In the rapidly evolving landscape of unmanned aerial vehicles (UAVs), the financial investment required to maintain a competitive edge is staggering. As professional-grade drones transition from simple hobbyist tools to sophisticated enterprise assets—often costing tens of thousands of dollars—the mechanisms used to protect these investments have become increasingly complex. One term that has migrated from the automotive and heavy machinery sectors into the world of high-end quadcopters is “gap insurance.”

For a drone operator, gap insurance is a specialized form of financial protection designed to bridge the disparity between the actual cash value (ACV) of a drone at the time of an accident and the amount still owed on its financing or lease agreement. In an industry where hardware depreciates rapidly due to the constant release of newer, more capable models, understanding what gap insurance is used for is essential for any commercial pilot or fleet manager looking to safeguard their operational continuity.

Understanding the Financial “Gap” in Professional UAV Hardware

The primary utility of gap insurance in the drone sector stems from the volatile nature of electronics depreciation. When a company purchases a high-end enterprise drone, such as a DJI Matrice 350 RTK or a specialized LiDAR-equipped hexacopter, the asset’s market value begins to decline the moment it is registered and put into service.

The Mechanics of Actual Cash Value vs. Loan Balance

Standard hull insurance for drones typically operates on an Actual Cash Value basis. If a drone suffers a total loss—perhaps due to a catastrophic hardware failure or a “fly-away” event—the insurance provider calculates the payout based on what the drone was worth on the open market five minutes before the crash. This takes into account wear and tear, battery cycles, and the current market price of newer iterations.

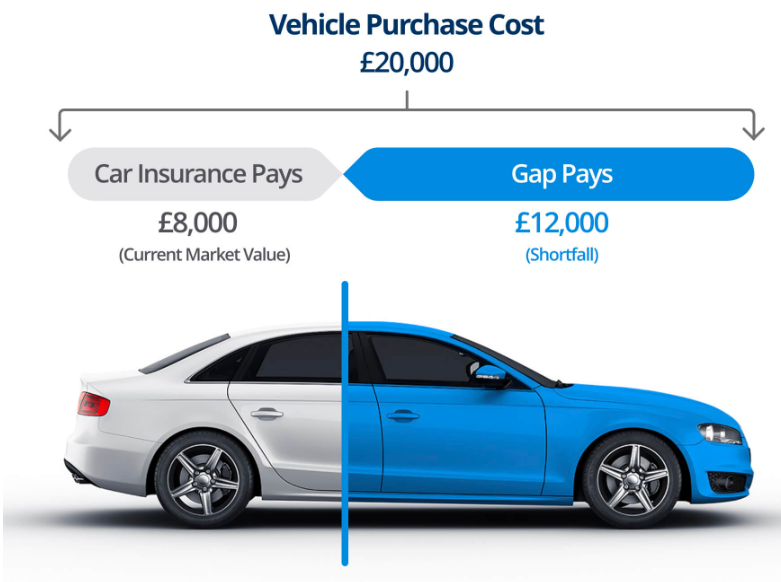

However, if the drone was financed through a bank or a specialized equipment lender, the balance of that loan does not decrease as fast as the drone’s market value. This creates a “gap.” Without gap insurance, an operator might receive a $10,000 payout for a totaled drone but still owe the lender $14,000. Gap insurance is used to cover that $4,000 deficit, ensuring the operator isn’t paying for a “ghost” drone that no longer exists in their hangar.

Depreciation Curves in High-End Drone Systems

Unlike traditional aircraft, which may hold their value for decades, drones are subject to the same “Moore’s Law” pressures as smartphones and computers. A drone that was top-of-the-line last year may be rendered obsolete by a firmware-locked competitor or a new sensor suite this year. This accelerated depreciation makes the “gap” in drone financing much wider and more dangerous than in other industries. Gap insurance acts as a stabilizer, allowing businesses to invest in the latest UAV technology without the fear that a single mid-air collision will leave them in a cycle of debt.

Why Commercial Drone Fleets Require Specialized Financial Coverage

For individual hobbyists flying micro-drones or FPV racers, the loss of a unit is often a manageable personal expense. However, for commercial entities using drones for infrastructure inspection, precision agriculture, or public safety, the drone is a revenue-generating asset. The loss of that asset without full financial recovery can halt business operations entirely.

