Understanding what constitutes a “good” credit score is crucial in today’s financial landscape. A strong credit score acts as a key that unlocks numerous financial opportunities, from securing favorable loan terms to simplifying rental applications. Conversely, a low score can create significant barriers, leading to higher interest rates, denied applications, and a generally more challenging path to financial goals. This guide will delve into the intricacies of credit scoring, defining what a good score is, the factors that influence it, and strategies for building and maintaining excellent credit.

The Anatomy of a Credit Score

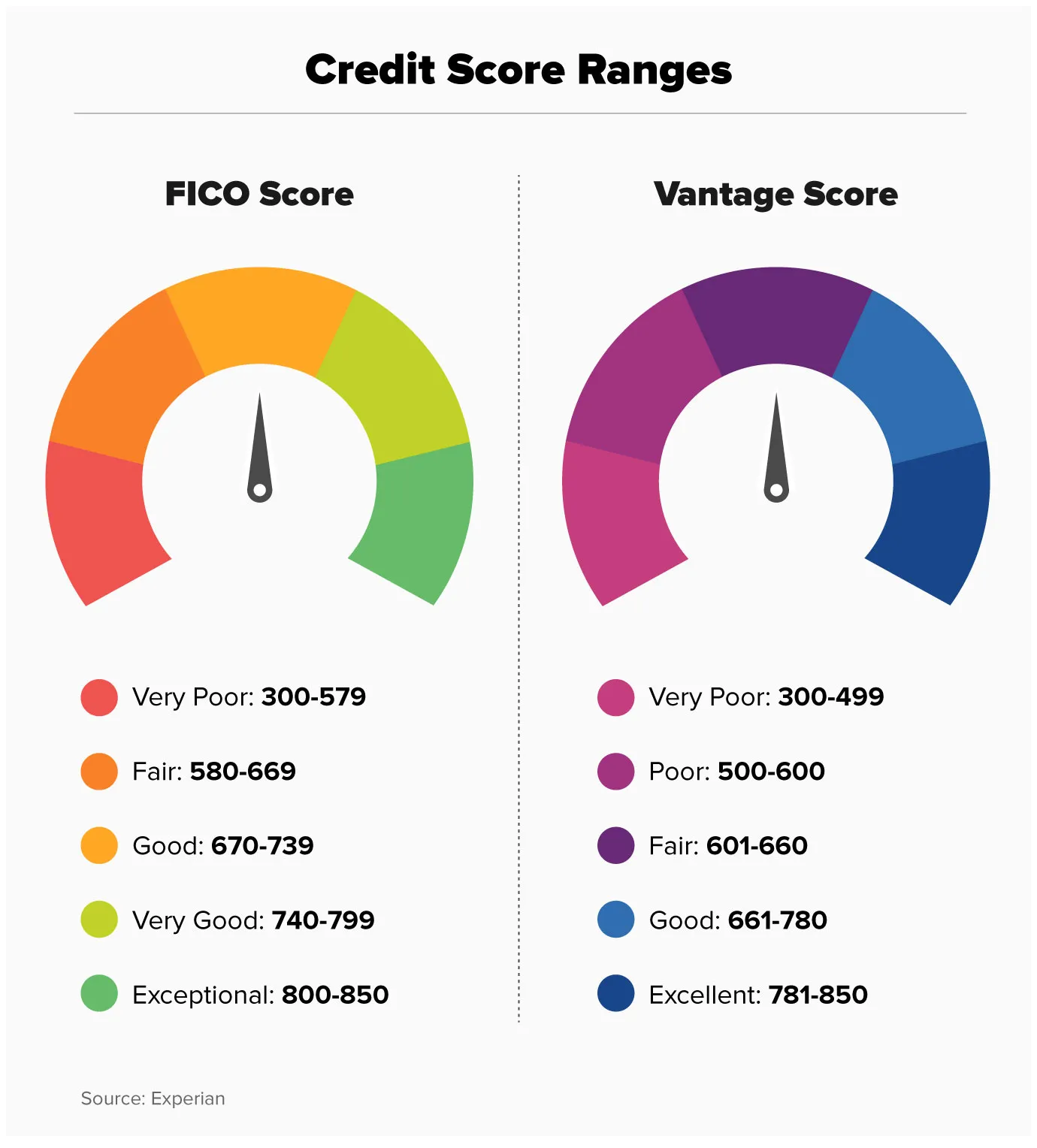

Credit scores are numerical representations of your creditworthiness, calculated using information from your credit reports. While various scoring models exist, the most widely used is the FICO score, with others like VantageScore also prevalent. These models aim to predict the likelihood of you repaying borrowed money. Understanding the general range and what is considered good is the first step.

