Understanding the tax implications of selling assets is crucial for any investor, and the distinction between short-term and long-term capital gains is a fundamental concept. This article delves into the specifics of how long-term capital gains are taxed, providing insights into the rates, factors influencing them, and strategies for managing this aspect of your investment portfolio. While the primary focus of this publication is on the exciting world of drones, flight technology, cameras, and aerial filmmaking, understanding financial principles like capital gains tax is a foundational element for anyone involved in the tech and innovation sector, which often involves significant investments in hardware, software, and intellectual property. For those of you who might be selling a drone business, specialized aerial equipment, or even shares in a drone manufacturing company, this knowledge becomes directly relevant.

Understanding Capital Gains and Losses

At its core, a capital gain occurs when you sell an asset for more than you paid for it. Conversely, a capital loss happens when you sell an asset for less than your purchase price. The “capital” in capital gains refers to capital assets, which are generally defined as property held for investment or personal use. For investors, this includes stocks, bonds, real estate, cryptocurrency, and, in the context of our niche, valuable drone equipment or even entire drone businesses.

The Holding Period: The Key Differentiator

The most critical factor in determining whether a gain or loss is short-term or long-term is the holding period. This is the amount of time you owned the asset before selling it.

- Short-Term Capital Gains: These are realized when you sell an asset that you have owned for one year or less.

- Long-Term Capital Gains: These are realized when you sell an asset that you have owned for more than one year.

The tax treatment of these two categories differs significantly, with long-term capital gains generally being taxed at more favorable rates. This preferential treatment is designed to encourage long-term investment, providing individuals and businesses with a financial incentive to hold onto assets rather than engaging in frequent trading.

Calculating Your Capital Gain or Loss

The calculation of a capital gain or loss is straightforward:

Proceeds from Sale – Cost Basis = Capital Gain or Loss

- Proceeds from Sale: This is the amount of money you received when you sold the asset.

- Cost Basis: This is generally the original purchase price of the asset. However, it can also include other costs associated with acquiring the asset, such as commissions or fees. For example, if you purchased a high-end cinematic drone for $5,000 and later sold it for $7,000, your capital gain would be $2,000. If, however, you sold it for $4,000, you would have a capital loss of $1,000. When considering the sale of a business, the cost basis can become more complex, involving the original investment, improvements, and any accumulated depreciation.

The Impact of Capital Losses

Capital losses can be used to offset capital gains. If you have more capital losses than capital gains in a given tax year, you can generally deduct up to $3,000 of those net capital losses against your ordinary income. Any remaining net capital losses can be carried forward to future tax years to offset future capital gains. This ability to offset gains with losses is a vital component of tax planning for investors, especially in volatile markets or industries experiencing rapid technological change where asset values can fluctuate significantly.

