In the rapidly evolving landscape of unmanned aerial vehicles (UAVs), the term “insurance” has transitioned from an optional safeguard to a fundamental pillar of professional operations. For enterprise pilots, surveying firms, and aerial cinematographers, a drone is not merely a gadget; it is a high-value technological asset. Much like health insurance for a human being, drone insurance serves to mitigate the financial impact of unforeseen “health” crises—be they mechanical failures, bird strikes, or pilot error. Central to this financial safety net is the concept of the deductible.

In this guide, we will explore the nuances of drone insurance deductibles within the Tech & Innovation niche. We will examine how professional operators navigate the trade-offs between premiums and out-of-pocket costs, how advanced tech like AI and remote sensing impacts these financial structures, and why understanding your “hull health” is the key to a sustainable UAV business.

Defining the Deductible in the Context of Professional Drone Operations

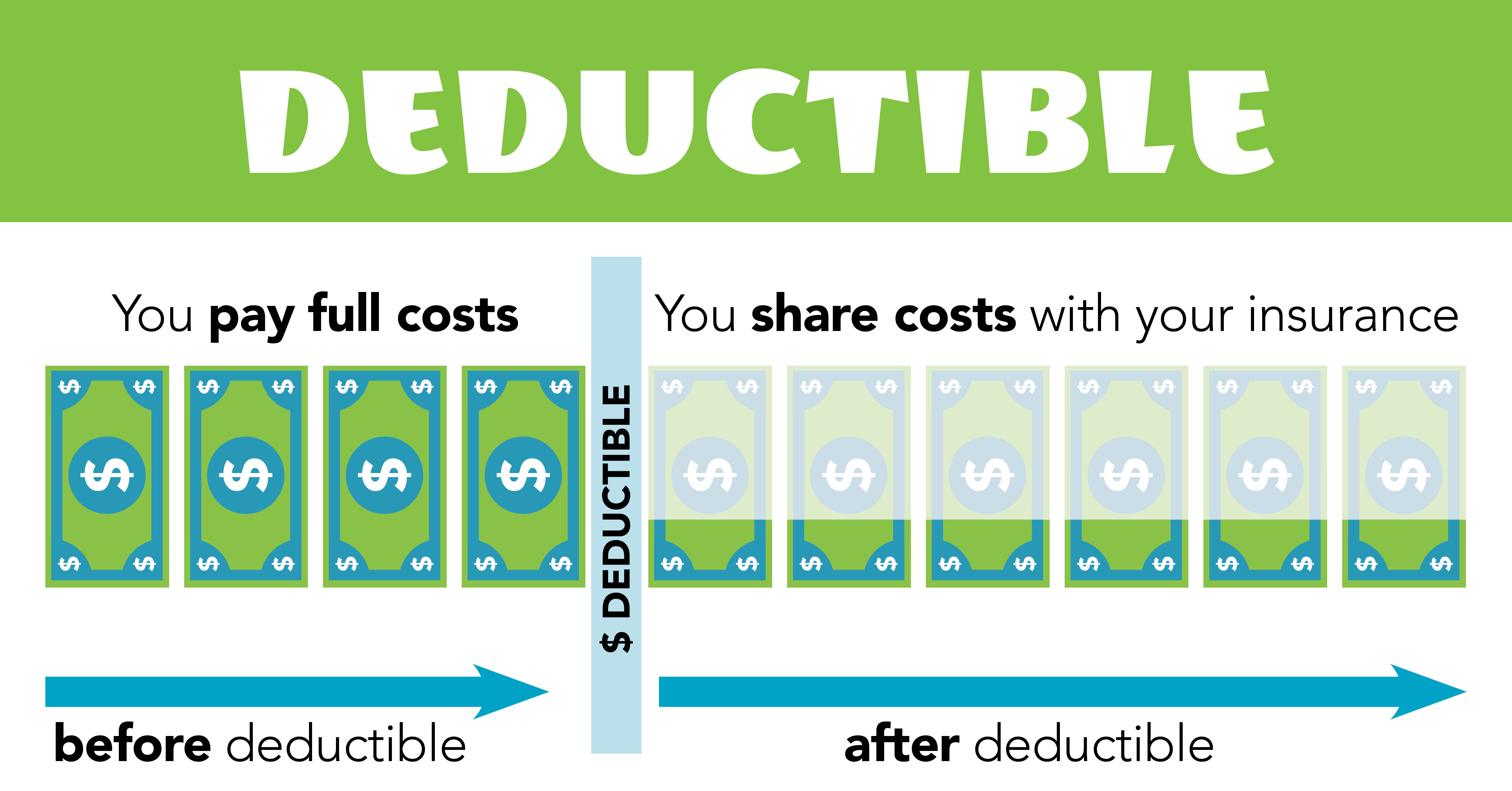

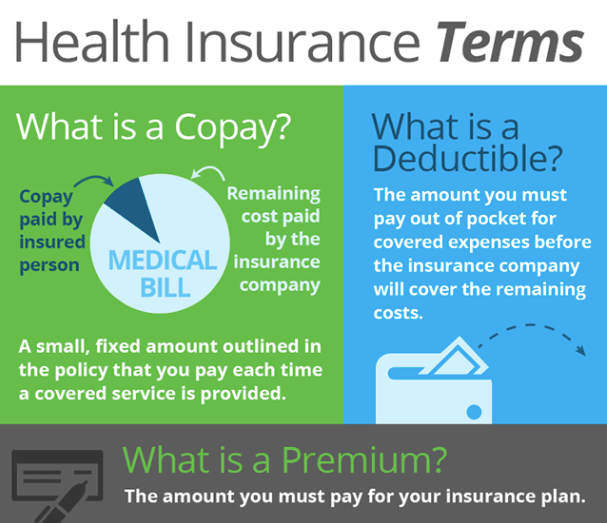

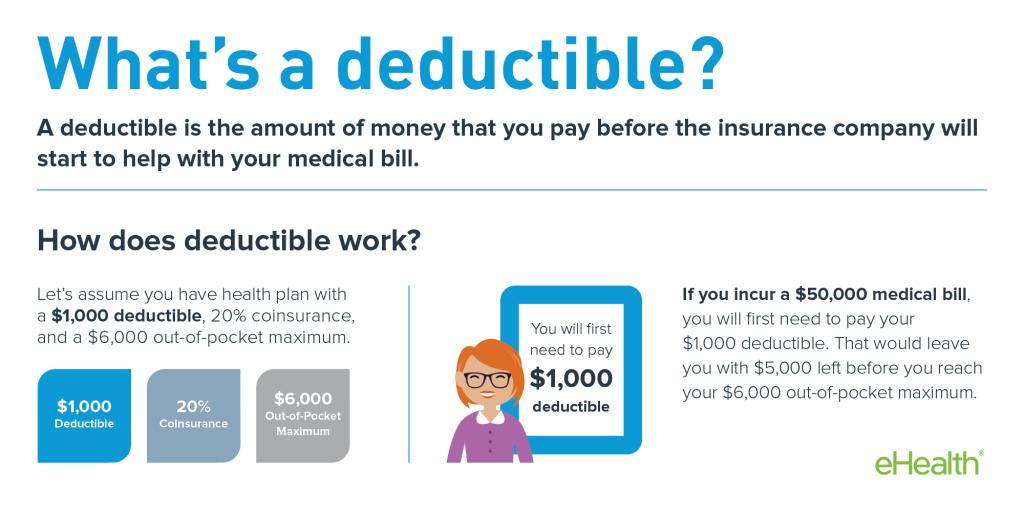

In the world of drone technology and innovation, a deductible is the pre-determined amount of money an operator must pay out-of-pocket before their insurance provider covers the remainder of a claim. Whether you are operating a fleet of mapping drones or a single high-end cinematic rig, the deductible acts as a shared risk mechanism between the insurer and the policyholder.

The Relationship Between Deductibles and Premiums