Understanding the Score Ranges

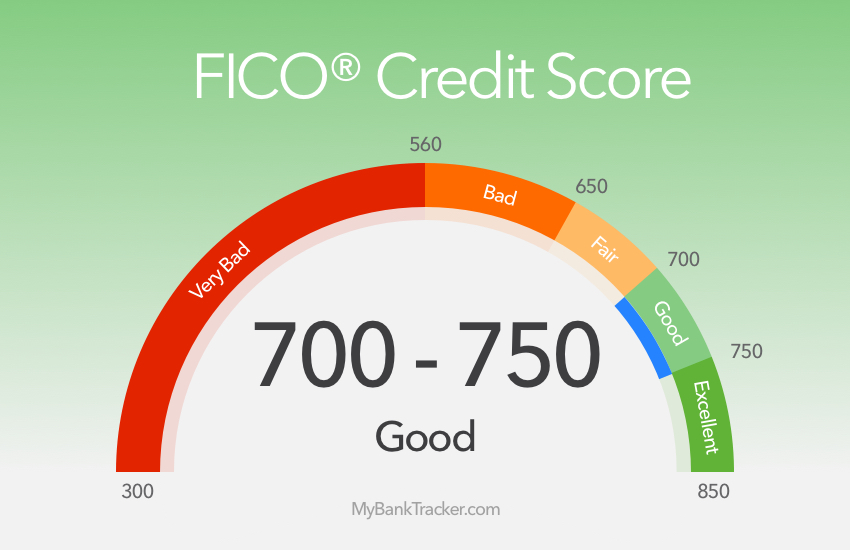

Credit scores typically fall within a range from 300 to 850. While these numbers can seem abstract, they translate into tangible financial implications.

