The Harmonized Sales Tax (HST) is a critical component of Canada’s tax system, particularly for businesses operating within the country. It represents a significant shift from the previous Goods and Services Tax (GST) and Provincial Sales Tax (PST) system, aiming to streamline tax collection and reduce the burden on consumers and businesses alike. For many, particularly those involved in the import/export of goods or services, understanding HST is not just a matter of compliance but a fundamental aspect of effective financial management. This article will delve into the intricacies of Canadian HST, exploring its origins, its application across different provinces, and its implications for various economic sectors.

Understanding the Foundation: GST and its Harmonization

The genesis of HST lies in the Goods and Services Tax (GST), a federal value-added tax introduced in Canada on January 1, 1991. Prior to the GST, consumers paid a federal tax on goods and services, while many provinces levied their own provincial sales taxes (PST). This dual-taxation system created complexities, particularly for businesses engaged in inter-provincial trade, as different tax rates and rules applied depending on the province of origin and destination. The GST was designed to replace the federal manufacturers’ sales tax and to create a more uniform tax environment across the nation.

The Rationale Behind the GST

The introduction of the GST was driven by several key economic objectives:

- Simplification of the Tax System: By consolidating federal sales tax into a single, broad-based tax, the GST aimed to reduce the administrative burden on businesses and simplify tax compliance for consumers.

- Economic Neutrality: The GST was intended to be a consumption tax that applied broadly to most goods and services, with limited exceptions. This neutrality was crucial for ensuring that business decisions were driven by market forces rather than tax considerations.

- International Competitiveness: A key motivation for the GST was to align Canada with the value-added tax systems prevalent in many of its trading partners. This was seen as essential for maintaining the competitiveness of Canadian exports in global markets. Unlike a multi-stage sales tax that is levied at each stage of production and distribution, a value-added tax is collected at each stage but is ultimately borne by the final consumer. Businesses can claim credits for the GST they pay on their inputs, effectively ensuring that the tax is only applied to the value added at each stage.

- Revenue Generation: While simplification and competitiveness were primary drivers, the GST also served as a significant source of revenue for the federal government.

The Evolution to Harmonized Sales Tax (HST)

While the GST provided a federal framework, several provinces continued to maintain their own provincial sales taxes. This meant that consumers in these provinces often paid a combined federal and provincial sales tax that could be significantly higher than the GST alone. To address this, the concept of the Harmonized Sales Tax (HST) emerged.

The HST is essentially a blend of the federal GST and the provincial sales tax into a single, unified tax. In provinces that adopt the HST, the GST rate is combined with a portion of the provincial sales tax to create a single, higher tax rate. This harmonization offers several potential benefits:

- Reduced Tax Collection Burden: Businesses no longer need to collect two separate taxes (GST and PST) on taxable goods and services. They collect a single HST rate, simplifying their invoicing and remittance processes.

- Improved Cash Flow: Businesses that are eligible to claim input tax credits (ITCs) for the HST they pay can recover a significant portion of the tax paid on their business inputs. This can improve their cash flow and reduce the overall cost of doing business.

- Elimination of Tax Cascades: In provinces with separate GST and PST systems, businesses that do not pay PST on their inputs might have to pass that PST on to their customers. This can lead to a “tax cascade,” where the tax is levied on tax, increasing the final price. The HST, by allowing businesses to claim ITCs for all HST paid on business inputs, aims to eliminate this cascade and ensure that the tax is only applied to final consumption.

- Greater Tax Certainty: A single, harmonized rate provides greater certainty for businesses regarding their tax obligations and for consumers regarding the final price of goods and services.