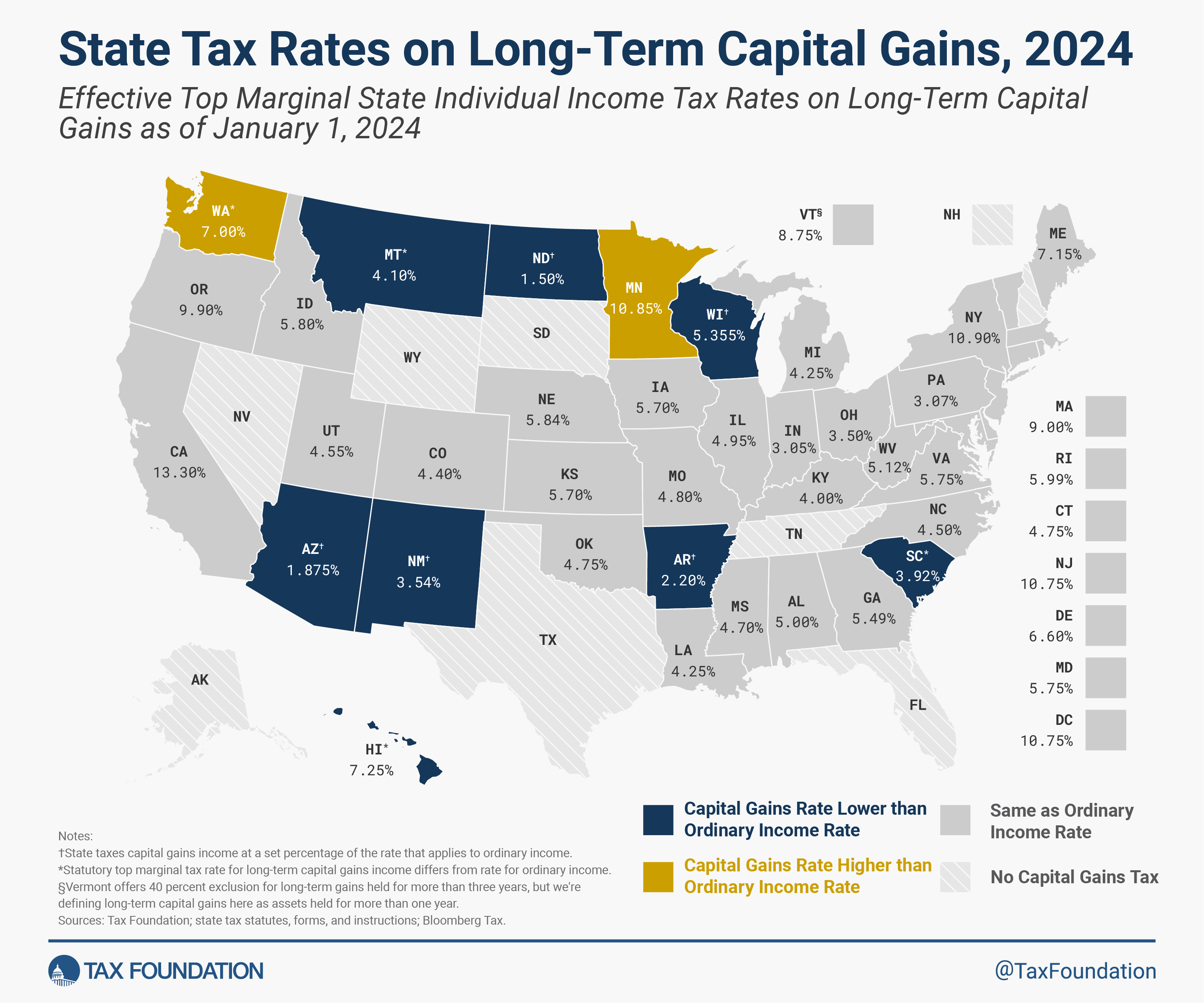

Long-Term Capital Gains Tax Rates

The tax rates applied to long-term capital gains are significantly lower than the ordinary income tax rates. This is a key incentive for investors to hold assets for longer periods. The specific rates depend on your taxable income. For the 2023 tax year (filed in 2024), the long-term capital gains tax rates are:

- 0%: This rate applies to individuals whose taxable income falls within the lowest income tax brackets.

- 15%: This is the most common rate, applying to individuals whose taxable income falls within the middle income tax brackets.

- 20%: This highest long-term capital gains rate applies to individuals in the highest income tax brackets.

Understanding Taxable Income Brackets

The exact income thresholds for these rates are adjusted annually for inflation. It’s crucial to consult the most up-to-date IRS figures for the specific tax year. For example, for the 2023 tax year, the taxable income thresholds for single filers were:

- 0%: Up to $44,625

- 15%: Between $44,626 and $492,300

- 20%: Over $492,300

For married couples filing jointly, these thresholds are higher. These figures illustrate how higher earners will generally pay a higher percentage of their long-term capital gains in taxes, though still at a reduced rate compared to their ordinary income.

Net Investment Income Tax (NIIT)

In addition to the capital gains tax rates, some individuals may also be subject to the Net Investment Income Tax (NIIT). This is an additional 3.8% tax on the lesser of your net investment income or the amount by which your modified adjusted gross income (MAGI) exceeds a certain threshold. Long-term capital gains are considered investment income for the purposes of the NIIT. This means that for higher earners, the effective tax rate on long-term capital gains could reach 23.8% (20% + 3.8%). The NIIT is designed to ensure that individuals with significant investment income contribute to the Medicare tax.

Special Considerations for Certain Assets

While the general rules for long-term capital gains apply broadly, there are some special considerations for specific types of assets, which can be particularly relevant in the technology sector.

Depreciable Business Property (Section 1231 Gains)

If you sell depreciable business property, such as commercial drones used for surveying or delivery, that you’ve owned for more than a year, the gains may be treated as long-term capital gains. However, a portion of these gains might be subject to “depreciation recapture,” which is taxed at ordinary income rates, up to a maximum of 25%. This occurs because you likely took depreciation deductions on the asset over time, reducing your ordinary income. The recapture provision ensures that some of that tax benefit is reversed upon sale.

