The landscape of business formation is often a complex one, filled with terminology that can be both daunting and critical to a venture’s success. For aspiring entrepreneurs, understanding the fundamental structures available is paramount. Among the most common and often-confused entities are the Sole Proprietorship and the Limited Liability Company (LLC). While both offer pathways to business ownership, their operational frameworks, legal protections, and tax implications diverge significantly. This article will delve into the core distinctions, empowering you with the knowledge to make an informed decision for your enterprise.

The Foundation: Defining Each Business Structure

At its heart, understanding the difference begins with a clear definition of each structure. These definitions lay the groundwork for appreciating the subsequent operational and legal ramifications.

Sole Proprietorship: The Unincorporated Individual

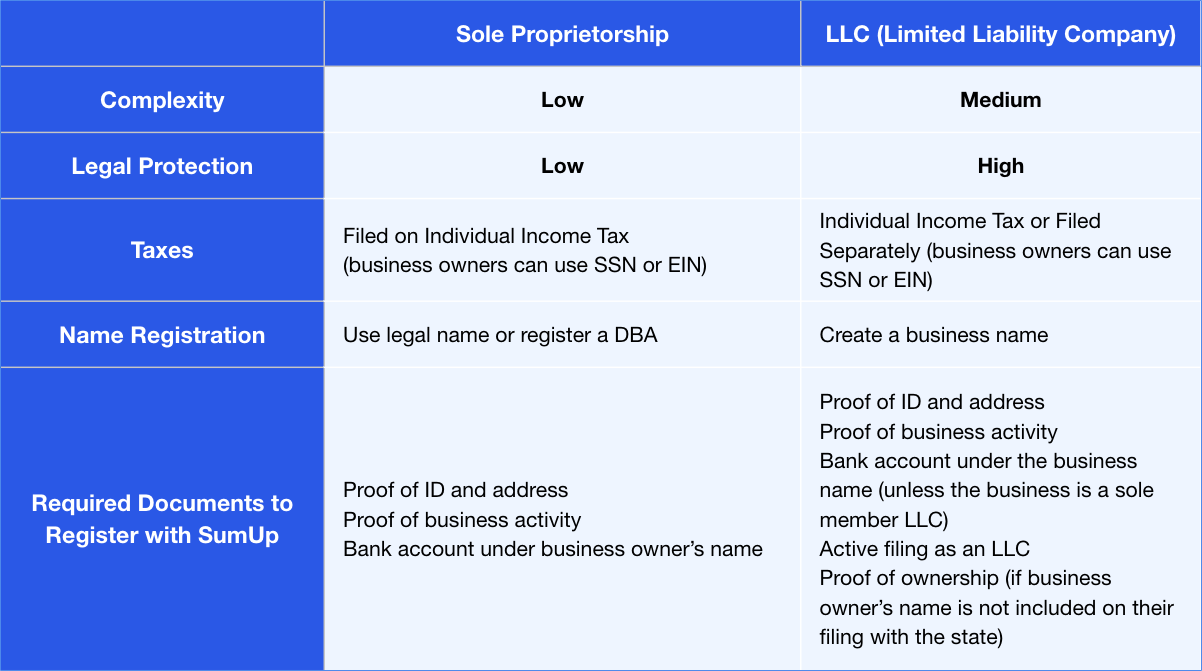

A sole proprietorship is the simplest and most straightforward business structure. It is owned and run by one individual, and there is no legal distinction between the owner and the business. This means that the business’s debts and liabilities are the owner’s personal debts and liabilities. The owner directly receives all profits. Setting up a sole proprietorship is typically easy and requires minimal paperwork, often involving simply starting to conduct business. Many small businesses, freelancers, and independent contractors begin their journey as sole proprietors due to its simplicity and low startup costs.

Key Characteristics of a Sole Proprietorship:

- Single Ownership: The business is owned by one person.

- No Legal Distinction: The owner and the business are considered the same legal entity.

- Unlimited Liability: The owner is personally responsible for all business debts and obligations.

- Pass-Through Taxation: Business income and losses are reported on the owner’s personal tax return.

- Ease of Formation: Minimal legal formalities and low startup costs.