Provinces Adopting the HST: A Diverse Landscape

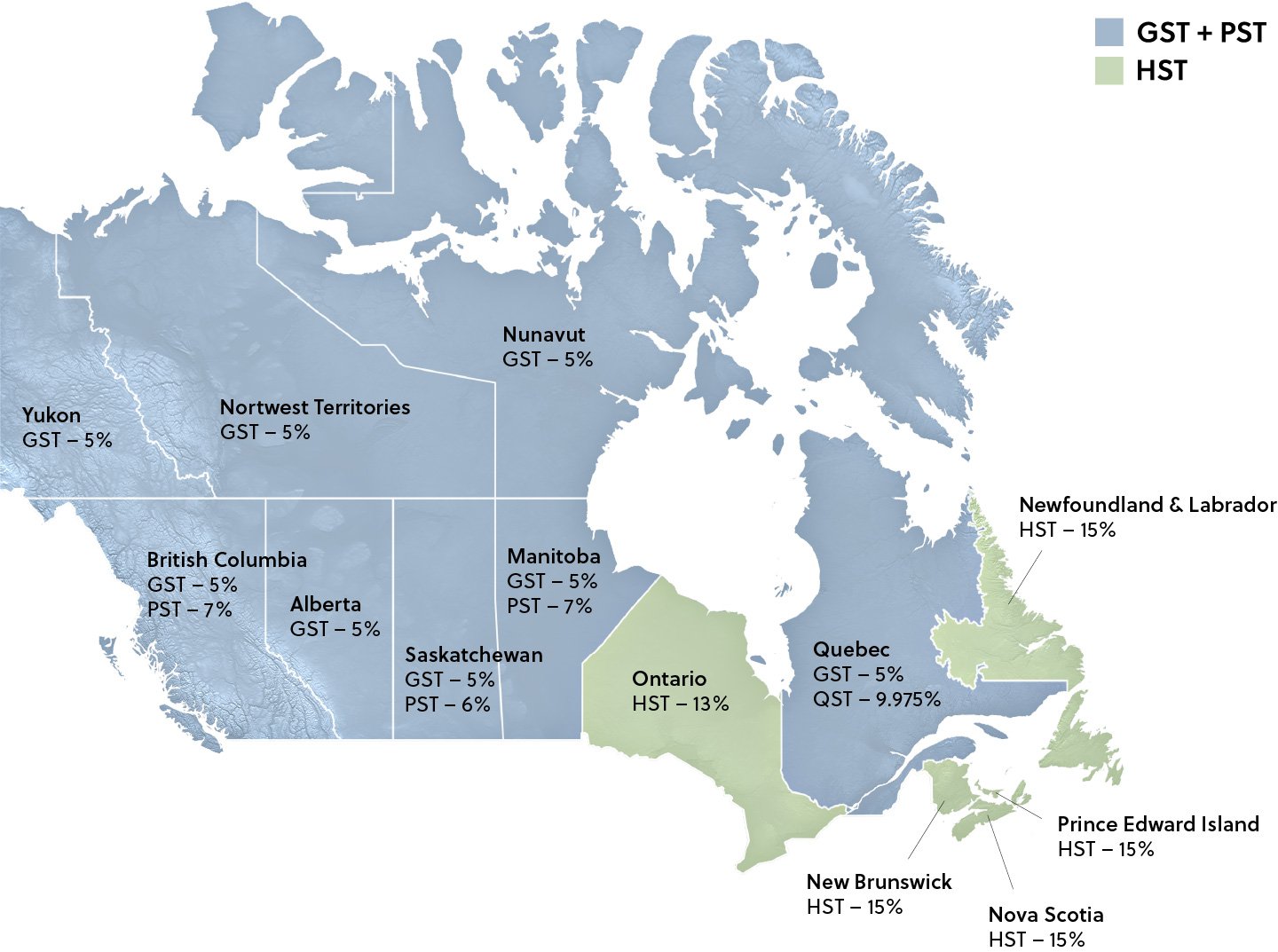

The adoption of the HST is not uniform across all Canadian provinces. Currently, five provinces have implemented the HST:

- Ontario: Introduced HST in July 2010, merging the 5% federal GST with an 8% provincial component to create an 13% HST.

- Nova Scotia: Introduced HST in May 1997, merging the 7% federal GST with an 10% provincial component to create a 15% HST.

- New Brunswick: Introduced HST in May 1997, merging the 7% federal GST with an 8% provincial component to create a 15% HST.

- Prince Edward Island: Introduced HST in April 2013, merging the 5% federal GST with a 10% provincial component to create a 15% HST.

- Newfoundland and Labrador: Introduced HST in April 2006, merging the 5% federal GST with an 8% provincial component to create a 13% HST.

It is important to note the differing rates and the specific provincial components. While the federal GST component is generally consistent, the provincial portion can vary, leading to different overall HST rates across these provinces.

Provinces Maintaining Separate GST and PST

In contrast to the HST provinces, other provinces and territories maintain separate GST and PST systems. These include:

- British Columbia: Operates with a 5% GST and a separate PST that varies by commodity.

- Saskatchewan: Operates with a 5% GST and a separate PST.

- Manitoba: Operates with a 5% GST and a separate Retail Sales Tax (RST).

- Alberta: Does not have a provincial sales tax, only the federal 5% GST.