Collectibles

Investments in collectibles, such as vintage cameras or unique drone prototypes (if they qualify as collectibles), may be subject to a higher long-term capital gains tax rate of 28%. This rate applies regardless of your income bracket. The definition of collectibles is quite specific and includes items like artwork, antiques, and other tangible personal property with a high degree of rarity or historical significance.

Qualified Small Business Stock (QSBS)

For entrepreneurs and early investors in qualifying small businesses, Section 1202 of the Internal Revenue Code offers a significant tax advantage. If you hold qualified small business stock for more than five years, you may be able to exclude up to 100% of the capital gain from taxation. This exclusion is subject to certain limitations, such as the size of the business and the amount of stock sold. This can be a game-changer for founders and investors in emerging tech companies, including those in the drone industry.

Strategies for Managing Long-Term Capital Gains Tax

Effectively managing your tax liability on long-term capital gains is a key component of sound financial planning. By implementing strategic approaches, you can potentially reduce your tax burden and maximize your investment returns.

Tax-Loss Harvesting

As mentioned earlier, capital losses can be used to offset capital gains. Tax-loss harvesting involves strategically selling investments that have decreased in value to realize capital losses. These losses can then be used to offset any capital gains you have realized, including long-term capital gains. If your losses exceed your gains, you can use up to $3,000 of the excess to reduce your ordinary income. This strategy is particularly useful in portfolios with diversified assets where some investments are performing poorly while others are appreciating.

Holding Assets for the Long Term

The most straightforward strategy to benefit from lower long-term capital gains rates is to simply hold your assets for more than one year. By resisting the urge to sell profitable assets too quickly, you ensure that any gains realized will be taxed at the more favorable long-term rates. This aligns with the general intent of capital gains tax policy, which favors long-term investment over speculative trading.

Strategic Asset Allocation and Diversification

A well-diversified portfolio can help mitigate risk and improve the chances of realizing long-term gains. By spreading your investments across different asset classes and sectors, you reduce the impact of any single asset’s poor performance. When it comes to selling assets, consider which ones have appreciated the most and have been held for the longest period. Prioritizing the sale of these assets can allow you to lock in long-term gains while potentially deferring gains on assets with shorter holding periods.

Tax-Advantaged Accounts

Investing within tax-advantaged retirement accounts, such as 401(k)s and IRAs, can significantly alter the tax treatment of capital gains. Within these accounts, capital gains and losses are generally not taxed annually. Instead, taxes are deferred until withdrawal (in traditional accounts) or eliminated altogether (in Roth accounts). This means that the buy and sell decisions within these accounts do not trigger immediate capital gains tax liabilities, allowing for more flexibility in managing your investment strategy without immediate tax consequences.

Timing Your Sales

Consider the timing of your sales, especially if you anticipate a change in your income bracket. If you expect your income to decrease in a future year, you might consider deferring sales that would generate significant capital gains until that lower-income year, potentially qualifying for the 0% or 15% capital gains tax rates. Conversely, if you anticipate your income to rise, it might be beneficial to realize some capital gains in the current year while you are still in a lower tax bracket.

Conclusion: Navigating Capital Gains for Informed Investment

Understanding how long-term capital gains are taxed is not just an abstract financial concept; it has direct implications for investors, entrepreneurs, and anyone involved in the technology and innovation landscape. Whether you are selling shares in a drone startup, a valuable piece of aerial imaging equipment, or an entire business built around flight technology, knowing the tax rules can significantly impact your net returns.

The preferential tax rates for long-term capital gains serve as a powerful incentive to invest for the long haul. By carefully considering the holding period, understanding your taxable income bracket, and being aware of additional taxes like the NIIT, you can make more informed decisions about your investments. Furthermore, employing strategies such as tax-loss harvesting, strategic asset allocation, and utilizing tax-advantaged accounts can help you optimize your tax liability.

As the drone industry, camera technology, and flight innovation continue to evolve at a rapid pace, so too will the financial landscapes surrounding these sectors. Staying informed about tax regulations, consulting with financial professionals, and integrating tax planning into your overall investment strategy will be paramount to navigating the complexities and capitalizing on the opportunities that lie ahead. By mastering the nuances of capital gains taxation, you equip yourself with a crucial tool for long-term financial success in the dynamic world of technology.