Protecting Financed Equipment and Leases

Many drone service providers (DSPs) utilize leasing models to keep their fleets current. These leases often contain clauses that require the lessee to pay the full remaining balance of the lease immediately if the equipment is destroyed. Gap insurance is used specifically to satisfy these contractual obligations. It provides a safety net for startups and small businesses that do not have the liquid capital to pay off a $20,000 lease while simultaneously trying to purchase a replacement unit to fulfill their client contracts.

Risk Mitigation for Enterprise-Grade Quadcopters

Enterprise-grade quadcopters are often equipped with modular payloads, such as thermal sensors, multispectral cameras, or gas sniffers. While hull insurance might cover the “airframe,” the complex financing often bundles the airframe and the sensors together. If a drone is lost in a high-risk environment—such as a dense urban construction site or over water—the financial exposure is total. Gap insurance ensures that the “total loss” scenario doesn’t become a “total business failure.” It allows the risk management team to treat the drone as a replaceable tool rather than a fragile liability.

Key Scenarios Where Drone Gap Insurance is Vital

To truly understand what gap insurance is used for, one must look at the specific operational risks unique to the drone industry. Drones operate in three-dimensional space, often in “dirty, dangerous, or dull” environments where the risk of total loss is significantly higher than that of ground-based assets.

Total Loss During Beyond Visual Line of Sight (BVLOS) Operations

As the FAA and other global regulators open the skies to Beyond Visual Line of Sight (BVLOS) flights, the stakes for drone operators have increased. BVLOS operations involve long-distance flights for delivery or pipeline inspection where the pilot cannot physically see the aircraft. If a drone goes down in a remote or inaccessible area, it is often classified as a total loss because recovery of the hardware is impossible or prohibitively expensive. In these instances, the insurance payout for a “lost” drone is almost always lower than the remaining loan balance, making gap coverage the only way to clear the financial slate.

Theft and Irretrievable Hardware Loss

Drones are highly portable and high-value, making them prime targets for theft. Furthermore, drones used for maritime inspections or offshore wind farm monitoring face the constant risk of “sinking” into the ocean. When a drone is stolen or ends up at the bottom of the sea, there is no salvage value to offset the loss. The gap insurance policy is used to bridge the chasm between the depreciated “book value” and the reality of the owner’s financial debt to the lender.

Evaluating the Cost-Benefit Ratio of Premium UAV Protection

Choosing to add gap insurance to a drone’s protection plan is a strategic decision that depends on the specific hardware being flown and the financial structure of the business. It is not always necessary for every drone, but for some, it is the most critical line in the budget.

Integrating Gap Coverage into Operational Budgets

When calculating the “Cost Per Flight Hour,” professional operators must include insurance premiums. While gap insurance adds an additional monthly or annual cost, it should be viewed as an “exit strategy” for a bad situation. If an operator is flying a DJI Matrice 30T that is fully paid off, gap insurance is unnecessary. However, if they are flying a fleet of five units on a 36-month lease, the cumulative “gap” across the fleet could be fifty thousand dollars or more. In this context, the insurance premium is a small price to pay for the assurance that a fleet-wide disaster won’t lead to bankruptcy.

Future-Proofing Your Aerial Assets

The drone industry moves at a breakneck pace. As we see the rise of AI-driven autonomous flight and more advanced collision avoidance systems, older drones become less desirable on the secondhand market. This drop in secondhand value is exactly what widens the gap that gap insurance is designed to fill. By utilizing gap insurance, a drone business can effectively “future-proof” its finances. They can commit to the most advanced technology available today, knowing that even if that technology’s market value craters tomorrow, their debt remains covered in the event of an accident.

Conclusion: The Role of Gap Insurance in a Maturing Drone Industry

As the drone industry matures, the focus is shifting from simply “how to fly” to “how to manage a drone business.” This shift requires a deeper understanding of asset management and financial protection. Gap insurance is no longer a niche product for car buyers; it is a vital tool for the modern UAV professional.

What gap insurance is used for, ultimately, is the preservation of momentum. In the high-stakes world of commercial drone operations, a crash is often just a matter of “when,” not “if.” When that moment arrives, the goal of any operator is to get back into the air as quickly as possible. By covering the difference between insurance payouts and loan balances, gap insurance removes the financial anchors that keep businesses grounded after an accident. It allows pilots and companies to focus on what they do best—capturing data, delivering goods, and innovating in the sky—without the looming shadow of underwater loans. For any drone operation that relies on financed, high-value hardware, gap insurance is not just an added expense; it is the foundation of a resilient and sustainable business model.