- Yukon, Northwest Territories, and Nunavut: These territories also operate with the federal 5% GST and do not have a territorial sales tax.

The decision of whether to adopt the HST or maintain separate GST and PST systems is a complex one for each provincial government. It involves considering the economic benefits and drawbacks, the potential impact on consumers and businesses, and the alignment with broader fiscal policies. Negotiations between the federal government and provincial governments are typically required for a province to implement the HST.

Key Concepts and Implications of HST

Understanding HST involves grasping several fundamental concepts and their practical implications for individuals and businesses.

Taxable Supplies and Exempt Supplies

Not all goods and services are subject to HST. Supplies are generally categorized as either taxable or exempt.

- Taxable Supplies: These are goods and services on which HST must be charged and collected. Most goods and services purchased by consumers and businesses fall into this category.

- Exempt Supplies: These are goods and services that are specifically excluded from HST. Common examples include certain basic groceries, prescription drugs, and most health, dental, and educational services. Businesses making exempt supplies cannot charge HST and, crucially, cannot claim input tax credits for the HST they pay on their business inputs. This can significantly increase their operating costs.

Input Tax Credits (ITCs)

A cornerstone of the value-added tax system, including HST, is the mechanism of Input Tax Credits (ITCs). Registered businesses that collect HST on their taxable supplies can claim ITCs to recover the HST they have paid on eligible purchases and expenses related to their commercial activity.

- How ITCs Work: When a business purchases goods or services that are subject to HST and uses them in its commercial activities, it pays the HST to its supplier. The business can then claim this HST as an ITC when it remits its net HST to the Canada Revenue Agency (CRA). The net HST payable by a business is calculated as the total HST collected on its taxable sales minus the total ITCs it is eligible to claim.

- Importance for Businesses: For businesses in HST provinces, ITCs are crucial for reducing their tax burden and ensuring that the HST is ultimately borne by the final consumer. Businesses that are not registered for HST (e.g., small suppliers below a certain revenue threshold) cannot charge HST and cannot claim ITCs.

Registration Requirements

Businesses that provide taxable goods or services in Canada must register for a GST/HST account with the CRA if their total annual taxable revenues exceed a certain threshold (currently $30,000). Once registered, they are required to collect HST on their taxable sales and remit it to the CRA.

- Small Suppliers: Businesses with annual taxable revenues below the threshold are considered “small suppliers” and are generally not required to register for, collect, or remit GST/HST. However, they also cannot claim ITCs on their business purchases. They can voluntarily register if they choose to.

- Voluntary Registration: Even if below the threshold, some small suppliers may choose to register voluntarily, particularly if they incur significant amounts of GST/HST on their business purchases and want to claim ITCs.

Filing and Remitting HST

Registered businesses are required to file GST/HST returns periodically (monthly, quarterly, or annually, depending on their sales volume and CRA requirements). These returns report the total HST collected on sales and the total ITCs claimed on business expenses. The difference is the net amount of HST that must be remitted to the CRA.

Impact and Considerations

The implementation and operation of HST have far-reaching implications for various stakeholders in the Canadian economy.

For Consumers

In HST provinces, consumers generally see a single, higher tax rate on many purchases compared to provinces with only GST. However, the potential for improved cash flow for businesses and reduced administrative complexity can, in theory, lead to more competitive pricing in the long run. For consumers, understanding which goods and services are exempt is crucial for budgeting and managing their expenses effectively.

For Businesses

The HST simplifies tax collection and remittance processes for businesses in participating provinces. The ability to claim ITCs can significantly reduce the cost of doing business. However, businesses must diligently track their sales and purchases, understand the rules around taxable and exempt supplies, and ensure accurate record-keeping for compliance. Businesses operating in both HST and non-HST provinces face the added complexity of navigating different tax regimes.

For the Canadian Economy

The HST is intended to promote economic efficiency and competitiveness. By harmonizing taxes, it can reduce internal trade barriers and simplify cross-border transactions within Canada. The revenue generated from HST contributes to federal and provincial government budgets, funding public services. However, the higher tax rates in HST provinces can sometimes be a point of political debate and public concern.

In conclusion, understanding Canadian HST is paramount for anyone involved in commerce within the country. It is a complex yet integral part of the tax landscape, designed to streamline tax administration and foster economic efficiency. By grasping its foundational principles, provincial variations, and operational mechanisms like input tax credits, individuals and businesses can navigate its intricacies with greater confidence and ensure compliance.