shape our world. The ongoing evolution of economic thought and practice suggests that the future will likely see further refinement and adaptation within these mixed models, driven by technological advancements, global challenges, and the ever-present human desire for prosperity and well-being.