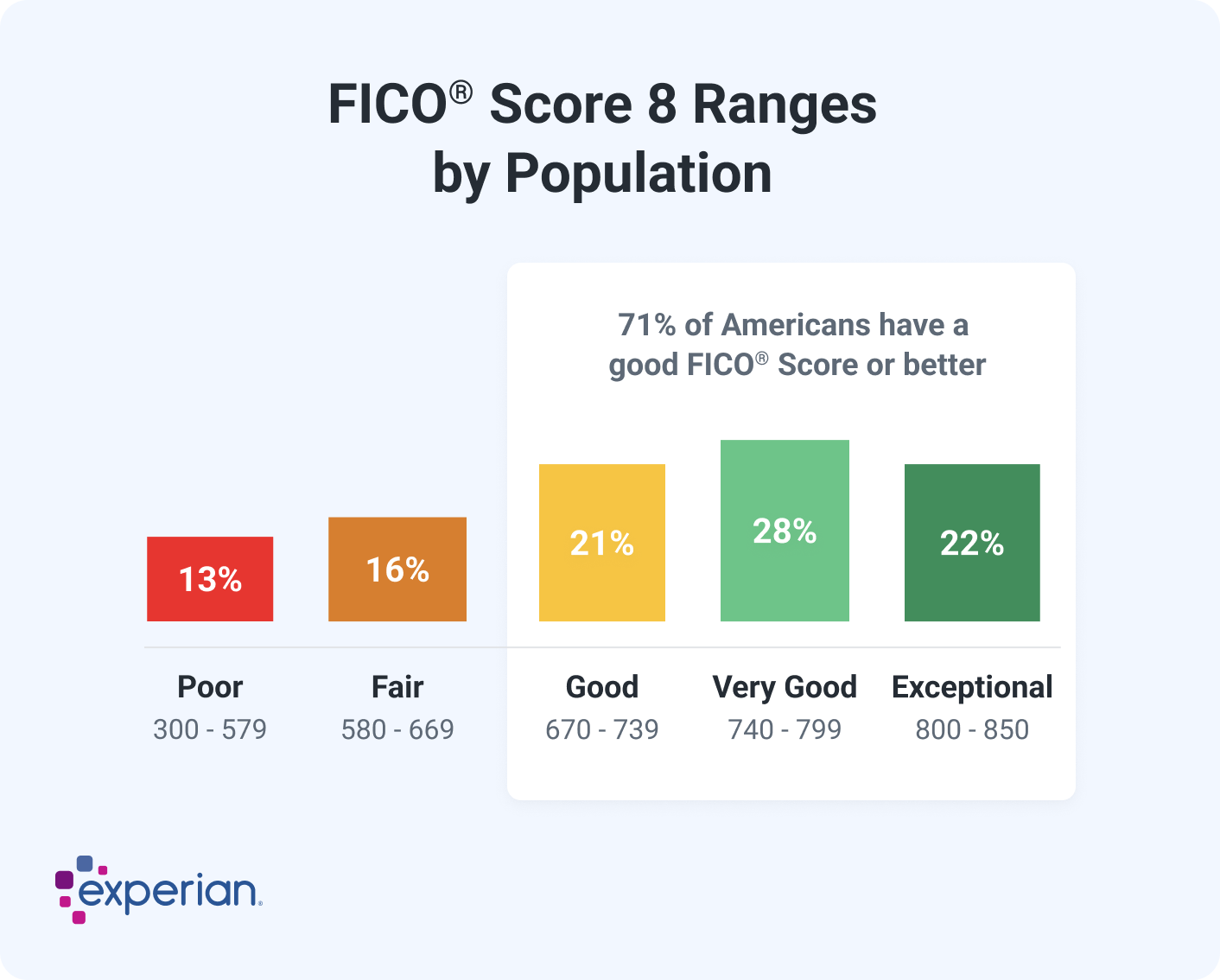

- Poor Credit (300-579): Scores in this range indicate a high risk to lenders. Obtaining credit will be extremely difficult, and if possible, it will come with very high interest rates and unfavorable terms. This range often signifies a history of missed payments, defaults, or significant debt.

- Fair Credit (580-669): While an improvement, scores in this range are still considered below average. You might qualify for some credit products, but the interest rates will likely be higher than prime borrowers. Lenders see a moderate risk.

- Good Credit (670-739): This is a significant milestone. A “good” credit score opens doors to more favorable loan terms, lower interest rates on mortgages, auto loans, and credit cards. Lenders view you as a reliable borrower.

- Very Good Credit (740-799): With a “very good” score, you are in a strong position. You can expect to be offered the best interest rates, generous credit limits, and a wider array of loan options. Lenders actively compete for your business.

- Exceptional Credit (800-850): This is the pinnacle of creditworthiness. An “exceptional” credit score signifies a near-perfect repayment history and minimal financial risk. You’ll have access to the absolute best rates, exclusive offers, and significant negotiation power.

It’s important to note that these ranges can vary slightly depending on the scoring model and the lender’s specific criteria. However, generally speaking, aiming for a score above 700 is a solid objective for most individuals seeking favorable financial outcomes.

Key Factors Influencing Your Score

Several key components contribute to your credit score. Understanding these factors is crucial for targeted improvement.

Payment History: The Cornerstone of Your Score

Your payment history is the single most impactful factor in your credit score, typically accounting for about 35% of the score. This metric reflects how consistently you pay your bills on time.

- On-Time Payments: Every payment made by its due date is a positive mark. This includes credit cards, loans, mortgages, and even some utility bills if they are reported to credit bureaus.

- Late Payments: Even a single late payment, especially if it’s 30 days or more past due, can significantly damage your score. The severity of the impact increases with the length of the delinquency (30, 60, 90+ days late).

- Collections and Charge-offs: Accounts sent to collections or charged off by the lender are severe negative marks that can drastically lower your score and remain on your report for many years.

- Bankruptcy and Foreclosure: These are the most severe negative events and will have a long-lasting detrimental effect on your credit score, often taking years to recover from.

Credit Utilization: Managing Your Debt Wisely

Credit utilization refers to the amount of credit you are using compared to your total available credit. This factor typically makes up around 30% of your credit score.

- The 30% Rule: A common guideline is to keep your credit utilization ratio below 30% for each credit card and across all your cards combined. For example, if you have a credit card with a $10,000 limit, keeping your balance below $3,000 is ideal.

- High Utilization Impact: Using a large portion of your available credit signals to lenders that you may be overextended and at a higher risk of defaulting.

- Low Utilization Benefit: Keeping your balances low demonstrates responsible credit management and can positively influence your score.

Length of Credit History: The Value of Time

The average age of your credit accounts and the age of your oldest account contribute approximately 15% to your credit score.

- Older Accounts are Better: Generally, a longer credit history indicates more experience managing credit. Lenders prefer to see a track record of responsible borrowing over an extended period.

- Closing Old Accounts: While tempting, closing older credit accounts, especially those with a positive payment history and no annual fee, can actually shorten your average credit history length and potentially lower your score.

- New Accounts: While opening new accounts can offer benefits, having too many new accounts opened in a short period can negatively impact this factor and signal a higher risk.

Credit Mix: Diversification in Borrowing

The types of credit you have (e.g., credit cards, installment loans like mortgages or auto loans) make up about 10% of your score.

- Demonstrates Versatility: Having a mix of credit types, such as revolving credit (credit cards) and installment credit (loans), can demonstrate your ability to manage different forms of debt responsibly.