- Direct Control: The owner has complete control over all business decisions.

Limited Liability Company (LLC): Blending Protection and Flexibility

An LLC, on the other hand, is a hybrid business structure that offers the pass-through taxation of a sole proprietorship or partnership with the limited liability of a corporation. In an LLC, the owners are known as “members.” Unlike a sole proprietorship, an LLC is a distinct legal entity separate from its owners. This separation is the defining feature that provides members with personal liability protection.

Key Characteristics of an LLC:

- Multiple Ownership Options: Can be owned by one person (single-member LLC) or multiple people (multi-member LLC).

- Separate Legal Entity: The LLC is legally distinct from its owners.

- Limited Liability: Members’ personal assets are protected from business debts and lawsuits.

- Flexible Taxation: Can choose to be taxed as a sole proprietorship, partnership, S-corporation, or C-corporation.

- Formal Formation: Requires filing specific documents with the state and often involves ongoing compliance.

- Operational Flexibility: Offers more flexibility in management and operation compared to corporations.

Core Differentiators: Liability and Legal Standing

The most significant divergence between an LLC and a sole proprietorship lies in their approach to liability and their legal standing within the business world. This distinction has profound implications for the owner’s financial security and the business’s ability to operate.

Unlimited Personal Liability vs. Limited Liability Protection

The hallmark of a sole proprietorship is unlimited personal liability. This means that if the business incurs debts, faces lawsuits, or is held responsible for damages, the owner’s personal assets—such as their house, car, savings accounts, and other investments—can be legally seized to satisfy these obligations. There is no shield between the business’s financial troubles and the owner’s personal wealth. Creditors and claimants can pursue the owner’s personal assets directly.

In stark contrast, an LLC provides limited liability protection. This is the primary advantage and often the driving force behind choosing an LLC structure. The LLC itself is responsible for its debts and liabilities. If the business faces a lawsuit or accumulates debt, the personal assets of the LLC members are generally shielded. Creditors and claimants can only pursue the assets of the LLC itself. This protection is not absolute; it can be compromised by personal guarantees made by the owner, or in cases of fraud or commingling of funds, but for standard business operations, it offers a crucial layer of personal financial security.

Legal Entity Status: Owner as the Business vs. Business as Separate Entity

The legal standing of a sole proprietorship is that the owner and the business are one and the same. There is no legal separation. When you operate as a sole proprietor, you are essentially trading under your own name, or a fictitious business name (DBA – “Doing Business As”), but legally, it’s still you. This simplifies operations but eliminates the formal recognition of the business as an independent entity.

An LLC, however, is a separate legal entity. This means it has its own legal identity, distinct from its owners. It can enter into contracts in its own name, own property, sue, and be sued, all separate from its members. This legal separation is what enables the limited liability protection, as it establishes a clear boundary between the business’s obligations and the owners’ personal affairs. This distinction can also lend greater credibility to the business in the eyes of partners, lenders, and customers.

Operational and Administrative Considerations

Beyond liability, the day-to-day operations, administrative requirements, and tax treatments also present significant differences between these two business structures. Understanding these aspects is crucial for long-term management and compliance.

Formation and Ongoing Compliance

Forming a sole proprietorship is remarkably simple and often requires no formal state filing beyond obtaining necessary business licenses or permits related to your specific industry. You can essentially begin operating as a sole proprietor by simply starting your business activities. There are generally no ongoing state compliance requirements beyond renewing any required licenses.

Establishing an LLC, conversely, involves more formal steps. You must file “Articles of Organization” (or a similar document, depending on the state) with the Secretary of State or equivalent agency in the state where you wish to form the LLC. This process typically incurs filing fees. Furthermore, LLCs often have ongoing compliance obligations, which can include:

- Annual Reports: Many states require LLCs to file annual reports and pay associated fees to maintain their good standing.

- Operating Agreement: While not always legally mandated by every state for single-member LLCs, a well-drafted Operating Agreement is highly recommended. This internal document outlines the ownership structure, member responsibilities, profit/loss distribution, and management procedures, providing a clear roadmap for the LLC’s operations.