The financial mechanics of drone insurance are built on an inverse relationship: as your deductible increases, your monthly or annual premium typically decreases. For tech-heavy enterprises, this is a strategic calculation. A high deductible suggests that the company has high confidence in its flight stabilization systems and pilot training, essentially “self-insuring” for minor incidents to keep overhead costs low. Conversely, a low deductible provides a safety net for high-risk environments—such as urban infrastructure inspection—where the likelihood of a localized “fender bender” is higher.

Hull Insurance vs. Liability Coverage

It is vital to distinguish between the two primary types of drone insurance, as deductibles apply differently to each. Hull Insurance covers the physical “health” of the drone itself—the airframe, the internal sensors, and the propulsion system. This is where the deductible is most prominent. If a $20,000 LiDAR drone crashes, and the policy has a 10% deductible, the operator pays $2,000 toward the repair or replacement. Liability Insurance, on the other hand, covers damage the drone causes to third-party property or people. In many professional liability policies, there may be no deductible at all, as the focus is on protecting the operator from catastrophic legal or medical expenses.

Why Enterprise Tech and Innovation Demand Robust Insurance Structures

As drones move beyond simple 4K photography into the realms of Remote Sensing, Mapping, and Autonomous Flight, the value of the equipment has skyrocketed. We are no longer talking about a few hundred dollars; we are talking about sophisticated flying computers carrying payloads that often exceed the cost of the aircraft itself.