- Not a Primary Driver: While beneficial, this factor is less impactful than payment history or credit utilization. Forcing yourself into unnecessary debt just to diversify your credit mix is not advisable.

New Credit: Opening Accounts Responsibly

The number of recent credit inquiries and newly opened accounts accounts for about 10% of your score.

- Hard Inquiries: When you apply for new credit, lenders perform a “hard inquiry” on your credit report. Multiple hard inquiries within a short period can indicate that you are seeking a lot of credit, which can be seen as a sign of financial distress.

- Soft Inquiries: These occur when you check your own credit score or when a company checks your credit for pre-approved offers. Soft inquiries do not impact your credit score.

- Strategic Applications: It’s best to apply for credit only when you genuinely need it and to space out applications to avoid negatively impacting your score.

Achieving and Maintaining a “Good” Credit Score

Building and maintaining a good credit score is an ongoing process that requires discipline and smart financial habits.

Strategies for Building Excellent Credit

For those starting from scratch or looking to improve their score, several strategies can be effective.

Responsible Credit Card Usage

Credit cards are powerful tools for building credit, but they must be used wisely.

- Secured Credit Cards: For individuals with no credit history or poor credit, secured credit cards are an excellent starting point. These require a cash deposit that typically equals your credit limit, reducing the lender’s risk. Consistent, on-time payments on a secured card can help build positive credit history.

- Becoming an Authorized User: If you have a trusted friend or family member with excellent credit, they can add you as an authorized user to their credit card. Their positive payment history can then be reflected on your credit report, helping to build your score. However, ensure the primary cardholder maintains responsible habits, as their negative actions can also impact you.

- Student Credit Cards: These cards are designed for college students and often have lower credit limits and easier approval requirements, making them a good option for young adults entering the credit landscape.

Timely Bill Payments: Non-Negotiable

As the most significant factor, making all payments on time is paramount.

- Automate Payments: Set up automatic payments for your credit cards and loans. This ensures you never miss a due date, even if you forget.

- Payment Reminders: Utilize calendar reminders or budgeting apps to keep track of your bill due dates.

- Communicate with Lenders: If you anticipate difficulty making a payment, contact your lender before the due date. They may be willing to offer a payment plan or a temporary hardship arrangement to avoid a delinquency being reported.

Managing Credit Utilization Effectively

Keeping your credit utilization low is a key component of a good credit score.

- Pay Down Balances: Regularly pay down your credit card balances, ideally before the statement closing date. This reduces the reported utilization for that billing cycle.

- Request Credit Limit Increases: If you have a history of responsible use with a particular card, you can request a credit limit increase. This can lower your utilization ratio without you having to spend less, provided your spending habits remain the same.

- Diversify Payments: If you have multiple credit cards, try to distribute your spending across them rather than maxing out one card while keeping others at zero.

Maintaining Your Good Credit Score

Once you’ve achieved a good credit score, the focus shifts to consistent maintenance.

Regular Credit Report Monitoring

Your credit reports are the foundation of your credit score. Regularly reviewing them is essential.

- Annual Credit Reports: You are entitled to a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once every 12 months at AnnualCreditReport.com.

- Dispute Errors: Scrutinize your reports for any inaccuracies, such as incorrect personal information, accounts you don’t recognize, or erroneous late payments. Dispute any errors promptly with the credit bureau.

- Identify Fraud: Regularly checking your reports can help you identify fraudulent activity early, allowing you to take immediate action to protect your identity and credit.

Avoiding Excessive New Credit Applications

While acquiring new credit can be beneficial in some circumstances, it’s important to do so judiciously.

- Only Apply When Necessary: Resist the urge to apply for credit cards or loans simply because they offer introductory bonuses or rewards. Only apply when you have a genuine need for the credit.

- Shop Smart for Loans: When applying for a mortgage or auto loan, you can shop around for the best rates. Multiple inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are often treated as a single inquiry, minimizing the impact on your score.

Long-Term Financial Health

Ultimately, a good credit score is a reflection of your overall financial health and responsibility.

- Budgeting and Saving: Living within your means, creating a budget, and maintaining an emergency fund can prevent you from needing to rely heavily on credit during difficult times.

- Debt Management: Develop a plan for managing and reducing debt. Prioritizing high-interest debt can save you money in the long run and free up cash flow.

- Financial Literacy: Continuously educating yourself about personal finance and credit management will empower you to make informed decisions and maintain a strong financial standing.

In conclusion, a “good” credit score is more than just a number; it’s a testament to your financial discipline and reliability. By understanding the factors that influence your score and implementing consistent, responsible financial practices, you can not only achieve but also maintain an excellent credit standing, paving the way for greater financial freedom and security.