- Separate Bank Accounts: Maintaining separate bank accounts for the LLC is essential for preserving the limited liability protection. Commingling personal and business funds can lead to the piercing of the corporate veil.

Taxation: Pass-Through Simplicity vs. Tax Flexibility

Both sole proprietorships and most LLCs benefit from pass-through taxation. This means the business itself does not pay income tax. Instead, the profits and losses of the business are “passed through” directly to the owner(s) and reported on their personal income tax returns.

For Sole Proprietorships: The owner reports all business income and deductible expenses on Schedule C (Profit or Loss From Business) of their Form 1040. They are also subject to self-employment taxes (Social Security and Medicare) on their business profits.

For LLCs: The tax treatment of an LLC is more flexible.

- Single-Member LLC: By default, a single-member LLC is taxed like a sole proprietorship. The owner reports profits and losses on Schedule C of their personal tax return.

- Multi-Member LLC: By default, a multi-member LLC is taxed like a partnership. The LLC files an informational tax return (Form 1065), and each member receives a Schedule K-1 detailing their share of the profits and losses, which they then report on their personal tax returns.

- LLC Election: An LLC can elect to be taxed as a corporation (either an S-corporation or a C-corporation) by filing specific forms with the IRS. This election can sometimes offer tax advantages, particularly for businesses with significant profits, by allowing for more nuanced control over income distribution and the potential to reduce self-employment taxes. This flexibility in tax classification is a key advantage of the LLC structure.

Management and Decision-Making

In a sole proprietorship, decision-making is straightforward. The owner is the sole authority and can make any decision without consulting others. This offers speed and agility in operations.

An LLC’s management structure can be more varied. LLCs can be member-managed, where all members actively participate in the daily operations and decision-making, similar to a partnership. Alternatively, they can be manager-managed, where members appoint one or more managers (who can be members or external individuals) to run the business. This structure is often preferred when some members are passive investors or when professional management is desired. The Operating Agreement typically dictates the management structure and decision-making protocols.

Weighing the Options: When to Choose Which Structure

The decision between forming an LLC or operating as a sole proprietorship hinges on a careful evaluation of your business’s specific needs, risk tolerance, and growth aspirations. There isn’t a one-size-fits-all answer; rather, it’s about aligning the business structure with your strategic goals.

Considerations for the Sole Proprietorship

A sole proprietorship is often the ideal choice for individuals who:

- Are just starting out and have minimal capital: The low barrier to entry and minimal setup costs are attractive.

- Operate a low-risk business: If your business activities do not inherently involve significant potential for lawsuits or substantial debt accumulation, the unlimited liability might be an acceptable risk.

- Value extreme simplicity and autonomy: The direct control and lack of administrative overhead are appealing.

- Intend to operate as a freelancer or independent contractor: For individuals providing services without significant business overhead or potential for product liability.

- Plan to transition to another structure soon: It can serve as a temporary starting point before a more formal entity is established.

However, it’s crucial to remember that as your business grows and its potential liabilities increase, the risks associated with unlimited personal liability become more pronounced.

Considerations for the LLC

An LLC is generally a more suitable choice for businesses that:

- Engage in activities with inherent risks: Businesses that involve potential for injury, product defects, contractual disputes, or significant financial obligations benefit greatly from liability protection.

- Seek to protect personal assets: If safeguarding your home, savings, and other personal investments from business-related creditors is a priority, an LLC is a strong option.

- Plan for growth and investment: The LLC structure can be more appealing to potential investors and lenders due to its formal recognition and limited liability.

- Desire flexibility in taxation: The option to elect corporate tax status can provide strategic tax planning opportunities.

- Plan to have multiple owners or partners: While a sole proprietor can operate under a DBA, an LLC provides a clear framework for multiple owners with defined roles and profit/loss distribution.

- Wish to enhance business credibility: The LLC designation can sometimes project a more professional and established image than a sole proprietorship.

Ultimately, while a sole proprietorship offers unparalleled simplicity, the limited liability and operational flexibility of an LLC often make it a more robust and secure choice for businesses with even moderate growth potential or inherent risks. Consulting with a legal professional or a business advisor can provide personalized guidance to help you navigate these critical decisions.