Protecting High-Value Payloads: LiDAR and Thermal Imaging

Innovation in sensor technology has introduced a new layer of complexity to insurance deductibles. A modern enterprise drone might carry a Zenmuse H20T thermal camera or a high-end LiDAR sensor for topographic mapping. These sensors are delicate and expensive. When choosing an insurance policy, operators must ensure that the deductible is structured to account for “payload-only” damage. In some cases, a minor hard landing might not damage the drone’s airframe but could knock a $15,000 thermal sensor out of alignment. Understanding how your deductible applies to these modular tech components is essential for maintaining the financial health of your innovation pipeline.

Autonomous Flight and the Evolution of Risk Assessment

The rise of AI Follow Mode and autonomous pathfinding has changed the way insurers calculate risk. In the early days of UAV tech, pilot error was the leading cause of claims. Today, with obstacle avoidance and GPS-redundancy systems, drones are “healthier” and safer than ever. However, autonomous flight introduces “systemic risk”—the possibility of a software glitch or a lost-link scenario. Insurers are now looking at the tech stack of the drone to determine deductible rates. A drone equipped with 360-degree obstacle avoidance and redundant battery systems may qualify for more favorable deductible terms because the technology itself serves as a risk-mitigation tool.

Navigating the Financial Landscape of Drone Maintenance and Repair

Managing a drone fleet is a constant balance between pushing the limits of technology and preserving the physical integrity of the equipment. The deductible is the pivot point of this balance.

Real-World Scenarios: When to Pay the Deductible

Every professional operator eventually faces the “Deductible Dilemma.” Suppose a propeller fails on a mapping drone, causing $1,200 worth of damage to the gimbal. If the policy deductible is $1,000, is it worth filing a claim? Filing a claim for a mere $200 benefit might lead to increased premiums in the next cycle. In the tech industry, many firms choose to handle “minor maintenance” internally, saving their insurance “health plan” for total losses or catastrophic failures. This approach requires a robust internal tech team capable of performing sensor calibrations and airframe repairs without voiding warranties.

Deductible Structures for Fleet Management

For companies utilizing Remote Sensing across dozens of units, individual deductibles can become a logistical nightmare. This has led to the innovation of “aggregate deductibles” or fleet-wide policies. In these structures, the company might have a total deductible for the year across all aircraft. This allows the enterprise to absorb the cost of a few minor “health issues” in their drones while remaining protected against a systemic failure that might ground the entire fleet.

The Role of Data and AI in Reducing Insurance Costs

The future of drone insurance is being written in code. As drones become more connected, the data they generate is being used to create more personalized and fair insurance models, mirroring the “telematics” used in the automotive industry.

Telemetry Data as the ‘Health Record’ of the Drone

Modern UAVs record every detail of their flight: motor RPM, battery temperature, GPS signal strength, and even the frequency of obstacle avoidance triggers. This telemetry data acts as a comprehensive “health record.” In the near future, insurers may offer “Pay-As-You-Fly” models where your deductible is dynamically adjusted based on the health of your equipment and the safety of your flight paths. If your data shows that you consistently fly in low-wind conditions with healthy battery cycles, your deductible for a tech failure might be lowered as a reward for proactive maintenance.

Predictive Maintenance: The Best Insurance Policy

Innovation in AI and Mapping has led to the development of predictive maintenance software. These systems analyze the vibrations and sound profiles of drone motors to predict a failure before it happens. By integrating this technology, operators can essentially eliminate the need to ever pay a deductible for mechanical failure. In the eyes of an insurer, a drone that is monitored by predictive AI is a much lower risk, allowing for innovative policy structures that favor the tech-savvy pilot.

Conclusion: Balancing Innovation and Protection

Understanding “what is a deductible” in the context of drone insurance is about more than just reading the fine print of a policy; it is about understanding the value of your technological investment. In the world of Drones and Tech Innovation, the equipment is the lifeblood of the business. Whether you are conducting remote sensing in the wilderness or mapping an urban construction site, your drone’s “health” is synonymous with your company’s success.

By strategically choosing your deductible, investing in drones with advanced obstacle avoidance, and leveraging telemetry data to prove your operational safety, you can turn insurance from a burdensome cost into a competitive advantage. In an industry defined by rapid change, the most innovative pilots are those who not only know how to fly but also know how to protect the technology that keeps them in the air. As UAV systems continue to advance, the synergy between drone tech and financial risk management will only grow stronger, ensuring that the “health” of the industry remains robust for years to come.